Changes in sentiment may drive the performance of the Eurozone equity markets, even with disappointing economic data.

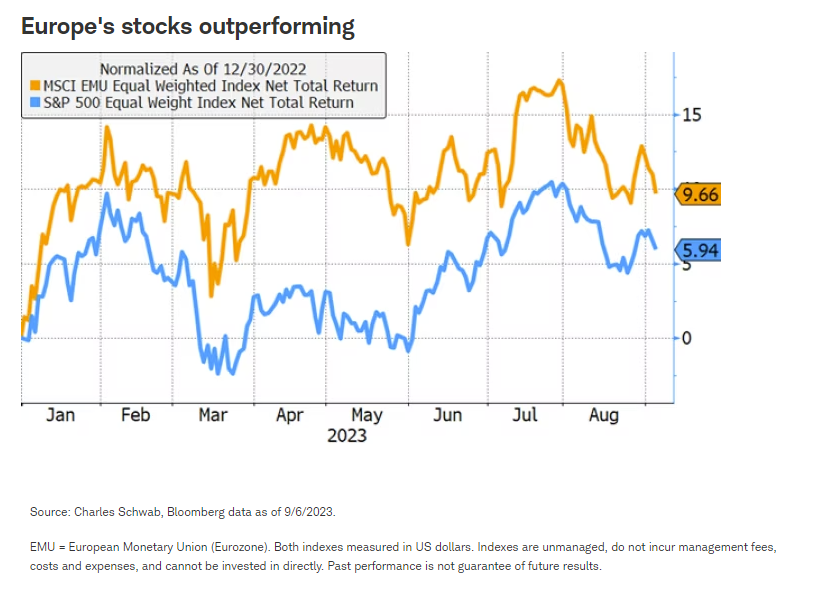

Economic data for the U.S. is now tracking close to 6% GDP growth for the third quarter, according to the Atlanta Fed's GDPNow forecast, which provides a running estimate of real GDP growth based on available economic data for the current quarter. In contrast, the data for Europe shows the economy may be back in recession. Yet, the stock markets are favoring Europe with the average European stock outperforming the average U.S. stock this year and there is a tie in the race so far in the third quarter. Why the weak economy yet strong stock market? Because sentiment matters.

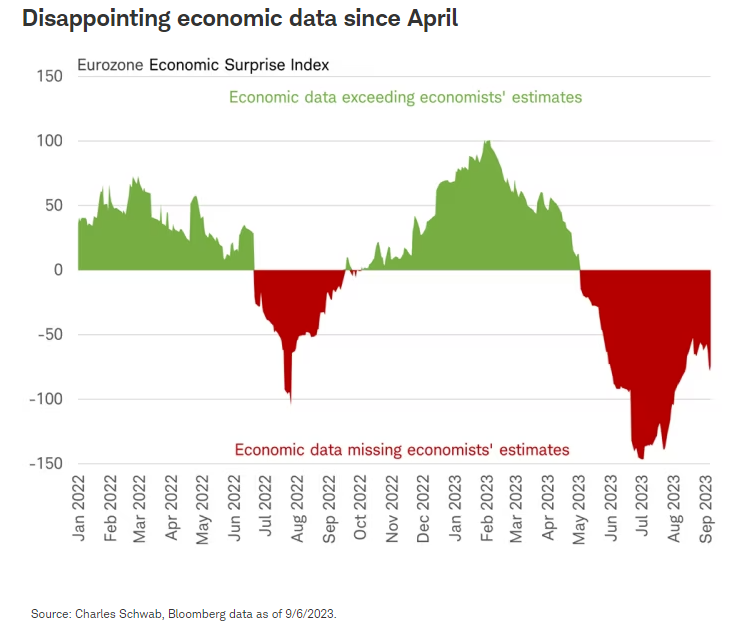

Disappointing data

The Eurozone's economic indicators have continued to surprise on the downside since April. August saw the Eurozone composite Purchasing Managers Index (PMI) fall to 47, from 48.5 in July, with the services PMI unexpectedly dropping into contractionary territory alongside the manufacturing index. In Europe's largest economy, Germany, factory orders for July fell the most since the lockdowns in 2020. The Eurozone consumer confidence recovery also stalled unexpectedly in August, remaining below its long-term average.

The economic surprise index for Europe has been below zero since April. A reading for the Citi Economic Surprise Index below zero means data is coming in worse than Bloomberg-tracked economists' forecasts and above zero means it is better than forecast.

ECB to blame?

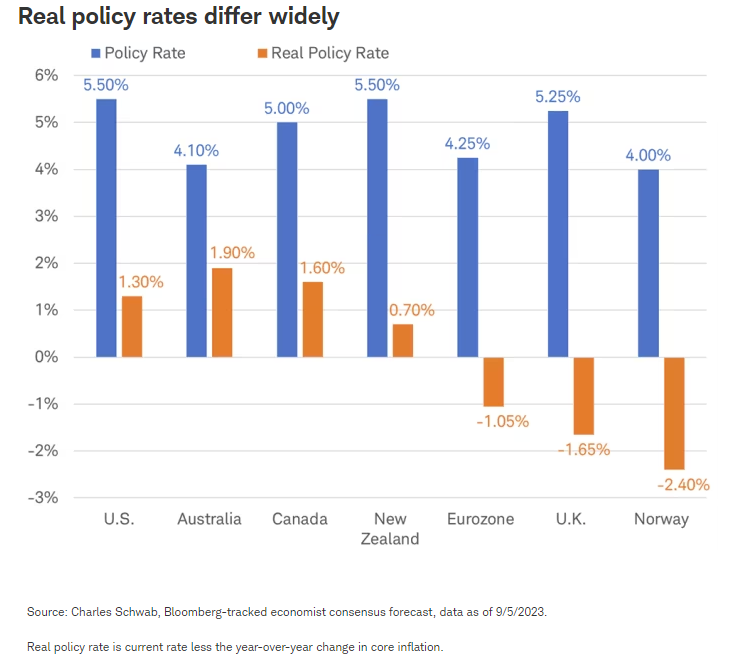

In short, the modest momentum the Eurozone gained in the second quarter of 2023, when real GDP grew +0.3% (not annualized), seems to be evaporating. Does this mean the European Central Bank (ECB) hiked interest rates too far in their efforts to slow demand and cool inflation? The table below suggests not. While the ECB has hiked rates into the 4.0% to 5.5% range of other major central banks, when we adjust the policy rate for core inflation—to determine how restrictive the rate actually is—we can see that the real policy rate is still negative by over 100 basis points (bps). That remains below neutral and nowhere near the positive 130 bps in the U.S., where economic growth continues.

Performance

The performance of Eurozone equity markets does not seem to reflect this extended string of disappointing data. While the average European stock, measured by the equal-weighted MSCI EMU Index, is down from this year's peak at the end of July, it has not broken out to the downside. Rather it has traded sideways over the past five months that the economic surprise index was below zero. And the average European stock has maintained its outperformance of the average U.S. stock so far this year, despite the big gap in economic momentum.

Sentiment matters

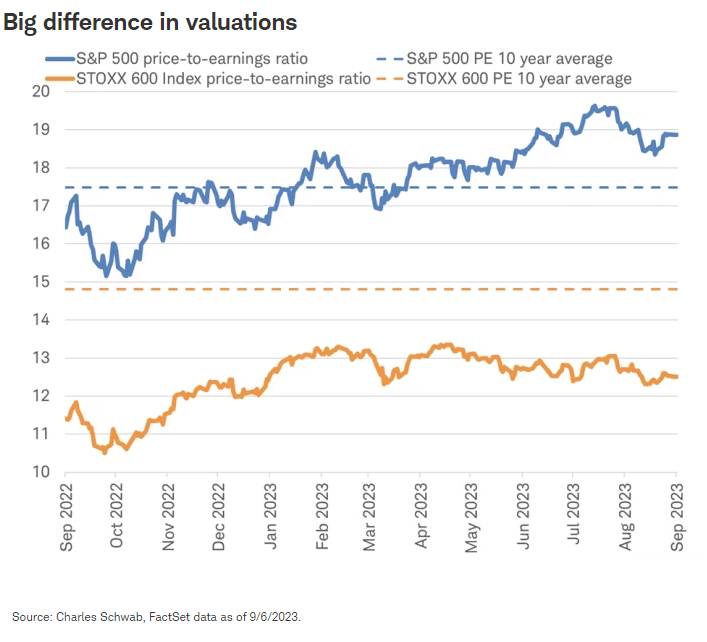

In contrast to the U.S., where an upbeat growth outlook by investors supports an above average multiple on earnings (price-to-earnings ratio) for the S&P 500 Index, investors in Europe have been valuing European stocks in the STOXX 600 Index well below the long-term average. The low earnings multiple indicates that investors have been expecting weaker earnings compared to history and the United States.

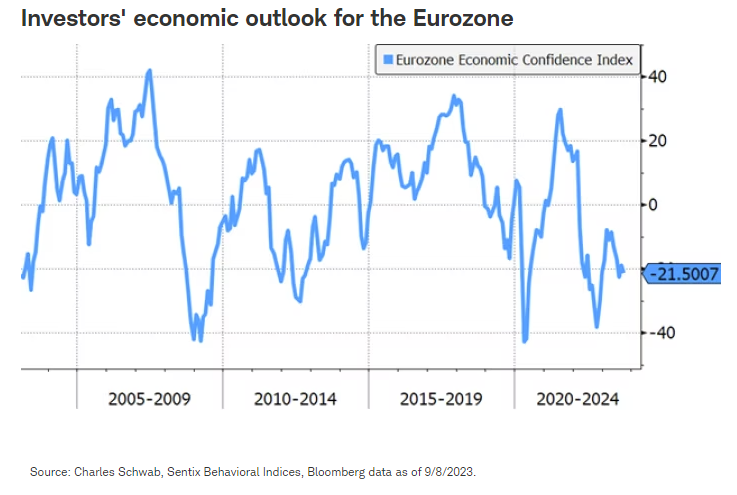

Notably, Eurozone economic sentiment by investors tracked by Sentix is currently dismal, with the confidence index near recessionary lows in August. Global investors are no more cheerful. According to Bank of America's most recent monthly survey in August, the net percentage of fund managers expecting European stock markets to weaken over the coming months climbed to 71%. This suggests any improvement in confidence could provide lift to European stocks.

Investor expectations for Eurozone growth may already be so low that negative surprises are now expected and no longer seem to hurt stock prices. Investors willing to look beyond the current weakness could start to drive up price-to-earnings ratios from these depressed levels as they anticipate the next upswing. Counterintuitively, a catalyst could include more disappointing economic data if that data were considered weak enough to persuade the European Central Bank to halt its unwinding of quantitative easing that began in March and start cutting interest rates. Other developments that could be seen by investors as catalysts for Europe's next economic upswing could also include effective stimulus in China, a rebound in European consumer spending as rapid disinflation pushes up real incomes, or restoration of the grain deal between Russia and Ukraine helping to ease food prices that are currently the largest component of overall Eurozone inflation.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results.

Investing involves risk including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The Sentix Economic Confidence Index is based on a monthly survey of more than 4,000 financial market investors, both institutional and private, that assesses both the current economic situation and expectations for the next six months. The Index has global coverage, as well as coverage for several economic regions including the Eurozone, the U.S. and Japan.

A message from Advisor Perspectives and VettaFi: Equities are essential portfolio building blocks. Join VettaFi for the Equity symposium.

© Charles Schwab

Read more commentaries by Charles Schwab