The 10-year Treasury yield has climbed steadily over the past two years. But we believe fixed-income investors should be prepared for lower yields ahead.

Treasury yields have spent the past year in a state of flux—rising and falling on mixed economic news. The 10-year Treasury yield has climbed as high as 4.3% this year, and some market observers expect it to crest at 5%. We don’t share this view. We believe Treasury yields will eventually come down, making this a potentially attractive entry point for fixed-income investors.

Why We Believe Yields Will Fall

For Treasury yields to fall, we expect to see at least one of three conditions materialize: further evidence of slowing in the US labor market; a continued deceleration in inflation toward the Fed’s target of 2%; and continued weakness in midsize US regional banks. Currently, we see evidence of all three, although this doesn’t mean we can’t see near-term volatility in rates as economic data gets released.

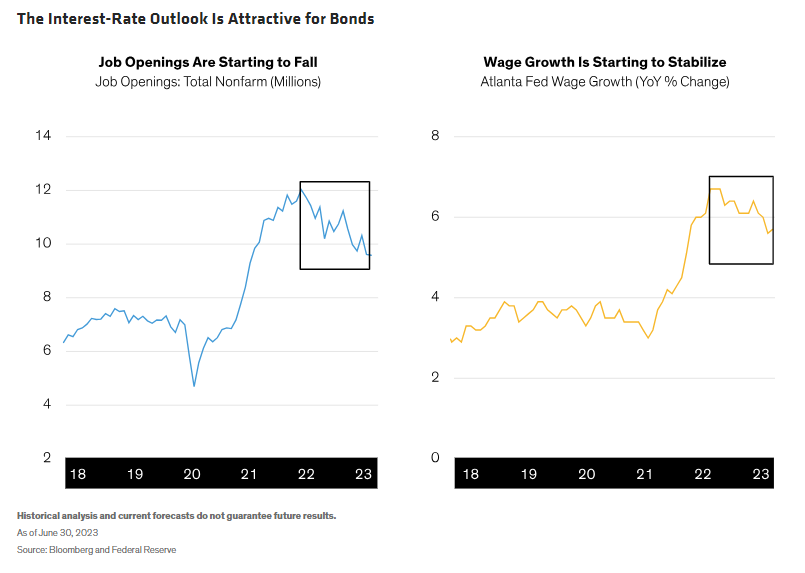

Borrowing costs have increased for many small and midsize businesses, and eventually business owners will need to decide whether it makes sense to continue adding headcount. As excess US consumer savings accumulated during the pandemic dissipate, the answer may increasingly be no. Despite steady but slowing job growth so far in 2023, job openings are now starting to retrench and wage growth is stabilizing (Display), which could portend a slowdown in near-term consumer spending.

Inflation, too, is decelerating, although not as fast as policymakers would like. The Personal Consumption Expenditures Price Index—the Federal Reserve’s preferred barometer of inflation—rose 0.2% in July for the second straight month, which has put some upward pressure on yields. Still, the index is coming off its lowest annual rate in more than two years.

Additionally, regional banks are facing liquidity pressures. The Fed’s Bank Term Funding Program, which was designed to shore up liquidity in the US banking system, will expire in March 2024. With banking liquidity a persistent concern and regional lenders trying to offload private-credit debt and levered loans from their balance sheets, regional banks may provide the Fed with one more risk to consider. This is particularly true given their importance as lenders to small and medium-size businesses.

Economic Risks May Also Pressure Yields

Treasury yields could also fall if other barometers of economic health deteriorate. The Institute for Supply Management’s Purchasing Managers’ Index—a reliable indicator of business sentiment—came in weaker than expected in August. Historically, there has been a relationship between PMI levels and Treasury yields, so this index will bear watching.

The US budget deficit could also factor in. According to the Congressional Budget Office, the cumulative deficit for the period spanning 2024–2033 is expected to top $20 trillion, or more than 6% of US GDP. Exceeding the 6% threshold is a historical rarity. If the cost of servicing its debt rises, the US government won’t have as much to spend on other programs, which could become an impediment to economic growth.

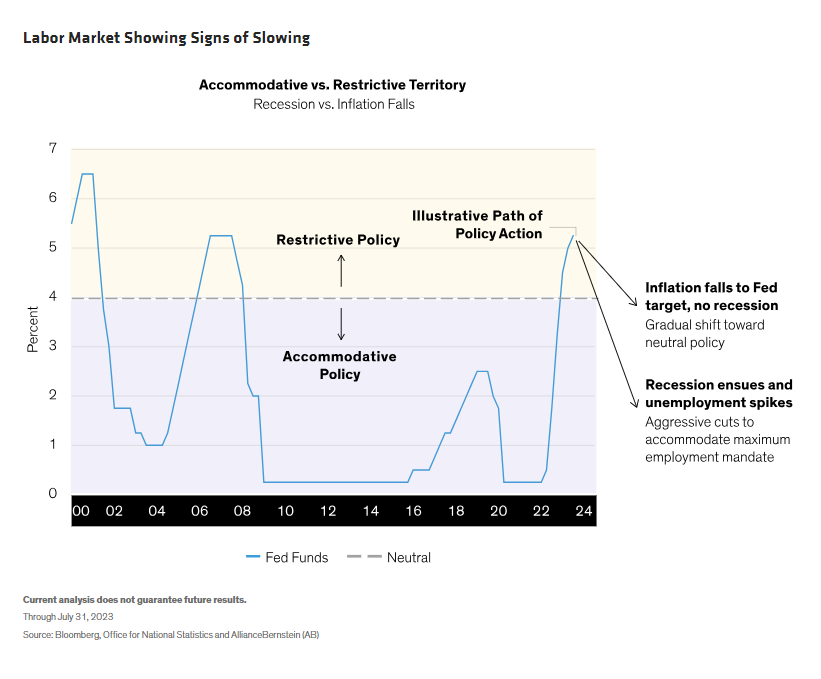

Of course, the Federal Reserve will have the final say. With the target fed funds rate at 5.25–5.5%, monetary policy is already in restrictive territory. If economic growth is steady but inflation continues to decelerate, the Fed is likely to steer interest rates toward its policy-neutral 2.5% rate. If the US falls into recession, rates could fall even more (Display).

Ultimately, there doesn’t need to be a single catalyst for the economy to slow. Any combination of factors could turn the tide. As it stands, we’re forecasting the 10-year Treasury yield to be in the range of 3.5%–4% by year-end.

Outlook Attractive for Bonds

For fixed-income investors, this could be a good entry point or an opportunity to extend duration. Bond valuations are attractive and, despite the potential for economic slowing, corporate issuers are in much better shape financially than they were entering past slowdowns, with sound balance sheets and high interest coverage ratios.

But with yields elevated, timing is critical. We believe investors should consider pairing government bonds with longer-duration high-yield credits that can benefit from lower rates ahead. A diversified “barbell” strategy of this kind can balance interest-rate and credit risk, with high-yield bonds providing income and government securities offering ballast if market conditions turn choppy.

Although we view this as an all-weather approach to fixed-income investing, the current forecast for this strategy is encouraging.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© AllianceBernstein

Read more commentaries by AllianceBernstein