Although US bond yields are well above their lows of the past decade, it’s always a good idea to think globally.

It’s tempting for US investors to focus on their home-field yield advantage and forego opportunities abroad, but we believe that by expanding the fixed-income opportunity set globally, investors can capture much-needed diversification, while still enjoying attractive yields and potential returns. Below are three reasons why we think US investors should embrace the global bond market today.

1. A much bigger opportunity set means more opportunities to add alpha.

Gone are the days when the US fixed-income market dominated the world’s supply of bonds. Today, the US represents less than a third of the global bond universe. And the global bond market is much more diverse than the US bond market. Not only does it offer more opportunities from which an active manager can choose, but its differing landscapes provide significant variety and diversification sources.

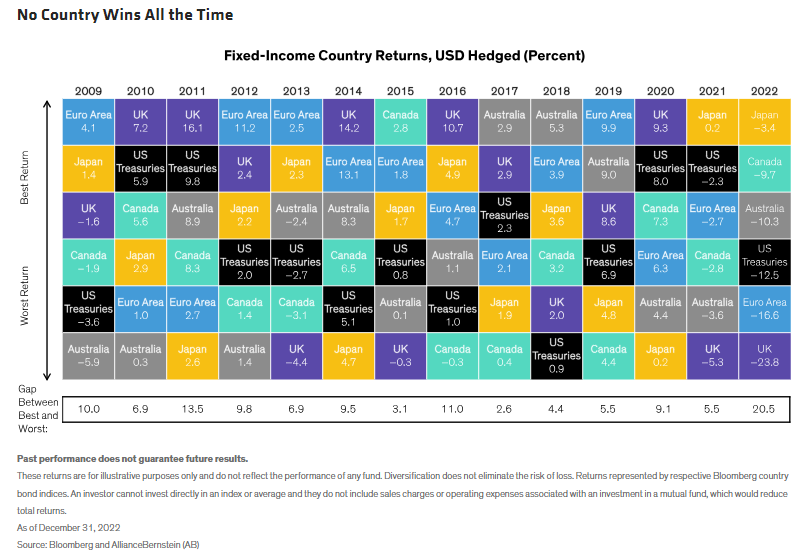

Bond returns differ country by country and year to year because of varying economic cycles, monetary cycles, business cycles, inflation regimes, geopolitical concerns and yield curves. Indeed, on a hedged basis, US Treasuries haven’t been a top performer among government bonds in more than a decade (Display). Similarly, sector returns vary across countries and regions. For example, high-yield corporate bonds may look like weak sauce in one region but a major opportunity in another.

Diverging regimes create opportunities for investors to differentiate and add new sources of alpha. Today, for instance, as central banks come to the end of their hiking cycles, the lagged impact of tightening feeds through to economies at different speeds.

For example, we favor UK government bonds. In the UK, where inflation has lagged the decline seen in other economies, the market has been pessimistic about UK government debt. We take a different view. In our analysis, the growth outlook appears bleak; consumer resilience is being tested, and the economy is feeling the effects of monetary policy tightening. As a result, we believe the market will need to lower their expectations for further tightening.

Meanwhile, despite high hedged yields, we’re cautious on Japan, because diverging rates continue to put pressure on the yen and could lead to further adjustment to Japan’s yield-curve control and even to the removal of its negative interest-rate policy.

2. Hedged global bonds have historically been less volatile, while supplying bigger diversification benefits, than the US bond market.

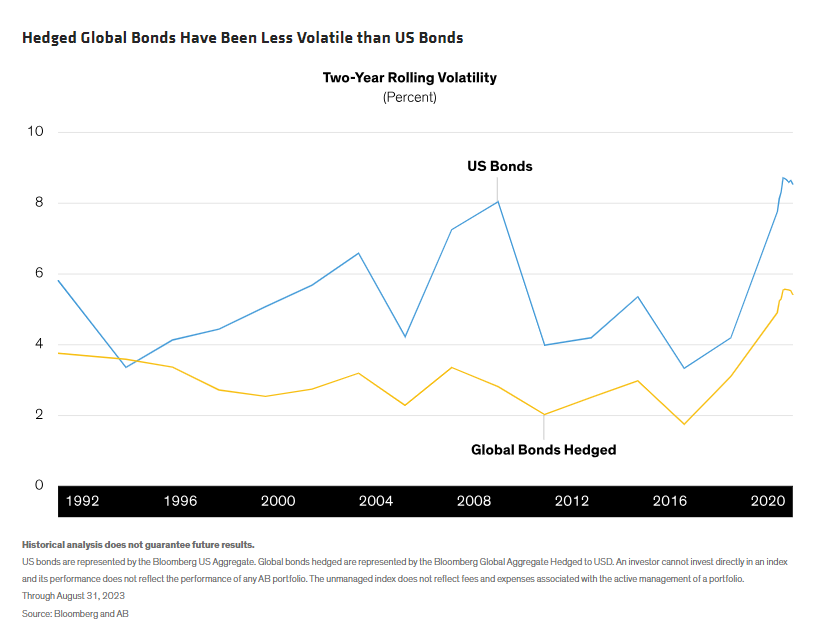

Historically, the hedged global bond market has generated higher returns with less volatility than the US bond market. For example, over the 30 years ending August 31, 2023, the Bloomberg Global Aggregate Index (hedged into US dollars) posted an average annualized return of 4.8%, versus 4.6% for the Bloomberg US Aggregate Index. And it did so with less volatility (Display).

That’s not all. Both the US and global bond markets provide a nice offset to the volatility of US stocks. Between February 1985 and August 2023, the US bond market and hedged global bond market both averaged very low correlations to the S&P 500, at 0.18 and 0.17, respectively.

But the real power in global bonds comes during extreme down periods for stock markets. During months when US stocks fell by more than one standard deviation, US bonds saw correlations to the S&P 500 fall to –0.06, while the correlations of hedged global bonds to stocks fell to –0.13.

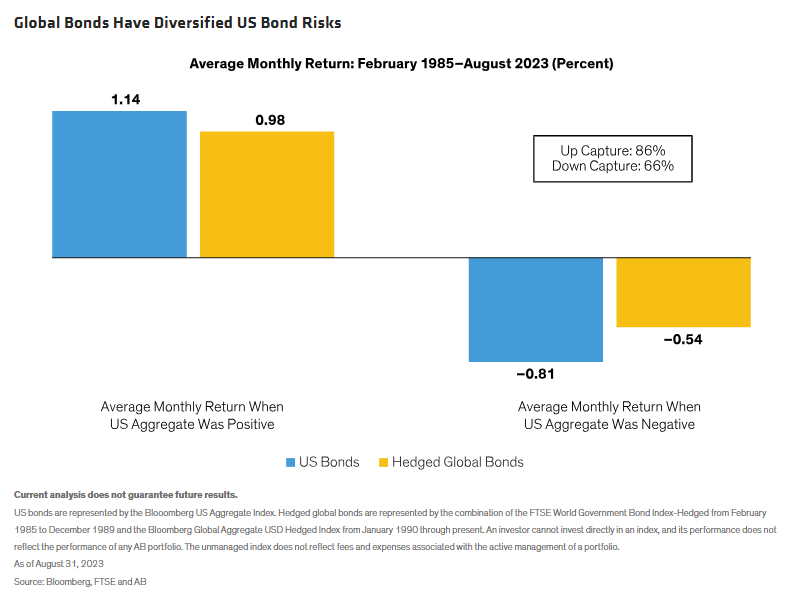

Lastly, bond investors didn’t miss out on US bond market rallies by investing in global markets. But they also didn’t concede as much when US bond markets fell. In other words, global bonds have historically provided attractive up/down capture ratios versus the US bond market (Display). Since 1985, during months when US bonds rallied, hedged global bonds captured 86% of positive returns. Conversely, when US bonds sold off, hedged global bonds preserved more capital, experiencing just 66% of that downturn.

3. Hedging into US dollars can boost low yields.

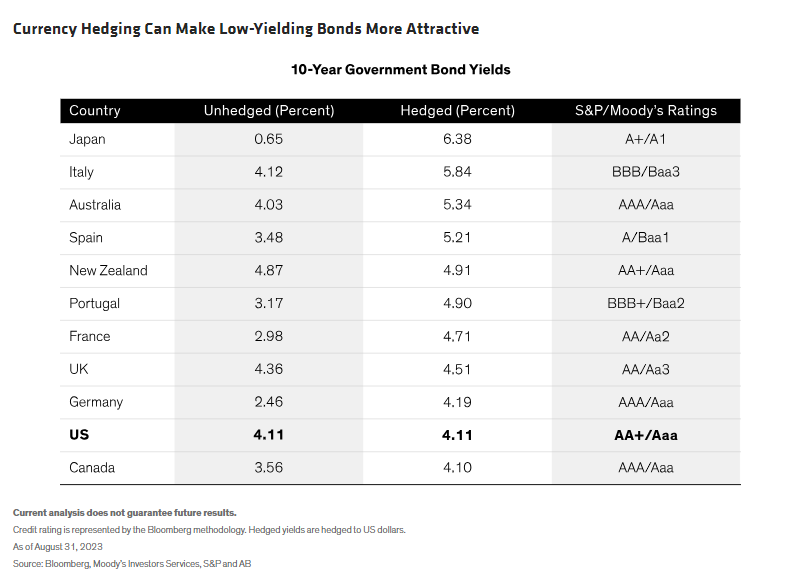

Why invest globally when so much of the global government bond market is trading with lower yields? Because, depending on the differences between countries’ short-term interest rates, currency hedging can raise a bond’s yield.

Hedging foreign currency back into US dollars accomplishes two things. First, it lowers the volatility of a global bond portfolio while preserving global bonds’ diversification benefits. Second, in today’s markets, the currency hedge leads to higher yields (Display).

In fact, on a hedged basis, nearly all non-US government bonds provide higher yields than the US today. For example, at the end of August, currency hedging into US dollars lifted the low-yielding Japanese Government Bond yield from 0.7% to 6.4%—227 basis points above the 10-year US Treasury yield.

The key is actively managing these exposures because hedging relationships change. Thankfully, hedging can be implemented cheaply and effectively with currency forwards and futures. In fact, the currency forward markets are among the most liquid markets in the world, making transaction costs very small. And, of course, relative yield is not the only consideration when making investment decisions.

In short, active investors should keep the full range of global bond options on the table—and stay nimble to take advantage—especially in today’s environment. Given its return, volatility and diversification advantages, as well as its unique opportunities for adding alpha, we think an allocation to global bonds makes sense for US investors.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© AllianceBernstein

Read more commentaries by AllianceBernstein