The September Federal Reserve meeting provided few surprises, but ongoing uncertainty about the Fed's next move may mean more volatility ahead.

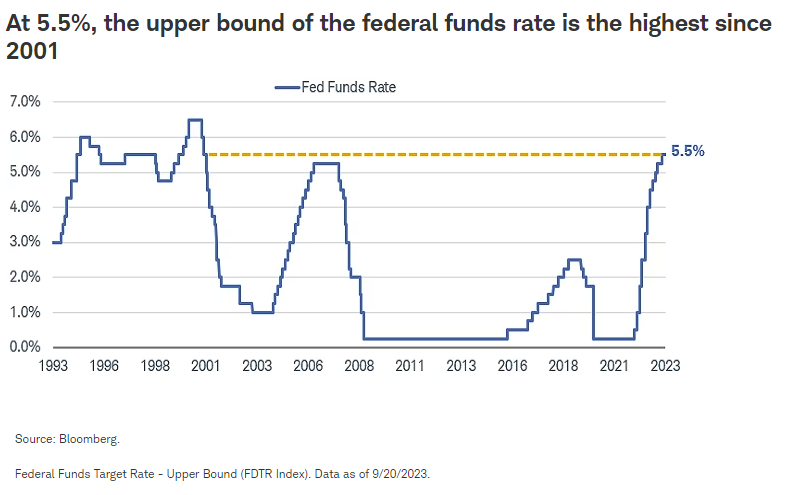

As expected, the Federal Reserve left its key policy rate—the federal funds rate—unchanged in September at a range of 5.25% to 5.5% but signaled that another rate hike later this year is the consensus view. The overriding message from the Fed is that it will continue to keep rates high until inflation comes down. This "higher-for-longer" message reflects a high level of uncertainty at the Fed about what it will take to move inflation sustainably lower.

Statement changes

The Federal Open Market Committee (FOMC) made a few modifications to its statement. It noted that economic growth was expanding at a solid pace, an upgrade from the previous statement that said activity was expanding at a "moderate" pace. It changed its description of the labor market, highlighting that job gains have slowed, as opposed to the "robust" job gains noted in June. In describing inflation, the Fed said inflation remained elevated, which should be no surprise considering that most inflation readings remain well above the Fed’s target.

Are we there yet?

The big question facing the markets is: Are we at the peak in the federal funds rate for the cycle, or are there more rate hikes ahead?

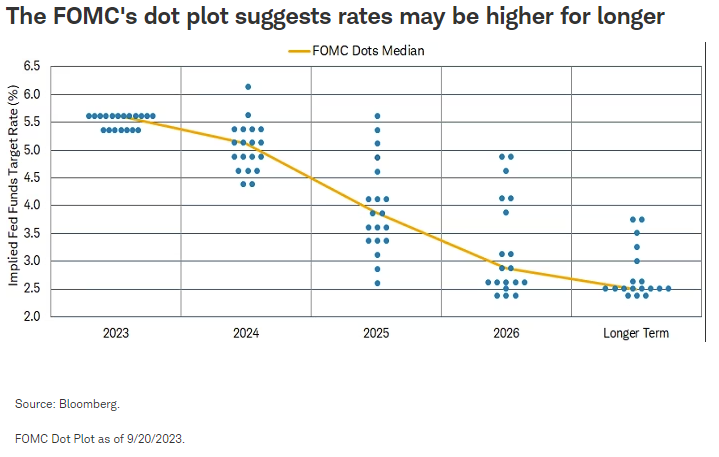

Based on the "dot plot," which summarizes projections of Fed members about where the policy rate is going, the consensus still looks for one more rate hike this year, and the size of rate cuts in 2024 diminished somewhat. The dot plot is a chart that records each Fed official's projection for where the federal funds rate will be at the end of each year, as you can see in the chart below.

The median dot for next year suggests a year-end rate of 5.1%, compared to a median projection of 4.6% at the June meeting—a 50-basis-point difference. Likewise, the year-end fed funds rate projection for 2025 was revised up to 3.9% from 3.4%. In other words, Fed projections suggest a "higher-for-longer" interest rate environment.

The longer-run projection was unchanged at 2.5%.

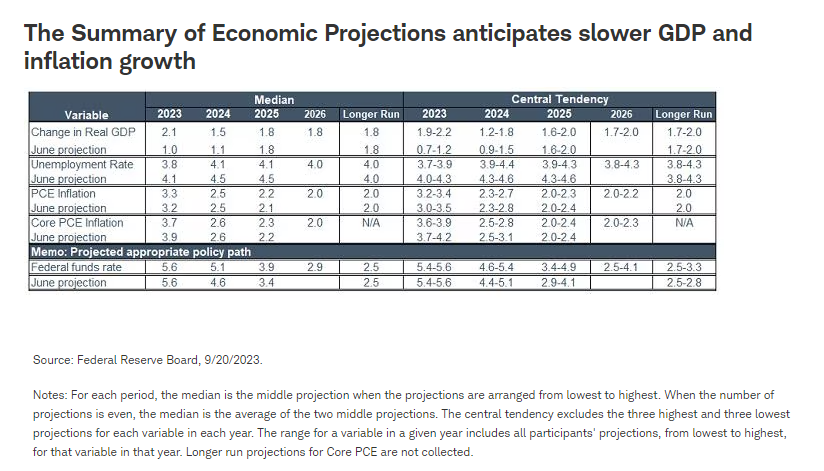

The Summary of Economic Projections (SEP) indicated that the Fed is looking for gross domestic product (GDP) growth and inflation to slow over the next year. Although the 2023 and 2024 GDP projections were revised higher from June, the committee is projecting growth to slow from 2.1% this year to 1.5% next year. The unemployment rate projections were also revised higher.

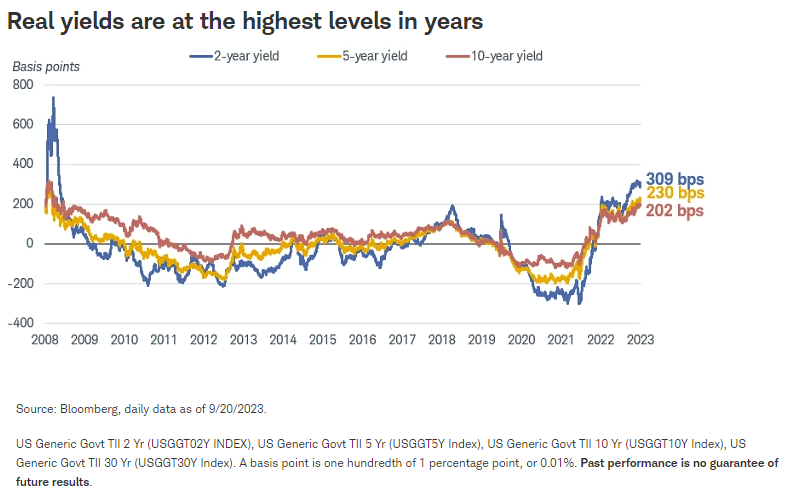

Based on Fed Chair Jerome Powell's comments after this meeting, the Fed doesn't appear confident about reaching its goal of 2% inflation in the near term, but does believe policy is currently "restrictive," or tight enough to slow growth and inflation. He was referring to the high level of real yields—adjusted for inflation—which have reached levels not seen since 2008. High real yields tend to dampen consumer spending and business investment.

What's next?

It's worth noting that even if the Fed is done with its rate hikes, monetary policy is still "tight." Leaving short-term nominal rates at current levels as inflation falls will send real yields—adjusted for inflation—higher. In addition, the Fed is still in the process of reducing its balance sheet by allowing bonds it holds to mature without replacement. The Fed has signaled that the process is likely to continue even when it shifts to lowering the fed funds rate. Watching to see how all of these policy measures play out will likely keep the Fed on hold until Q2 of next year.

Yields fluctuated following the statement's release and into the press conference. The yield curve remains inverted, continuing the trend over the past year. As long as the Fed remains in tightening mode, we believe the yield curve will remain inverted.

As usual, Powell stressed that whether the Fed hikes again will depend on the incoming data. The committee is "data dependent." Despite the median dot projecting another rate hike this year, the market still isn't sure. According to the fed funds futures market, the implied probability of another hike this year is just 50%. But a higher-for-longer policy should, over time, bring inflation down toward the Fed's 2% target.

Overall, the Fed meeting provided few surprises. Bond yields rose modestly and stocks declined on the prospect of interest rates remaining high. Investors should prepare for a sustained period in which the markets will react to each incoming economic report to try to gauge what it will mean for Fed policy. That could mean more volatility ahead.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results.

Investing involves risk including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab