Schwab Market Perspective: Crosscurrents

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhile surface-level economic data appear resilient, details below the surface are mixed.

Although U.S. and European economic data have been resilient, there are signs that trends below the surface may not be as strong and stable as they appear. Leading employment indicators suggest that both U.S. and eurozone employment growth may be softening, supporting the idea that central banks may not need to hike interest rates again in this cycle.

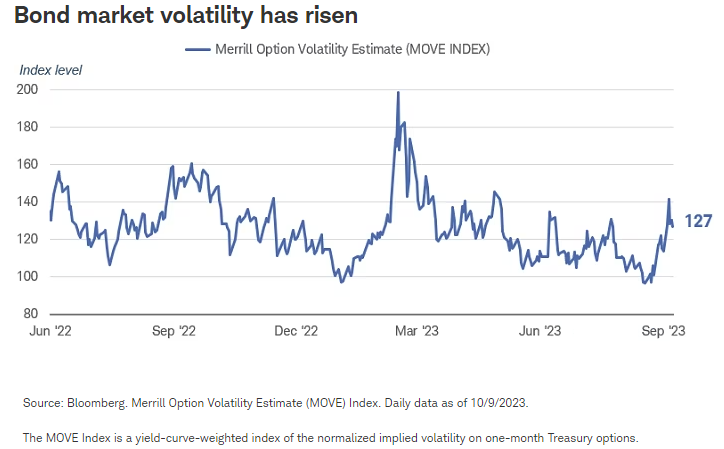

Meanwhile, Treasury yields are at their highest levels in years and bond market volatility has risen in recent weeks. Uncertainty about the direction of the Fed policy amid the mixed economic signals is keeping investors on edge.

U.S. stocks and economy: Churn below the surface

So far this year, there have been several crosscurrents within the economy and, importantly, the labor market—emphasizing the fact that while surface-level data look resilient, subsurface details are mixed at best. Case in point is the September U.S. jobs report, which blew past expectations with a gain of 336,000 jobs. Encouragingly, upward revisions to both August's and July's payroll data bucked the year-to-date trend of consistent negative revisions (typically a worrisome sign).

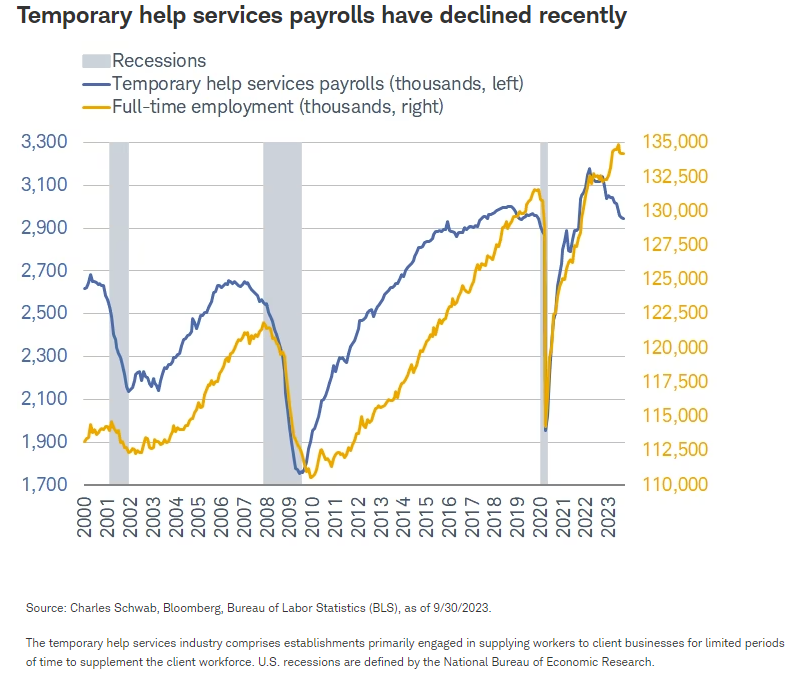

Yet, for all the positive aspects of the labor update, there are still several indicators that fail to support a robust jobs picture. For example, temporary help services payrolls—a leading indicator for overall employment—have fallen substantially from their all-time high, and the number of full-time positions seems to have peaked for now.

The decline in both metrics doesn't necessarily point to a looming, epic labor shock, but it does keep us on alert for a labor market that continues to weaken below the surface. If the contractions in temporary help and full-time employment ease, it will give us more confidence that the current slowdowns are merely post-pandemic normalizations, not recession signals.

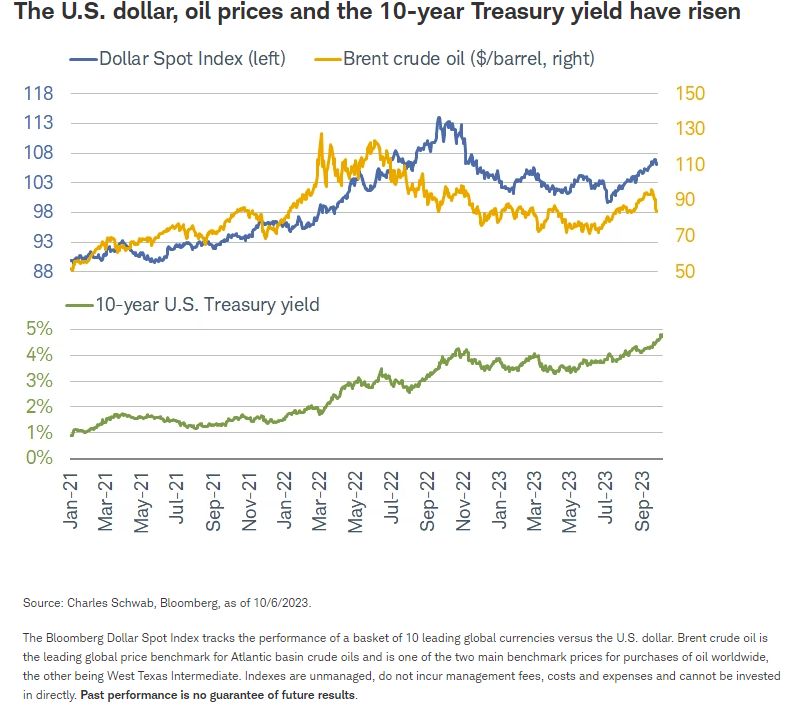

Admittedly, though, recession risks are still with us, evidenced by the recent triple threat of the increase in the value of the U.S. dollar, oil prices, and Treasury bond yields. All three metrics have moved higher since the summer, each putting downward pressure on key areas of the economy and market. All else being equal, a stronger dollar tends to weigh on foreign revenues for U.S. companies; higher oil prices sap spending power and are inflationary; and rising yields (particularly inflation-adjusted yields) are typically synonymous with tightening financial conditions.

Although oil prices have fallen significantly lately, volatility remains high. We continue to think the magnitude of the moves in interest rates, oil, and the dollar will matter more than the levels for the market, at least in the near term.

Undoubtedly, all three have contributed to the S&P 500® Index's decline since its July peak. While the rally up until that point was narrow in nature, the selloff has been broad-based—sparing virtually no corner of the market. The Energy sector has been an outperformer among its peers, but the strong tie to oil prices means it remains heavily exposed to macroeconomic swings.

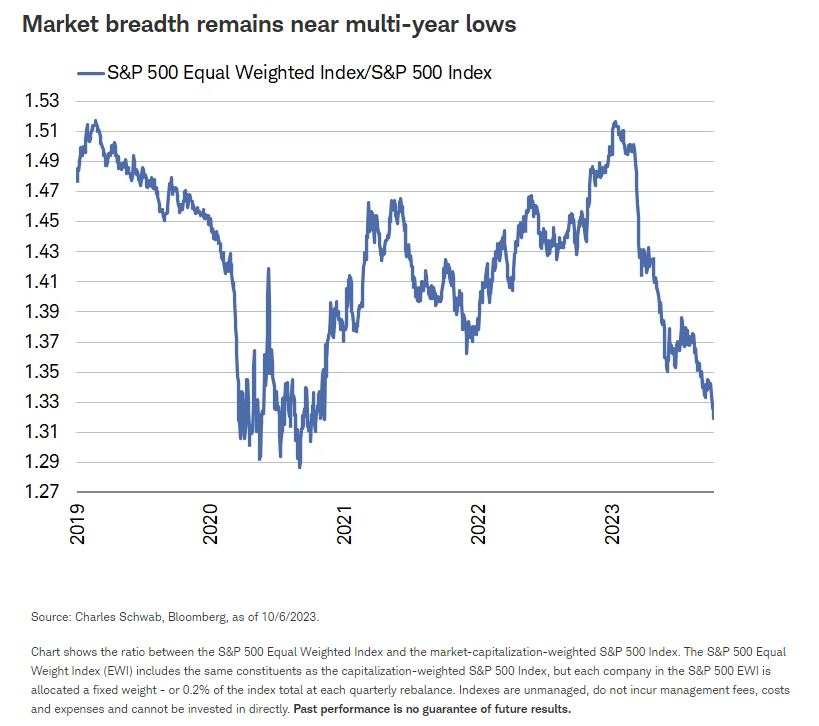

Much like parts of the economy and labor market, there are signs of deterioration under the market's surface. Not only are a handful of mega-cap stocks in the S&P 500 still accounting for most of the market's gain this year, the "average stock" continues to underperform. The performance of the S&P 500 Equal Weighted Index relative to the market-capitalization-weighted S&P 500 has recently fallen to its lowest level since November 2020. Any failure to turn would likely portend further weakness for stocks, especially if economic momentum falters.

Fixed income: Proceed with caution

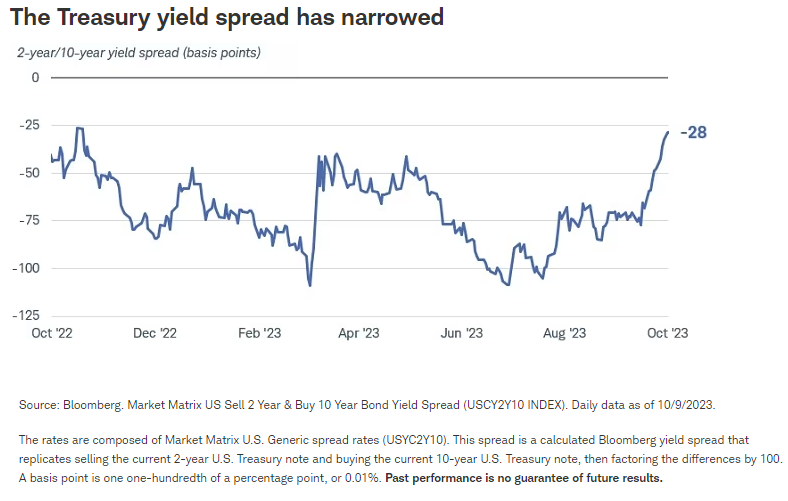

The fixed income markets are entering the last quarter of the year with Treasury yields close to the highest levels in nearly 15 years. It's notable that the surge in yields in recent months has been led by long-term bonds, a reversal of the trend seen earlier in the year. With economic growth proving more resilient than expected, yields have moved higher to reflect the shift in the Federal Reserve's September meeting projections that suggested the central bank would likely keep its policy rates "higher for longer." Consequently, yields for intermediate- and long-term bonds moved up to adjust for the prospect of continued high interest rates. The yield spread between two- and 10-year Treasuries, which had been deeply inverted by more than 100 basis points as recently as July, narrowed to about 30 basis points.

It's unusual for a flattening or "un-inverting" yield curve to be driven by rising long-term yields instead of falling short-term yields. In past cycles, a flattening yield curve was often an outgrowth of the Federal Reserve cutting short-term rates due to an approaching recession. However, very little about this interest rate cycle has been "usual." Economic growth slowed at the beginning of the cycle, but job growth has been resilient, even in the face of the most rapid pace of Fed rate hikes in modern times. Meanwhile, inflation has fallen and is approaching the Fed's 2% target level. The Fed's benchmark inflation measure—the deflator for personal consumption expenditures excluding food and energy, or "core" PCE—has slowed to a 2.2% annualized pace over the past three months.

Given all of these crosscurrents, it's not surprising that volatility in the bond market has moved up in recent weeks. Uncertainty about the direction of the Fed policy amid the mixed signals is keeping investors on edge.

Looking out to the rest of the year, we see the potential for the bond market to stabilize and yields to move moderately lower. A handful of Fed officials have begun to suggest that the impact of rate hikes to date is starting to show up in the slowing inflation. High borrowing costs have slowed the housing market, driven up delinquency rates on credit cards and auto loans and raised the default risk for low-credit-quality corporate bonds. Even if the Fed holds rates steady for a few months, it will still be tightening policy by continuing to reduce its balance sheet. It has already shed more than $1 trillion in bonds in the past few months.

There is still a risk of one more rate hike in this cycle, but we think that likelihood is diminishing. It will depend on the path of economic growth and inflation, but with volatility picking up and inflation low, the Fed runs the risk of overdoing its tightening and triggering a recession or a financial market problem. If we're correct that the Fed is at or near the end of its tightening cycle, then bond yields should begin to move lower in the fourth quarter and into 2024. There will likely continue to be a lot of volatility, however, so just like the Fed, investors should proceed with caution.

Global stocks and economy: Europe's labor outlook

Currently, Europe's job market is strong and so is wage growth. However, we expect that to change soon, which should allow the European Central Bank (ECB) to keep interest rates on hold and perhaps even begin to cut rates later next year.

Eurozone employment now stands at an all-time high, with 5.3 million more jobs than before the pandemic, according to Eurostat data. At the same time, 10.9 million people are unemployed in the eurozone, 1.3 million fewer than before the pandemic. The unemployment rate is now 6.4%, in line with the all-time low set in June. Yet, leading indicators of the labor market in Europe are showing signs that this strength may soon ease:

- In Germany, the number of people who have filed unemployment claims rose for an eighth straight month in September, according to the Federal Statistical Office of Germany.

- The number of reported job vacancies in Germany continued to slide in September.

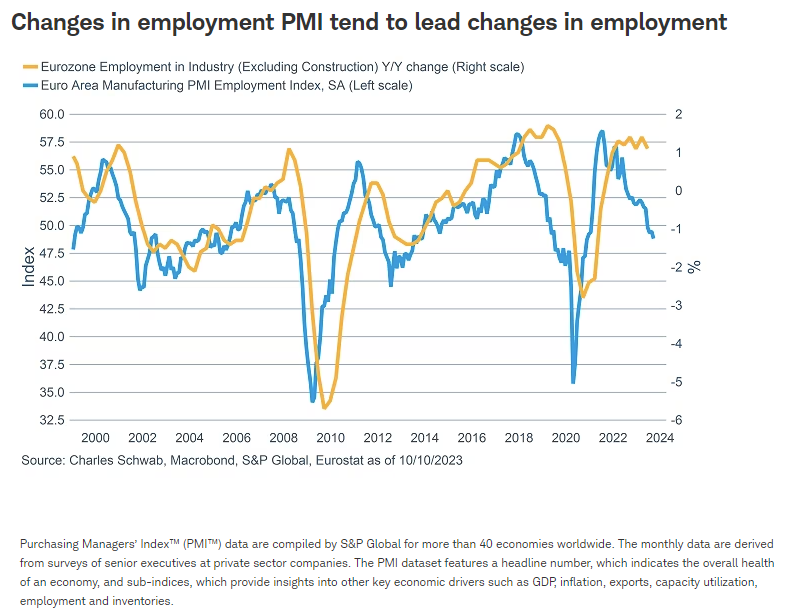

- The manufacturing employment Purchasing Managers' Index (PMI) points to a fall in employment in the coming months. Changes in the employment PMI tend to lead changes in employment by six to nine months, as you can see in the chart below.

- Europe has four times as many services jobs as manufacturing jobs, per Eurostat. The former strength in services employment appears to have started to weaken. The services PMI employment index was below 50 (the level that separates expansion from contraction) in Germany in September and in Italy in August and has come down sharply in recent months in France and Spain, consistent with a worsening outlook for services employment.

- European company management communications on earnings calls and shareholder presentations reveal a rising trend of mentions of job cuts (including phrases like reduction in force, layoffs, headcount reduction, employees furloughed, downsizing, personnel reductions) along with a falling trend in mentions of labor shortages (including phrases like labor shortages, inability to hire, difficulty in hiring, struggling to fill positions, driver shortages).

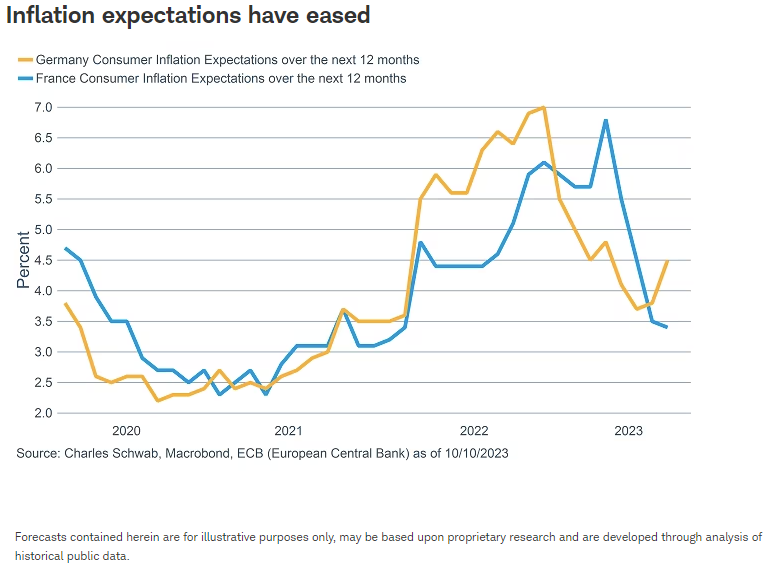

A low unemployment rate implies higher wage growth, which could force the ECB to continue to hike rates, and consequently put more downward pressure on the economy and stock market. Worryingly, wage growth has remained stubbornly high in Europe even as it has eased in the United States. Having peaked later in Europe than in the U.S., higher inflation gave workers the opportunity to demand larger pay rises in a tight labor market. Looking forward, European households' expectations for inflation over the next 12 months has already fallen sharply. If headline inflation continues to recede over the coming year as we expect, it seems likely that inflation expectations will track lower, prompting workers to eventually settle for lower pay increases.

Early signs of easing wages have appeared in Indeed's wage tracker for Europe (derived from job postings on Indeed.com), which has reported lower wage growth in July and August. If the unemployment rate remains low and inflation continues to fall, there may be little need for further rate hikes by the ECB.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. All expressions of opinion are subject to changes without notice in reaction to shifting market, economic, and geopolitical conditions.

Data herein is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Indeed Wage Tracker measures growth in wages and salaries advertised in Indeed job postings in eight advanced economies: France, Germany, Ireland, Italy, the Netherlands, Spain, the UK, and the US.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All