Tight lending standards and rising yields, along with concern about an approaching turn in the business cycle, have put opportunistic credit in the spotlight. But what, exactly, does opportunistic credit mean? Here’s how we look at it—and what we think it may offer investors.

It may be helpful to think of opportunistic credit as an investment in dislocation. Put simply, it’s a strategy that seeks to capitalize on periodic disruptions across public and private credit markets that can cause assets to become mispriced. The nature of these dislocations can vary widely—some can persist while others are fleeting—and managers’ ability to generate returns depends on being able to identify them.

In public markets, dislocations tend to be cyclical in nature and can cause investors to paint an entire asset class with a broad brush. Should rising interest rates spark a sudden widening in high-yield corporate bond spreads, for instance, traditional mutual fund or exchange-traded fund managers may have to exit less liquid positions and reduce overall market exposure in a hurry to limit losses and maintain daily liquidity.

An opportunistic credit investor who can hold semi-liquid and illiquid assets might decide to step in and buy bonds at a discount from those desperate to sell, then wait for prices to rebound. Those who do this well, in our view, can increase their chances of delivering excess return relative to traditional public market credit investments by tapping into illiquidity premia that generally aren’t available to traditional credit investors.

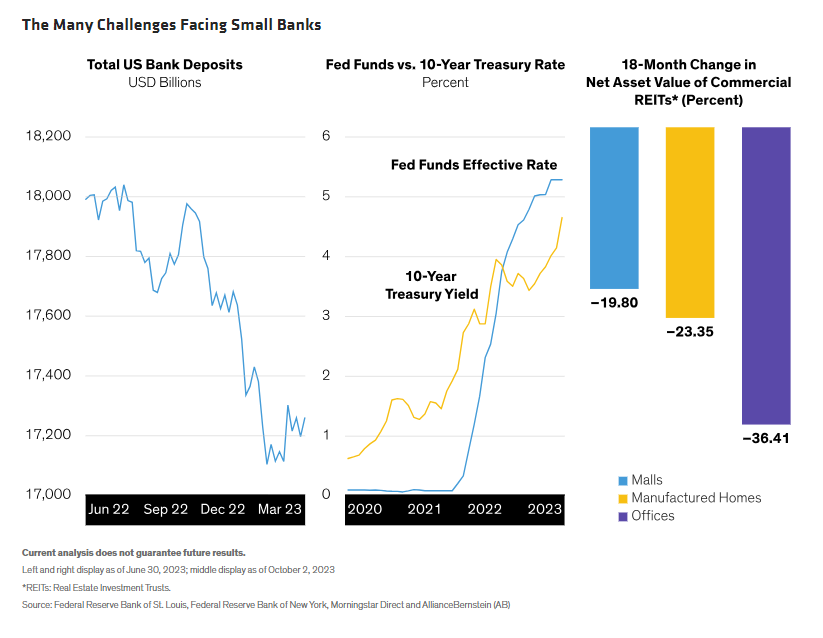

On the private side, dislocations typically take more time to develop and can last longer, potentially creating more enduring return opportunities. For example, large US banks have steadily reduced many types of consumer and commercial lending since the global financial crisis, leaving mid-sized regional banks to fill the gap.

But originating and holding those loans to maturity has become more difficult today for these smaller banks. Many of them are wrestling with a steady decline in deposits, a rising cost of capital (Display), exposure to troubled commercial real estate investments and a thick book of loans originated at yesterday’s low rates.

An opportunistic credit manager might see this as an opportunity to acquire loans from banks at a discount and sell them later at a profit. Another might decide to provide capital that private, non-bank lenders can use to originate new loans at prevailing higher rates. The opportunity extends well beyond commercial real estate as banks seek to clean up their balance sheets and originate new loans.

A Strategy for All Seasons

What sets opportunistic credit apart from other types of credit investing? First, these strategies are not tied to a single market or sector, so they can deploy capital to attractive opportunities over the course of a full cycle. We think of it as a “go anywhere approach,” enabling them to serve as an all-weather strategy.

Second, they offer the potential for capital appreciation. As we’ve seen, it isn’t unusual for opportunistic credit investors to own deeply discounted securities. This creates capital appreciation opportunities while offering high levels of income, increasing an investor’s total return potential.

Finally, the diverse set of holdings across public and private markets may enhance diversification beyond what a purely public or private credit strategy typically offers and may help to mitigate downside risk.

More than Just Income

In our view, integrating a more opportunistic approach into existing investment portfolios has the potential to generate higher overall income with lower drawdowns.

For income-oriented investors, it offers diversification of interest rates and credit and broader exposure to the economy. For traditional 60/40 investors, it can provide a simple way to selectively add privately sourced investments, which offer less liquidity than public assets, but higher potential returns. And for investors already comfortable with alternative strategies, it can provide diversification through access to consumer credit, which may complement the private market exposure found in commercial real estate and direct lending.

For investors who can carve out the space in their allocations, we believe opportunity may be waiting.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© AllianceBernstein

Read more commentaries by AllianceBernstein