Why Go Long When Short-Term Bonds Yield More?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith the Federal Reserve poised to change direction, investors who have been investing in very short-term securities may soon face "reinvestment risk."

Given the shape of the yield curve today, one of the most common questions we receive is, "Why should I buy a longer-term bond when I can get a higher or similar yield with a shorter-term one?"

It may seem counterintuitive, but it can make sense to buy a bond or certificate of deposit (CD) with a longer time to maturity but a similar yield vs. one with a shorter maturity. The reason is that an investor can have greater control over their cash flows, rather than being subject to reinvestment risk—that is, the risk of having to reinvest a maturing security at a lower interest rate in the future. This may be especially worth considering now, when the Federal Reserve appears poised to halt, or at least slow, the series of short-term rate hikes it began in 2022.

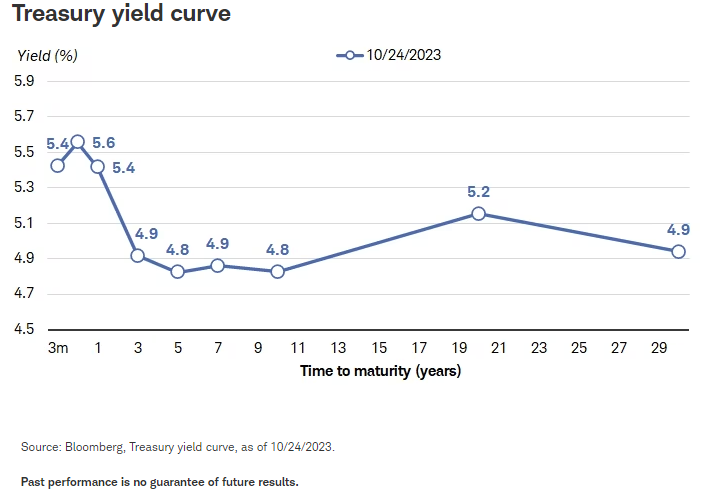

A primer on the yield curve

The yield curve is a line that plots yields relative to the length of time they have to maturity. It is a snapshot in time. Yield curves can (and frequently do) shift their shape. The most-tracked yield curve is the Treasury yield curve, but there are many other yield curves—for example, those that capture yields in corporate and municipal bonds and CDs.

The Treasury yield curve is usually upward-sloping, meaning longer-term securities yield more than shorter-term securities. This makes sense, because investors often demand higher yields for locking their money up for a longer period. However, it's not the case today: Parts of the Treasury yield curve are inverted, meaning shorter-term bonds are yielding more than longer-term bonds. This is largely because the Fed has been pushing short-term rates up for the past year and a half, in an effort to contain inflation.

Shorter-term bonds are subject to greater reinvestment risk

All of this leads us to the central question: Why invest in a longer-term bond when you can get a similar yield with a shorter-term one?

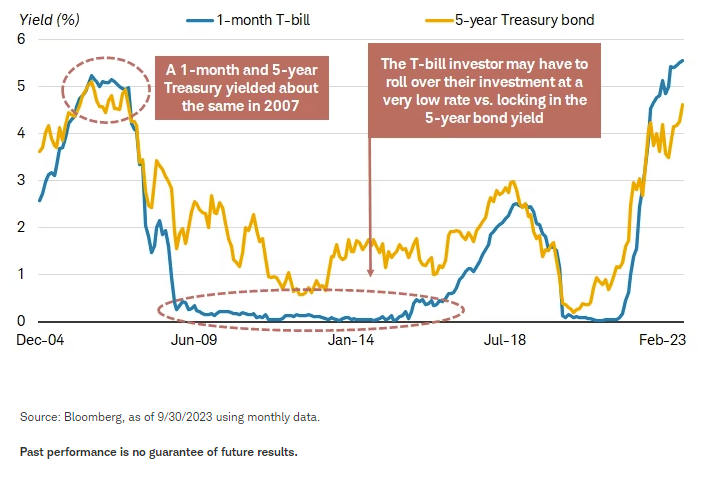

In two words: reinvestment risk. To illustrate how this works, consider an example using one-month and five-year Treasuries in February 2007. (Although this time period was right before the 2007-2008 global financial crisis, we're only using it for illustration purposes; we're not predicting a similar situation.) At that time, both yielded about 5%. However:

- The investor who purchased one-month Treasury bills would have to repeatedly repurchase a new T-bill each time their Treasury matured, and would therefore invest at the current market rate.

- The investor in the five-year Treasury bond would have locked in an annual income of 5% for the subsequent five years.

Fast-forward to the start of 2009, by which time yields on short-term Treasuries had fallen sharply because the Fed aggressively cut rates due to the global financial crisis. The T-bill investor would now be faced with the prospect of rolling over their investment at a rate that is much lower than the original 5%, whereas the five-year Treasury bond investor would continue to earn 5% for another three years.

Yields don't move in lockstep

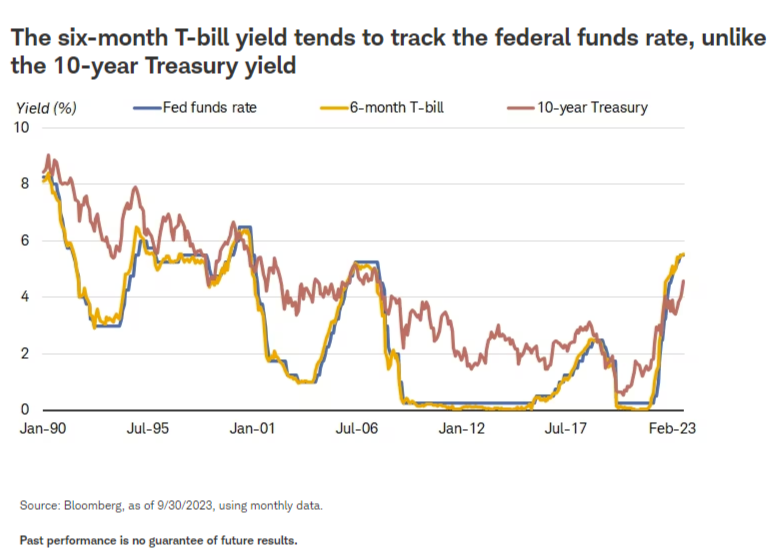

A common misconception is that when the Fed raises the federal funds rate, all yields rise in lockstep. This isn't usually true. As illustrated in the chart below, yields for short-term securities, like a six-month Treasury bill, typically closely track the federal funds rate, whereas longer-term rates are more tied to the outlook for growth and inflation which can be influenced by the market's interpretation of what the Federal Reserve will do.

Going forward, it's likely that the Fed will hold interest rates at an elevated level for a period of time to further cool inflation. The market now expects that the Fed will cut interest rates in the later part of 2024 but that view has changed as the economic data has developed.

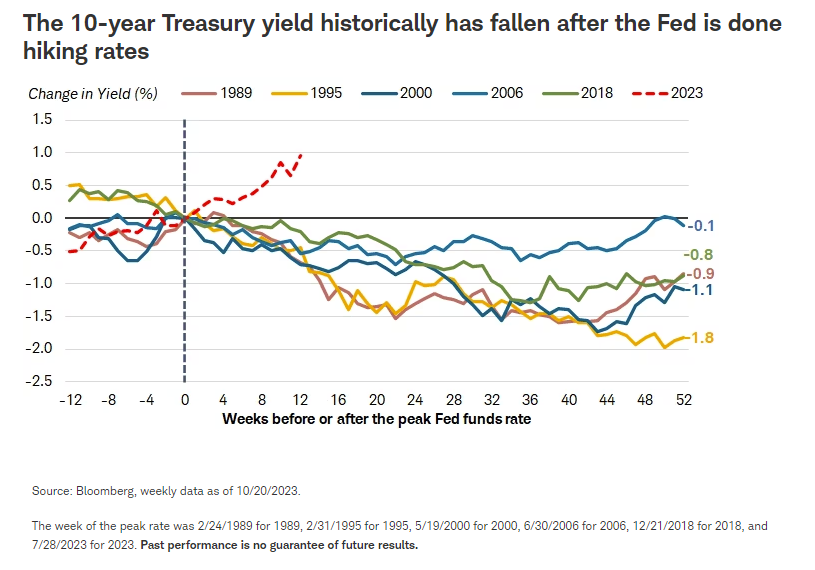

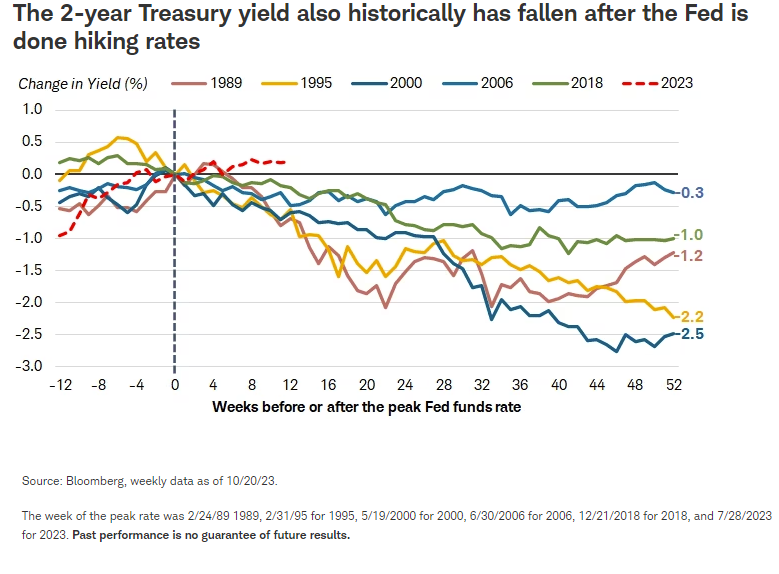

Historically, the Fed has paused hiking rates when it believed that the economic growth was about to contract and inflation to slow. In response to the worsening economic background, longer-term Treasuries usually decline, as illustrated in the chart below, which shows the change in the 10-year Treasury yield in the weeks before and after the Fed hiked rates to the peak level for that cycle. The horizontal bar is the week in which the Fed hiked the federal funds rate to the peak level. For example, in 1989 the Fed increased the federal funds rate to 9.75%. At the time, the 10-year Treasury was at 9.4%. Over the next year, as the economy slowed, the 10-year yield fell to 8.5%, a decline of nearly 1%.

It's not just longer-term yields that have fallen after the Fed is done hiking rates. Short-term rates also have declined after the Fed has hiked rates to the peak level. That makes sense because short-term yields generally move in advance of what the Fed is expected to do and once the Fed reaches the peak level, it eventually cuts rates as the economy cools. This cycle has been unique in that rates have risen since the last rate hike, assuming that it was in July. However, going forward, we would not be surprised if we're near the peak in rates. The implication is that investors who have been investing in very short-term securities may soon face the prospect of both lower short-term and long-term rates.

Total returns may favor intermediate-term bonds going forward

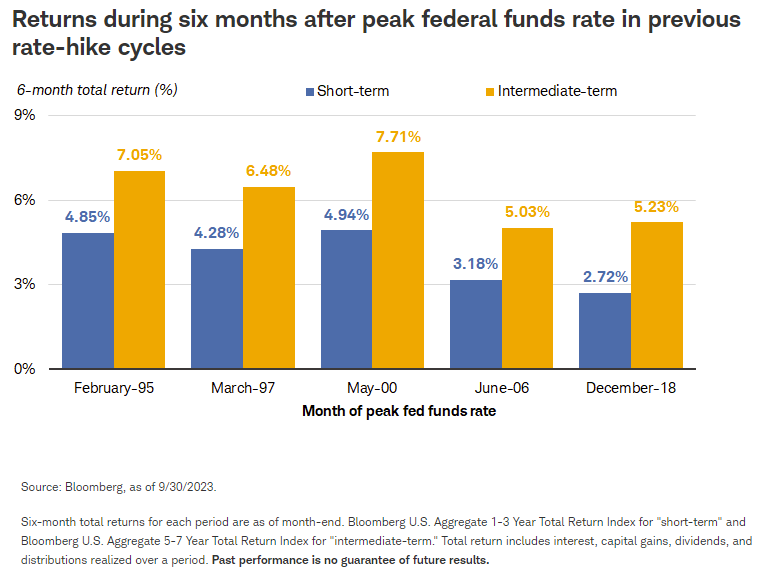

The suggestion to consider longer-term securities relative to shorter-term ones doesn't just apply to investors in individual bonds or CDs. Investors who prefer bond funds, such as mutual funds or exchange-traded funds (ETFs), should take notice, too. Historically, intermediate-term bonds have outperformed shorter-term bonds when the Fed is done hiking interest rates, as illustrated in the chart below.

For example, in December 2018 the Fed hiked rates for the ninth and final time in that rate-hiking cycle. Over the following six months, an index of intermediate-term bonds returned 5.23%, relative to 2.72% for an index of short-term bonds. This is an important point for investors who invest in bond funds rather than individual bonds, because if this pattern holds, intermediate-term bonds may outperform shorter-term ones going forward, since the Fed is likely close to being done hiking rates.

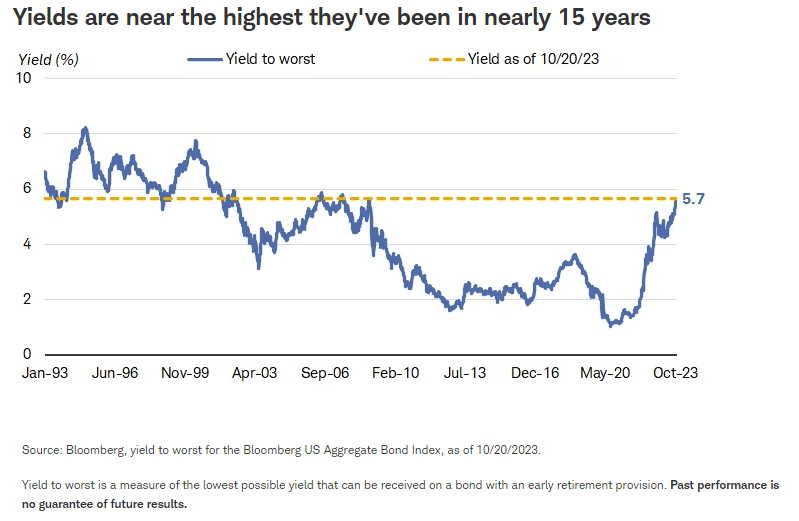

Why not just wait in for yields to move higher?

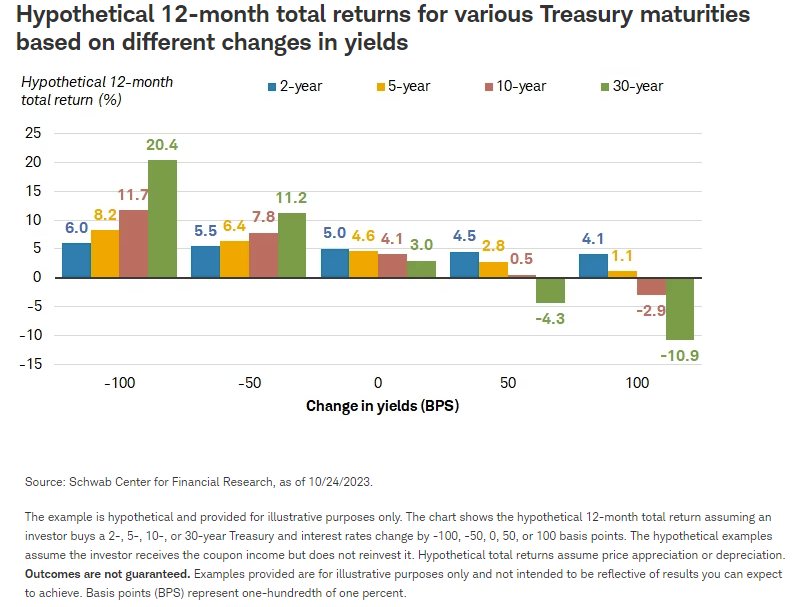

If the Fed isn't expected to cut rates until later in 2024, it may be tempting to wait in cash and see if yields move even higher, but we think this is a bad strategy. It's been a very difficult year for high-quality fixed income investments, which has caused some investors to contemplate waiting until things get better. We believe going forward, returns should be more favorable than what they have been recently because yields already have moved sharply higher. Returns for fixed income securities can be broken down into two primary sources—coupon income and changes in prices. As yields have moved sharply higher over the past year and a half, this provides a much larger cushion for returns in case yields continue to march higher. For example, as illustrated in the chart below, even if the 10-year Treasury yield moves higher by another 50 basis points, or 0.5%, we estimate that an investor's 12-month total return would still be positive.

Additionally, it may be tempting to wait for the "peak" in yields but we won't know if the peak has happened until long after it's occurred. Additionally, even if yields have some further upside from here, we believe that we are at very attractive levels and investors shouldn't wait to try to time the peak in rates.

What to consider now

We believe that the recent move up in longer-term yields presents an opportunity for investors who have been hesitant to invest in longer-term bonds. We suggest extending duration to lock in those yields. For investors who prefer individual bonds or CDs, two strategies to consider are a ladder or a barbell. Both strategies have the potential benefit of holding some shorter-term bonds while also investing in some longer-term bonds.

For investors who prefer funds, Schwab clients can log in to research individual municipal bonds, view pre-screened municipal bond exchange-traded funds (ETFs) on Schwab's ETF Select List® or municipal bond mutual funds on Schwab's Mutual Fund OneSource Select List®. For additional help in selecting an appropriate solution for your needs, a Schwab Financial Consultant or Fixed Income Specialist can help.

Investors should consider carefully information contained in the prospectus, or if available, the summary prospectus, including investment objectives, risks, charges, and expenses. You can request a prospectus by calling 800-435-4000. Please read the prospectus carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Bloomberg U.S. Aggregate 1-3 Years Index tracks bonds with 1-3 year maturities within the flagship US Aggregate Bond Index. Total return includes interest, capital gains, dividends, and distributions realized over a period.

The Bloomberg U.S. Aggregate 5-7 Years Index tracks bonds with 5-7 year maturities within the flagship US Aggregate Bond Index. Total return includes interest, capital gains, dividends, and distributions realized over a period.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

A bond ladder, depending on the types and amount of securities within the ladder, may not ensure adequate diversification of your investment portfolio. This potential lack of diversification may result in heightened volatility of the value of your portfolio. As compared to other fixed income products and strategies, engaging in a bond ladder strategy may potentially result in future reinvestment at lower interest rates and may necessitate higher minimum investments to maintain cost-effectiveness. Evaluate whether a bond ladder and the securities held within it are consistent with your investment objective, risk tolerance and financial circumstances.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, Charles Schwab & Co., Inc. does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All