Inflation is a touchy subject, and given there are many ways to analyze it, investors should take note of the nuances that exist within the data.

It's difficult to find a subject that has captured the zeitgeist of the post-pandemic world more than inflation. For valid reasons, discussion about the rise in prices is all around us—whether it stems from Federal Reserve officials setting monetary policy, consumers facing strains at stores and the gas pump, or businesses boosting workers' wages.

This year, though, the conversation around inflation has demonstrably shifted. The pace of price increases has eased considerably relative to a year ago; most recently, the October consumer price index (CPI) report helped solidify some strategists' and analysts' conviction that the Fed is done hiking interest rates. Not only that, it has pushed many Fed watchers (and market participants) to start expecting rate cuts by as early as March 2024.

Inflation is a touchy subject, not least because there are many ways to frame and/or calculate it. If the pandemic-related surge taught us anything, it's that inflation is truly in the eye of the beholder. So, let's take a look at the many different ways one can measure the change in prices. Given this is a rather lengthy report, I'll state my conclusion early on: You can literally paint whatever picture you want with any subset of inflation metrics.

CPI of the beholder

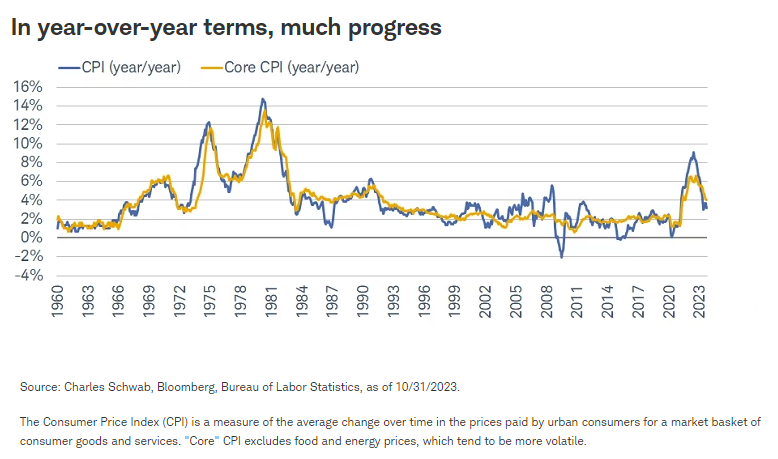

Starting with the most widely followed metric—CPI—the chart below shows one of the most common ways to look at inflation: the year-over-year percentage change in the index. As you can see, we've made remarkable progress over the past year after seeing a spike to the fastest inflation rate since the 1980s. While the trend has eased this year, CPI and core CPI (which strips out food and energy) are still hovering at rates that are likely too fast for the Fed to declare victory.

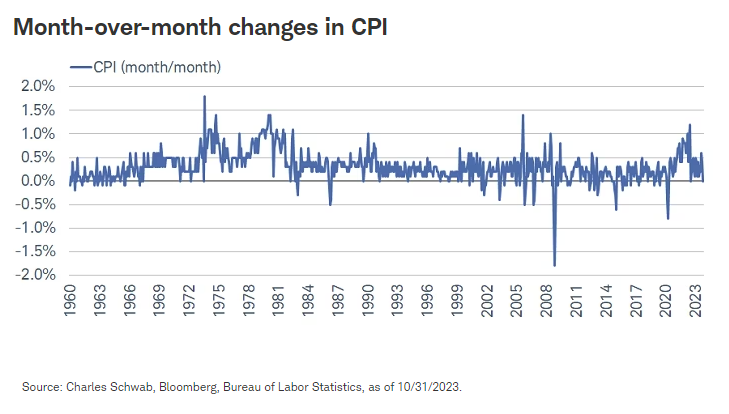

Sometimes, you'll read media headlines or articles that say prices rose or fell from the prior month, which likely means the month-over-month change is being cited. As you can see in the chart below, these are much smaller moves relative to the year-over-year changes shown in the prior chart. Case in point: As of October, CPI was unchanged from the prior month. If you're in the camp saying the inflation dragon has been slain, you can point to this and say we have no more inflation relative to the prior month.

Not so fast, though. The monthly inflation data are incredibly volatile, so it's tough to rely on those readings to construct a trend. To help smooth out that volatility, a common way analysts will look at trends is by measuring the change in prices over the past three months, then annualizing that figure to get a sense of what the increase would look like over a one-year period.

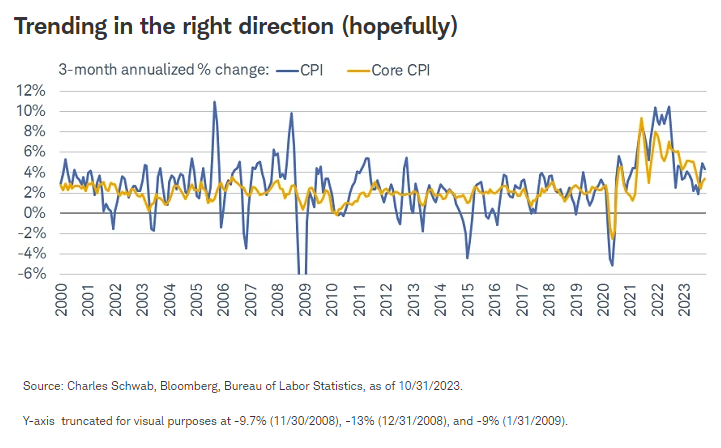

As shown below, doing that calculation for CPI and core CPI, you can see that the pace of price increases has eased considerably from the stressful peak in 2022. Even with both series, one can find an optimistic and pessimistic conclusion. An optimist will point to the considerable decline over the past year, while a pessimist will say that inflation is nowhere near the Fed's 2% inflation goal.

Main Street vs. Wall Street

We're skipping over an important aspect of inflation, though—and that is how the public views price increases. Now that we have a couple years' worth of survey data to look through, it's clear that consumers are generally upset with the increase in price levels relative to the pre-pandemic era.

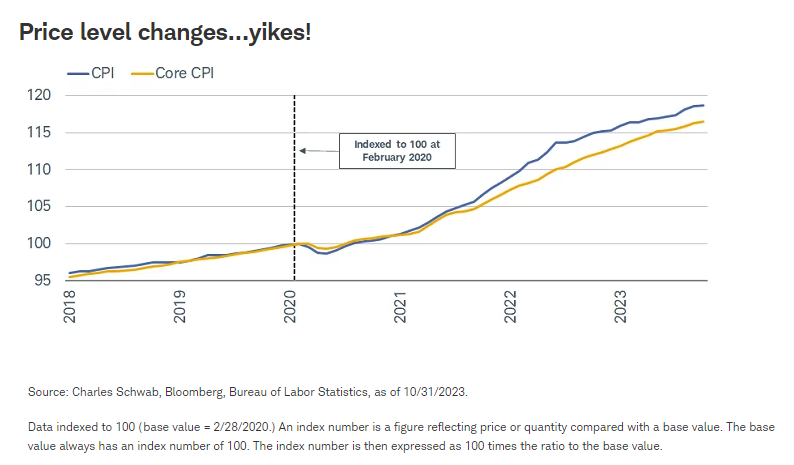

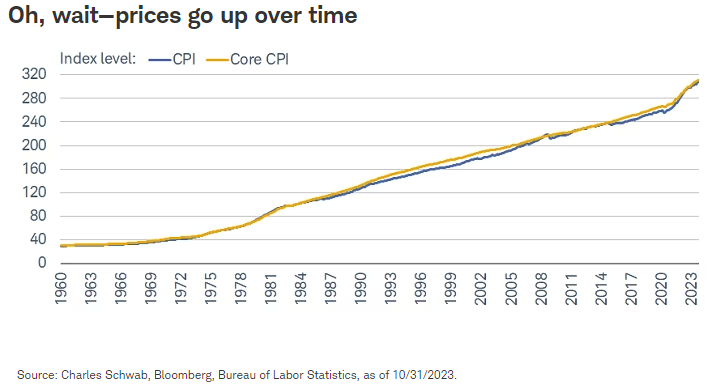

As shown in the chart below, looking at the change in the levels of CPI and core CPI since right before the pandemic began, you can see that prices are up by nearly 19% and 17%, respectively. It's unlikely that the average consumer is going to cheer about the year-over-year percentage change in CPI having come down to 3.2%. They likely care more about the fact that the prices they're paying for goods are considerably more expensive relative to a few years ago.

Here's the rub. Prices tend to increase over time. Zooming out and looking at the index levels for CPI and core CPI, you can see that they are not mean-reverting; that is, they historically have not returned to their long-term mean or average level. To be sure, there are periods when both lines were increasing at a faster pace—like in the 1970s and during/after COVID—but the pain associated with those moves likely only went away with time.

Is inflation still an issue?

For numerous reasons, the inflation debate has arguably never been as nuanced as it is today. Much of that is due to the nature of the inflation we've faced since the pandemic. The initial burst in early 2021 was ignited and exacerbated by the nature of the shutdowns and what they did to the global economy.

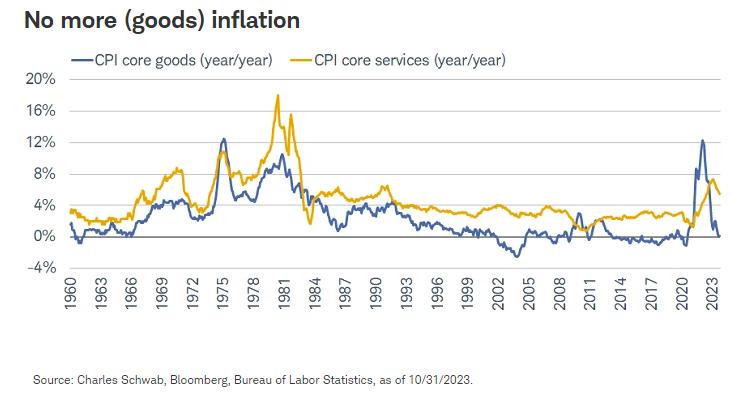

When much of the world was locked down, many consumers were driven to buy goods at the expense of services. With both fiscal and monetary stimulus measures helping preserve (and in some cases, boost) spending power—and a supply chain crisis in key manufacturing hubs like China—there was a perfect breeding ground for goods inflation to soar. As you can see in the chart below, the year-over-year change in core goods inflation spiked to the highest since the early 1970s. That was a painful move, but it was also relatively short-lived (dare I say, transitory), since that metric has plunged back to 0%. That move was driven by the broad reopening of the economy, when the world abruptly switched from mass goods to mass services consumption (the "revenge spending" we often hear about). As a result, core services inflation started moving up much later and has been stickier (meaning it's taking longer to move lower).

One of the reasons core services inflation has been sticky is because of shelter costs. The rent component of CPI is likely discussed the most these days, mostly because analysts think it's a controversial way to measure housing costs. The owners' equivalent rent (OER) portion of CPI is an imputed metric, which means it is derived from homeowners' assessments of how much they can rent their homes out for. Readers can arrive at their own conclusion as to why that might be controversial, especially because OER's weight in the CPI is hefty at nearly 26%. When you add in the other shelter components, the combined weight of housing as a category adds up to nearly 45% of CPI.

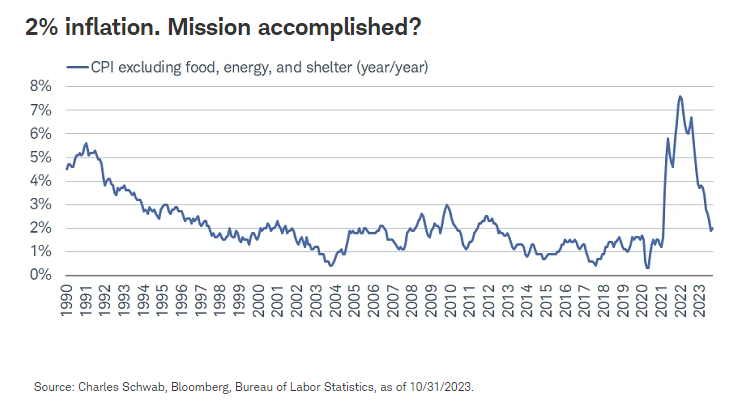

Because of that, many analysts will simply exclude the housing/shelter component from inflation metrics. Not only that, but they'll take out food and energy components, given those tend to be incredibly volatile over time. This leads to quips that go something like this: If you don't drive, heat your home or eat, inflation doesn't look bad…or, if you just take out the prices that are going up considerably, inflation doesn't look bad. As luck would have it, there is indeed a version of CPI that excludes food, energy, and shelter. Hey, look! We're back at 2%. Mission accomplished for the Fed?

Will the real core inflation please stand up?

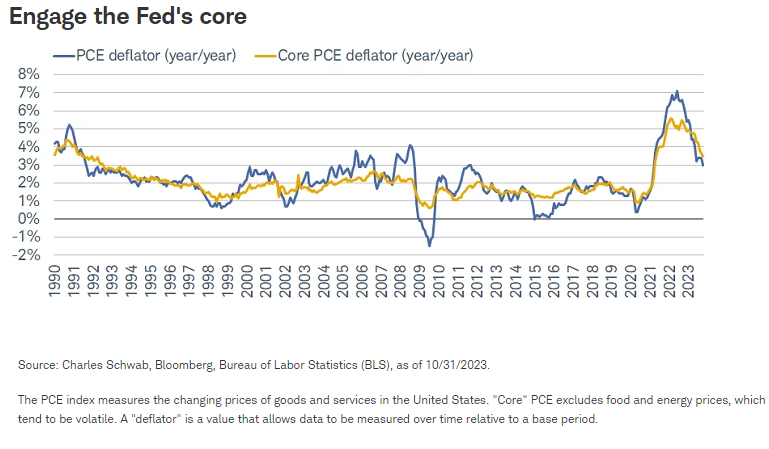

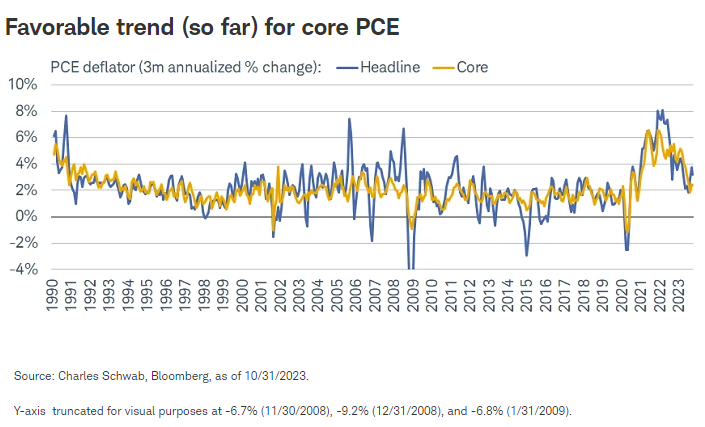

If only it were that easy. One of the difficulties in looking solely at CPI is that it isn't the specific inflation metric the Fed focuses on with regard to its 2% target. For the Fed, the core personal consumption expenditure (PCE) deflator is the metric in focus. As shown in the chart below, through October, the year-over-year percentage change in core PCE continued to ease but had only fallen to 3.5%, which is well above the Fed's 2% goal.

In some ways, the slowdown in core PCE inflation has been more aggressive than in core CPI. Looking at the three-month annualized change (like we did earlier), you can see that it actually slowed to exactly 2% in August. There was a bounce back to 2.4% in October, but for the most part, the extreme gains look to be behind us for now. So, here's another instance in which an inflation optimist can say that the inflation battle has mostly been won.

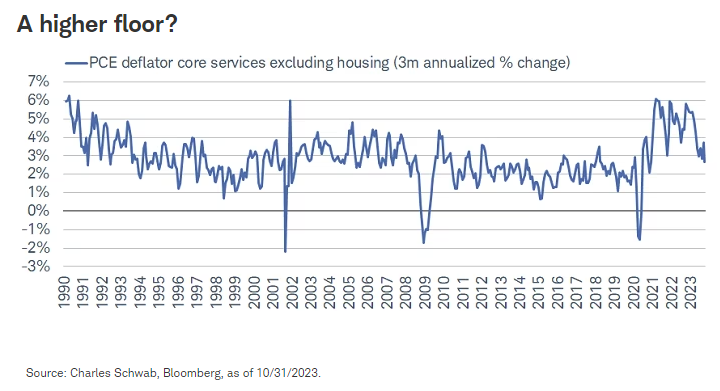

Not so fast (again). The shelter components I discussed within CPI also exist in the PCE inflation metrics. They're not nearly as weighty as they are in the CPI, but they're still a large presence. Even the Fed has acknowledged this. And given several real-time rent metrics show that rental price growth has slowed back to almost 0% (year-over-year), the Fed has decided to sharpen its focus on core services PCE excluding housing.

You can see that metric in the chart below, which shows the three-month annualized change. As of October, it did ease, but to 2.7% (slightly faster than core PCE). If you're viewing this negatively, you might say that it looks like we're settling around a higher average compared to pre-pandemic times. If you're viewing this optimistically, you'd take a lot of comfort that we're not seeing 6% gains like we did in 2021-2022 inflation spiral.

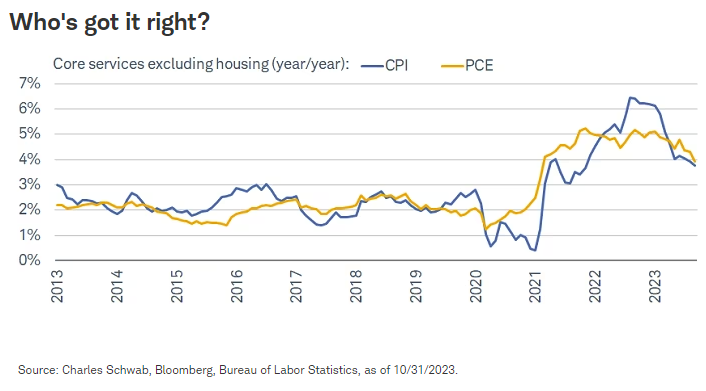

Since the kneejerk reaction of most consumers is not to look at a three-month annualized change, let's bring this back to the more common year-over-year change. Shown in the chart below is a comparison of the core services ex-housing versions of both CPI and PCE. What's fascinating is how much the two have diverged over the past couple of years. The trend in CPI will tell you that we've seen remarkable progress since the peak last year, from 6.5% to 3.8% (impressive!). However, over that same timeframe, the PCE version has only moved from 5% to 3.9% (not so impressive!). That's actually not terrible news, since it's the slowest rate since May 2021; but at the same time, it's still far from the Fed's target.

In sum

Paraphrasing my conclusion made at the beginning of this report, it's clear that one can paint any kind of picture with various subsets of inflation metrics to arrive at a conclusion that inflation is either still out of control or totally contained. It's a form of data manipulation, but in reality, data are always being manipulated (not in a nefarious way)—being shown in year-over-year, month-over-month, or three-month annualized terms. It depends on what kind of story is being told and, like most things in economics, it comes down to personal bias.

That's another major takeaway here—that inflation is deeply personal. My own inflation rate is not easing much these days, since I travel a lot, live in a city (New York) where rents are still rising swiftly, and consume more services than goods. Inflation is also largely dependent on geography. Case in point is the difference in CPI for major metro areas of late. Through October, the year-over-year change in Miami's inflation rate was 7.4%. For Baltimore, it was 2.2%; for Phoenix, it was 2.9%, per the Bureau of Labor Statistics.

One overarching conclusion from the panoply of charts I showed in this report is that we are still in a disinflationary trend—so, even though prices are still rising, they're doing so at a slower pace. While there might indeed be enough evidence for the Fed to refrain from additional interest rate increases, we'll need to do as the Fed does: Watch the incoming data. It's admittedly a fussy exercise, since there are so many economic crosscurrents these days, but that's the price we pay (no pun intended) for having lived through so many shocks over the past few years.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Supporting documentation for any claims or statistical information is available upon request.

Investing involves risk, including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab