Fixed Income Outlook: The Rocky Road Bond Market

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAlthough some volatility may continue, we believe interest rates have peaked. We expect lower Treasury yields and positive returns for investors in 2024.

The case for lower interest rates in 2024 is straightforward, but the path is likely to be rocky. We expect bond yields to decline in line with falling inflation and slower economic growth, but uncertainty about the Federal Reserve's policy moves will likely be a source of volatility. Nonetheless, we are optimistic that fixed income will deliver positive returns in 2024.

For illustrative purposes only.

Lower yields ahead

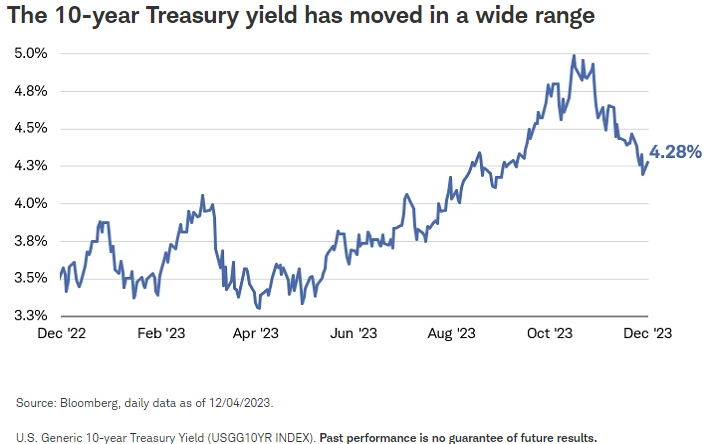

The action in the bond market has been anything but plain vanilla over the past year. Ten-year Treasury yields have spanned a huge range—from as low as 3.25% in April in the wake of the banking crisis to as high as 5.02% in October on surprisingly strong third-quarter economic growth. In 2024, we look for lower yields but expect bouts of volatility along the way, as markets continue to try to anticipate shifts in Fed policy. Assuming the Fed continues to lag market expectations for rate cuts, the market will be very attuned to every data point, likely causing yields to trade in wide ranges.

Nonetheless, we believe that both short- and long-term yields likely have peaked for the cycle and will continue to fall assuming inflation abates in 2024. In our view, much of the inflation driven by supply shortages early in this cycle has been corrected, but the full impact of the tightening in monetary policy by major central banks is still working its way through the global economy. Slower growth and less inflation pressure should be the result.

While intermediate- to long-term yields already have fallen significantly from the peak seen last October, we see more room for decline. The big questions revolve around the magnitude of the decline and the shape of the yield curve. Those trends will be driven by central bank policies.

However, we don't look for yields to fall back to the levels that prevailed in the aftermath of the 2007-2008 financial crisis or during the COVID-19 pandemic. In our view, the era of zero policy rates and quantitative easing has ended. A return to "normal" in the bond market would mean positive real yields during periods of economic expansion coupled with bouts of volatility as central banks allow markets to set rates.

Falling yields

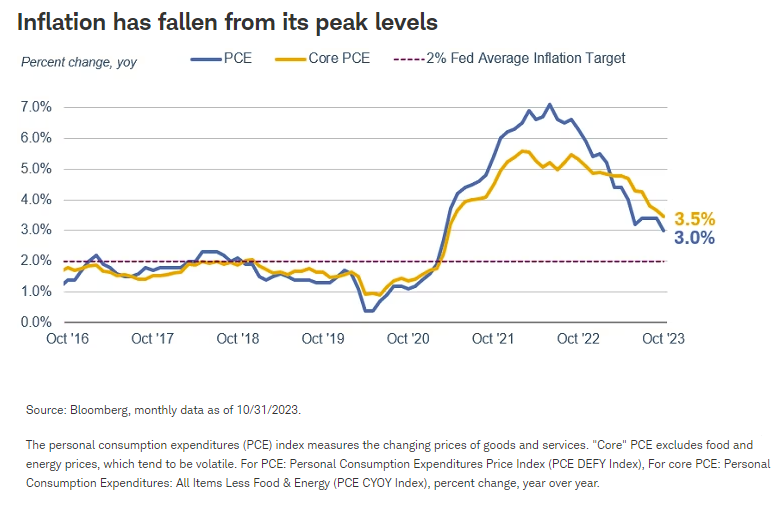

The Fed's policies to quell inflation involve raising interest rates and signaling it will keep them high until inflation falls back toward its 2% target, and quantitative tightening—or reducing the size of its balance sheet. So far, the process appears to be working, with inflation having fallen by half from its peak levels.

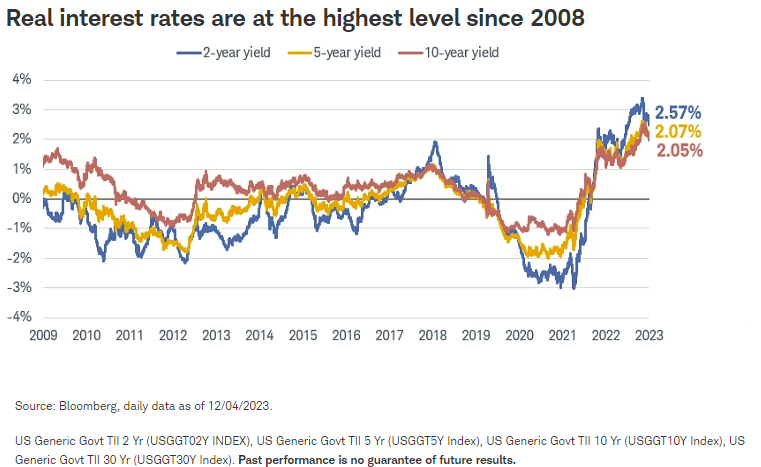

Pushing up interest rates rapidly and holding them steady as inflation falls has resulted in a sharp increase in "real" rates—that is, yields adjusted for inflation expectations. At current levels, real yields should be high enough to put a brake on the economy. High real interest rates make it more attractive for consumers to save than spend, and more difficult for businesses to borrow, hire, and invest. While consumer spending has been resilient during the past year, rising interest rates have slowed demand for durable goods, resulting in a downturn in the manufacturing sector. Recent data suggest that the pace of growth in the service sector is moderating as well.

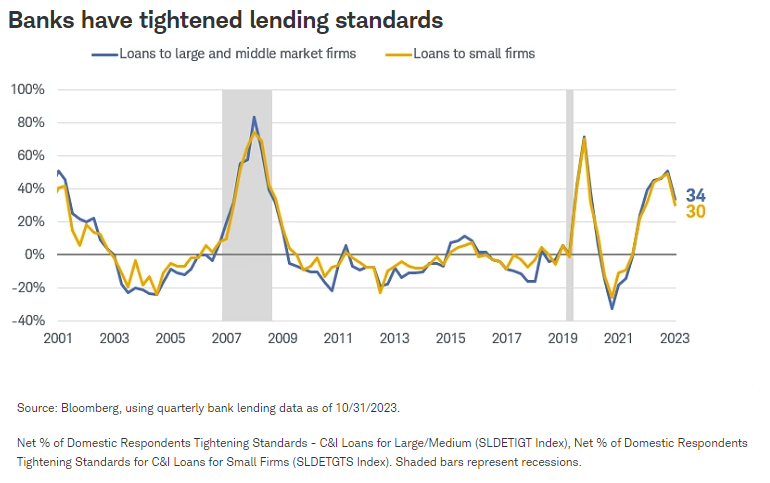

In addition to high real rates making borrowing more expensive, banks have tightened lending standards significantly in this cycle, limiting access to credit for both businesses and consumers.

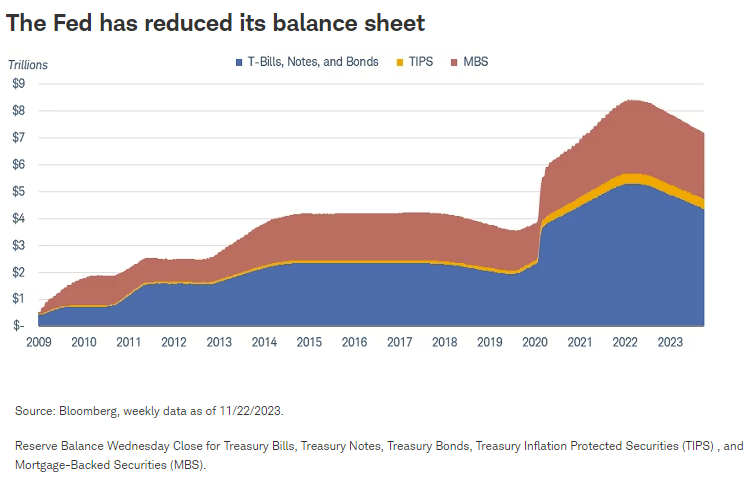

Moreover, the Fed intends to continue its quantitative tightening program—allowing bonds on its balance sheet to mature without reinvestment—even after it shifts to lowering interest rates. So far, that process has reduced the Fed's total holdings by more than $1 trillion.

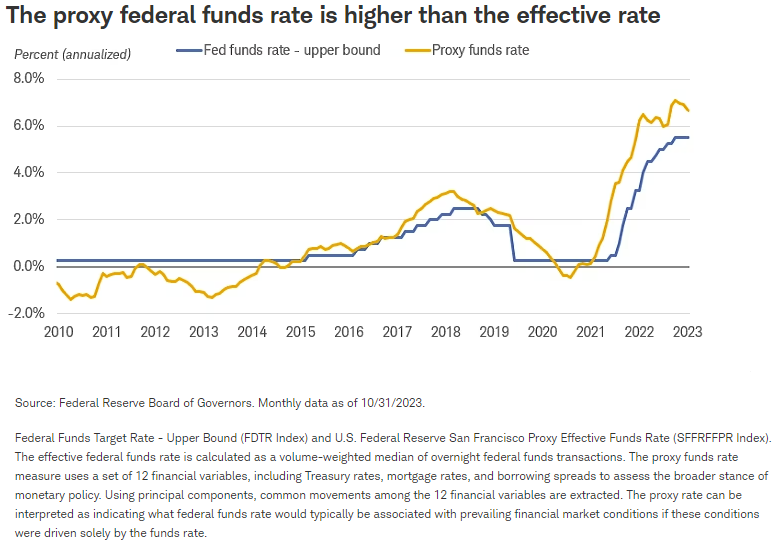

The federal funds rate, which guides overnight lending between U.S. banks, is currently 5.25% to 5.5%. However, the Fed policies combined—the "higher for longer" policy signal, quantitative tightening, and the cumulative rate hikes to date—are estimated to be the equivalent of pushing the federal funds rate to 6.7%, according to the "proxy funds rate" calculated by the San Francisco Federal Reserve Bank.

Lastly, this has been and continues to be a global tightening cycle, with central banks raising interest rates in most major and emerging market countries. The synchronized rate hikes are compounding the slowdown in domestic economic growth and inflation. As a result, the Organization for Economic Cooperation and Development (OECD) estimates that global gross domestic product growth will slow to 2.7% in 2024, slightly lower than in 2023 and significantly below the five-year pre-pandemic average of 4.6%.

What is the Federal Reserve's reaction function?

While the case for lowering interest rates seems clear to us, that's not necessarily true for everyone at the Federal Reserve. Having failed to recognize the need to tighten policy early in the cycle as inflation soared, the Fed continues to signal a willingness to keep policy tight for an extended period to make sure inflation falls toward its 2% target level.

This is a significant change in strategy. In past cycles, the Fed might already have started lowering rates in response to falling inflation, but this time around it doesn't want to squander the gains it has made to date. It is waiting for data to validate a shift in policy.

The message has been that short-term rates will be higher for longer, but without much detail. From recent comments by Fed officials, it appears that the majority is growing more confident that further rate hikes aren't needed. Most concur that the current 5.25% to 5.5% target range for the federal funds rate is sufficiently high to achieve their goals, although a few are holding out the potential for one more hike. We agree with the majority that the peak in rates has been reached.

However, we don't have much clarity about how much longer rates are going to remain high. The market has gotten ahead of the Fed in anticipating rate cuts a few times over the past year only to have to unwind those expectations, causing yields to rebound sharply.

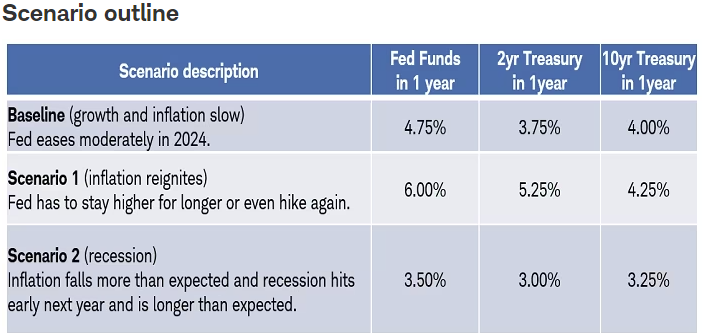

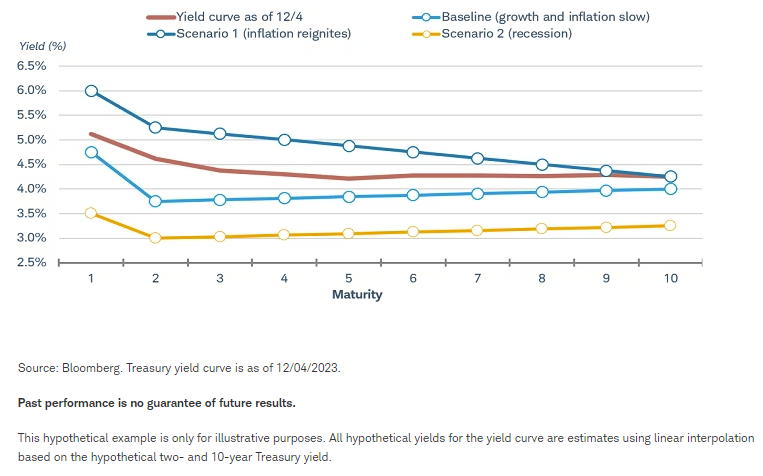

Given the uncertainty about the timing and magnitude of potential Fed rate cuts, we've constructed three hypothetical scenarios for 2024 and assessed the likely impact on Treasury yields and the yield curve.

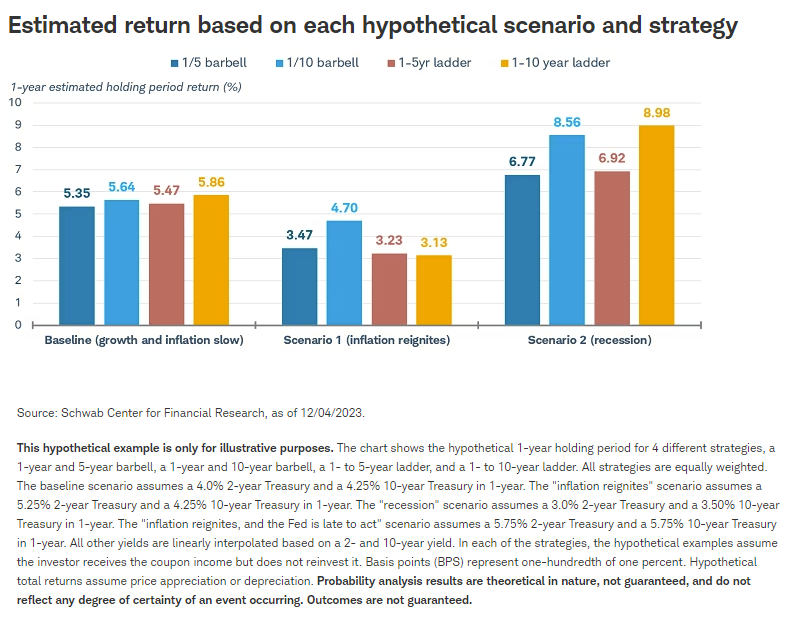

Baseline: Growth and inflation slow

Our base-case scenario is for three rate cuts of 25 basis points each, starting mid-year, bringing the upper bound of the target range for fed funds to 4.75%. This scenario reflects the Fed's reluctance to cut rates pre-emptively in this cycle and is generally in line with current market pricing. It would likely mean that the economy's growth rate slows down, but a recession is avoided. We would expect the yield curve to remain inverted as 10-year Treasury yields fall to 4% or lower while the federal funds rate stays elevated. However, two-year yields would likely decline below 10-year yields.

Scenario 1: Inflation reignites

This scenario—which we believe has a low probability of occurring—calls for one more 25-basis-point rate hike by the Fed and an extended period of high rates in response to rebounding inflation. We estimate that the yield curve would likely stay inverted due to the tightening in monetary policy, but yields would stay elevated for all maturities.

Scenario 2: Recession

This scenario assumes the Fed cuts rates by up to 150 basis points in the next 12 months due to the onset of recession. Rapid Fed rate cuts would likely mean that the yield curve would steepen due to short-term rates falling faster than long-term rates.

For fixed income investors, the good news is that the range of hypothetical potential outcomes for some commonly used strategies suggests positive returns. The chart shows the hypothetical returns for bond ladders and barbells with different maturities. We looked at one- to five-year and one- to 10-year ladders and barbells using Treasuries.

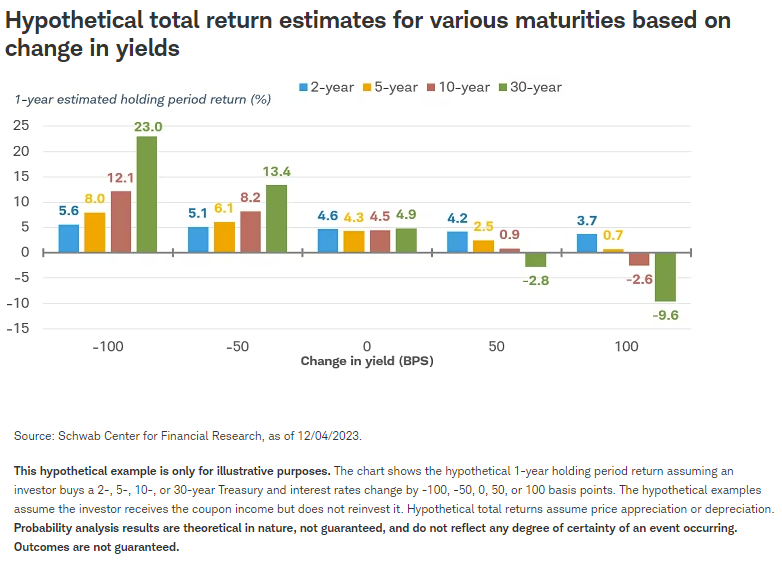

With starting yields in the 4% to 5% region, positive returns are likely, because the income generated from the coupon should offset price declines in most scenarios. If yields do rebound in 2024 relative to expectations, it would take a substantial increase to generate a negative total return, with the biggest impact on the longest duration bonds.

No matter what the scenario in the fixed income markets in 2024, it's likely to come with volatility. This cycle has been different in many ways from previous cycles and the road from high inflation to low and stable inflation likely won't be smooth. Every economic data report and Federal Reserve meeting or comment could cause an outsized reaction in the markets. However, in the long run, the trend in inflation is the biggest factor driving interest rates, and that is currently headed in the right direction. With the peak in rates likely behind us and high starting nominal and real yields, we look for lower yields and positive returns for investors.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Supporting documentation for any claims or statistical information is available upon request.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

A bond ladder, depending on the types and amount of securities within the ladder, may not ensure adequate diversification of your investment portfolio. This potential lack of diversification may result in heightened volatility of the value of your portfolio. As compared to other fixed income products and strategies, engaging in a bond ladder strategy may potentially result in future reinvestment at lower interest rates and may necessitate higher minimum investments to maintain cost-effectiveness. Evaluate whether a bond ladder and the securities held within it are consistent with your investment objective, risk tolerance and financial circumstances.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation. Treasury Inflation-Protected Securities are guaranteed by the US Government, but inflation-protected bond funds do not provide such a guarantee.

Mortgage-backed securities (MBS) may be more sensitive to interest rate changes than other fixed income investments. They are subject to extension risk, where borrowers extend the duration of their mortgages as interest rates rise, and prepayment risk, where borrowers pay off their mortgages earlier as interest rates fall. These risks may reduce returns.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, political instability, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Market trends are shifting – is your investment strategy keeping pace? Join industry experts as they delve into the equity and bond markets, offering insights into the 2024 outlook. Register for our Market Outlook Symposium, on December 14th at 11 am ET. Click here.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits