Top 5 Global Risks of 2024

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThere are many risks for 2024 including those that are an ever-present part of investing and not unique to the outlook for any particular year. We've highlighted our top five.

History shows us that the biggest risks in a typical year aren't usually from out of left field (although that sometimes happens, as it did in 2020 with the COVID-19 outbreak). Rather, they are often hiding in plain sight. As goes one of my favorite quotes often attributed to Mark Twain: "It ain't what you don't know that gets you in trouble, it's what you know for sure that just ain't so." Risk appears when there is a very high degree of confidence among market participants in a specific outcome that doesn’t pan out—for better or worse. So, by identifying the unexpected, here are our top global upside and downside risks to our base case outlook for next year, in no particular order:

- Lingering Inflation

- Rate hikes offsetting rate cuts

- China rebounding

- Artificial intelligence (AI) productivity boost

- Election surprises

Lingering inflation

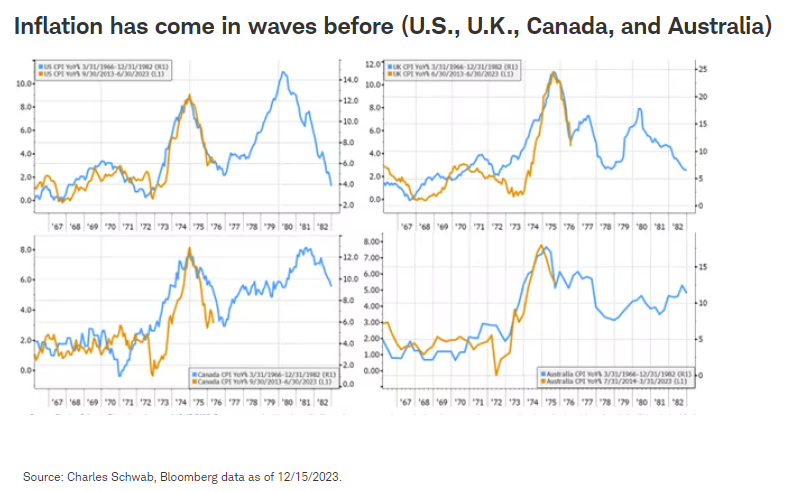

While it seems likely that central banks may declare victory over inflation in 2024 and enact rate cuts, inflation may not be as controlled as officials would like. Inflation, measured as a year-over-year rate of change, has historically come in waves. Four countries with long histories of consumer price index (CPI) inflation data, the United States, United Kingdom, Canada, and Australia, saw waves of inflation in the 1970s, as you can see in the chart below that we've been updating all year showing the path from the mid-60s to the early 1980s in blue. The current path of inflation in orange from 2013 to present has echoed that period's path, so far.

Now, the current period is not exactly like the series of shocks driving inflation in the 1970s. There are many differences, and inflation is not expected to surge to new highs in the coming years. But the 1970s dramatically illustrates inflation's tendency to be volatile, even after peaking. Volatility in the path of inflation could raise uncertainty about the direction of economic growth and central bank policy responses, fueling investor nervousness. It's possible that upticks in inflation could delay central banks from declaring the start of rate cuts, which the stock market seems to be eagerly anticipating given last week's rally on the signal of a Federal Reserve pivot to cuts next year, when the futures market moved to price in six 25-basis-point cuts in 2024.

What could cause inflation to not quickly and steadily return to central bankers' 2% targets in 2024? Potential causes include tight global labor markets, volatile energy prices, and supply chain problems. Specifically, potential supply chain problems may result from two key shipping "chokepoints," the Panama Canal and the Bab-al-Mandeb Strait in the Red Sea. Forty percent of global cargo traffic flows through the Panama Canal while 10% of global seaborne oil flows through the Bab al-Mandeb area. Due to severe drought, the Panama Canal Authority has announced it will be restricting the number of vessels by more than 50% of normal volume by February. Commercial ships have recently come under attack in the Red Sea, prompting the world's second biggest container shipping company, Maersk, and oil giant BP to halt ship traffic through the strait. Additionally, the International Longshoremen's Association serving East and Gulf Coast ports is threatening to strike in October 2024.

Rate hikes

There are signs of a new era for the Bank of Japan (BOJ), who may finally consider rate hikes after 17 years. Any rate hikes in Japan could offset some of the excitement over rate cuts by other major central banks in 2024. The BOJ will hold its next Monetary Policy Meeting on December 19. While we expect the BOJ to maintain the status quo at this week's meeting, there is potential for a signal that rate hikes are coming in early 2024 (for more on what this shift may mean for investors read: Bank of Japan: End of an Era?).

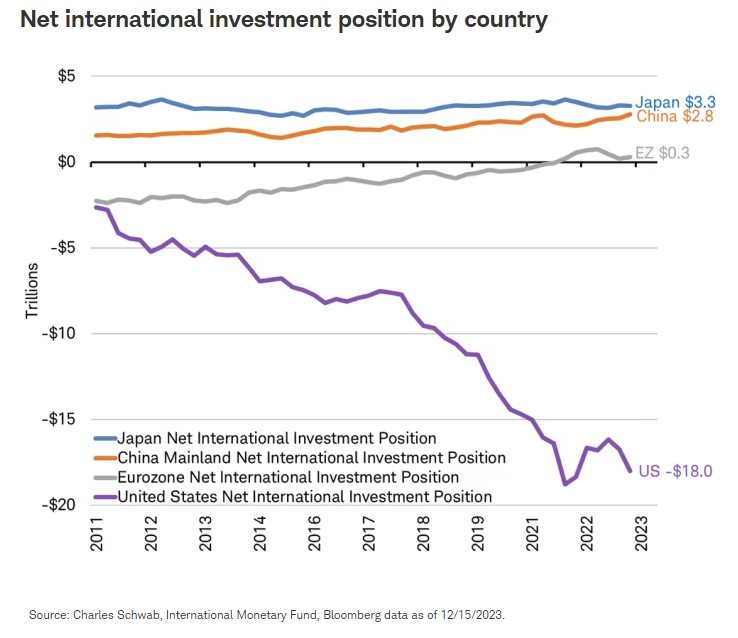

For over a decade, the Bank of Japan's policy has enabled Japan to be an important source of investment funding; Japanese investors net outflow to the rest of the world totals over $3 trillion, including holdings of more than $1 trillion in U.S. Treasuries. Any rate hikes over the next year hold the potential to prompt Japanese investors to sell foreign assets and bring them home, a move already incentivized by a stronger currency, higher interest rates, and the 27% gain in Japan's stock market in 2023, measured by the MSCI Japan Index.

Japan's Ministry of Finance announced international securities transactions data for November 2023, which revealed that Japanese investors turned net sellers of foreign bonds for the first time since July, and net sellers of foreign stocks for the first time since August after the central bank signaled a shift in policy at the October meeting. If the size and speed of the reversal of over a decade's worth of investment flows is greater than we anticipate in 2024, it could weigh on non-Japanese investments.

China rebound

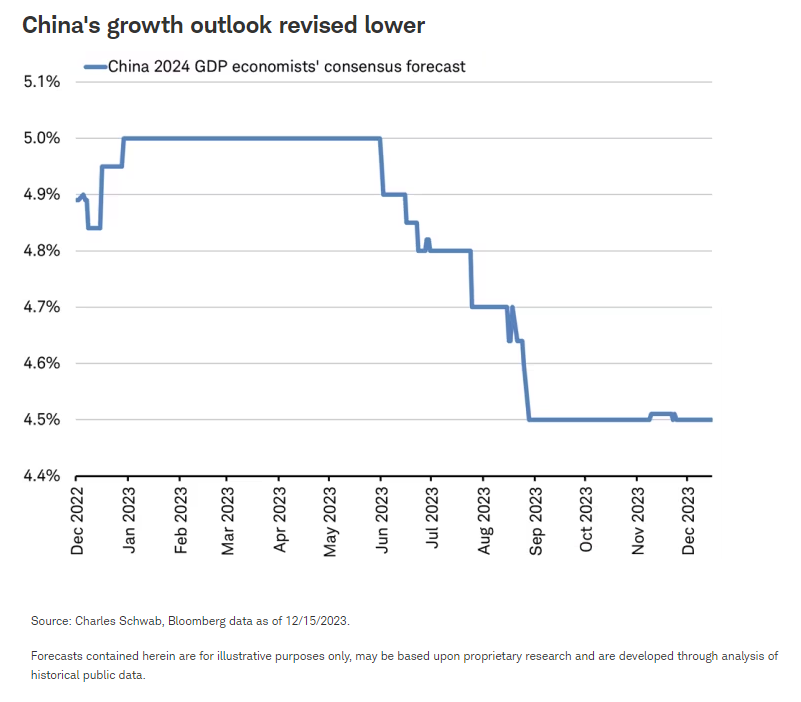

After strong growth in the first quarter of 2023, reopening momentum in China's economy stalled. Sentiment on China's growth outlook flipped from a year ago. Last year at this time, economists were upwardly revising their 2023 GDP forecasts from 4.8% in December 2022 to a high of 5.7% during the second quarter of 2023. But since mid-year 2023, economists have been steadily downgrading their 2024 outlook for China's economy from a mid-year high of 5.0% to a current forecast of 4.5%, as you can see in the chart below. China's official target is 5.0%. Economic pessimism is also reflected in the near-record lows seen in China's consumer confidence index from the National Statistics Bureau, which stretches back over more than 25 years.

After sticking to conservative and targeted policy adjustments for much of this year, even as economic growth was disappointing, China appears to have now changed course. In late October, China's leadership stepped up economic support measures by further easing housing policies and boosting infrastructure spending. More significantly, the government is likely to continue with more expansionary policy in 2024.

While China faces significant challenges (for our more in-depth take on China read: Is China Investable?), there is some potential for China to defy these low expectations in 2024. Property concerns by households may ease as government measures support delivery of contracted homes, export growth may improve as the global manufacturing recession slowly recovers, and ongoing stimulus measures may support industry. These drivers may combine to lift corporate profits and the price-to-earnings ratio of the MSCI China Index, which is currently in line with its 20-year low at nine times earnings.

Artificial intelligence (AI) productivity boost

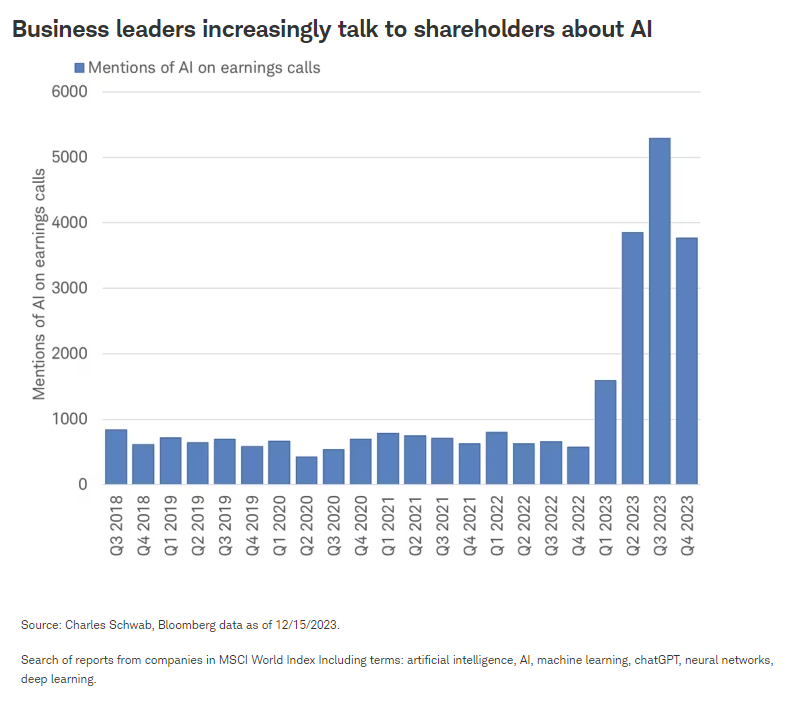

One development that has the potential to transform growth prospects might be an Artificial intelligence (AI)-related boom in productivity [for a deeper look at investing in AI read: Investing in Artificial Intelligence (AI)]. The tightest labor market in generations—with unemployment rates in the U.S., Canada, Germany, and the United Kingdom recently falling to lows not seen in 50 years—threatens to keep labor costs elevated and slow growth. AI could help manage wage costs by filling the gaps where workers are unavailable and boosting output per worker.

In general, history shows that the greater and more rapid the investment in new technologies by businesses, the greater the potential impact on productivity. We can gauge the potential impact of AI by monitoring the scale of investment into AI-related capital focused on information processing equipment and software. Historically, changes in productivity tended to be signaled a few years in advance by the change in business investment. Economy-wide productivity wasn't enhanced until enough businesses had integrated the new technology into their operations and capitalized on their new capabilities. Currently, AI integration seems to be in its infancy across wide swaths of industry, with a long way to go for adoption in manufacturing, product design, drug development, transportation, construction, customer service, heath care, agriculture, and mining. But it is possible that AI may be adopted more quickly in 2024 along with the potential of stronger growth and lower inflation.

Election surprises

There are several major presidential and parliamentary elections taking place in 2024. A risk to the manufacturing sector firming up in 2024 is tariffs and trade frictions further weakening demand and factory output. From the January election in Taiwan, to the June parliament election in Europe, to the U.S. elections in November, not to mention the elections in three of the five most populous countries in the world (India, Pakistan, and Indonesia) there is potential for outcomes that encourage nationalist policies that may hinder trade in manufactured goods.

A risk associated with U.S. elections in particular is during the transition between outgoing and incoming U.S. presidents, when foreign adversaries often have chosen to take actions in conflict with U.S. interests, to seemingly test the incoming administration.

- After the 1980 elections, the Iran hostage crisis came to a peak and ended (1/19/81) with the release of 52 American hostages minutes after the inauguration of Ronald Reagan on the following day.

- After the 1988 elections, George H.W. Bush contended with the terrorist bombing of a commercial airliner over Lockerbie, Scotland (12/21/88) and an aerial clash that led to U.S. fighters shooting down Libyan warplanes (1/4/89).

- After the 1992 elections, the transition period before the incoming Clinton administration included 28,000 U.S. troops being sent to Somalia in December 1992. In January 1993, Iraq moved surface to air missiles into the no-fly zone patrolled by the U.S. and allied warplanes, resulting in bombing of the missile sites.

While most geopolitical events tend to have a limited impact on markets relative to the economic and earnings outlook, the risks are worth monitoring.

Be prepared

While we highlighted our top five, there are many other risks for 2024 including those that are an ever-present part of investing and not unique to the outlook for any particular year. These include rising fiscal sustainability concerns as debt and deficits continue to spiral ever higher, another pandemic or variant could emerge that evades existing vaccines, the outbreak of wars, and cyberattacks that can disrupt the flow of information and commerce, among many others.

Whether or not these particular risks for 2024 come to pass, a new year almost always brings surprises of one form or another. Having a well-balanced, diversified portfolio with a risk profile consistent with your goals, and being prepared with a plan in the event of an unexpected outcome tends to be one key to successful investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Currencies are speculative, very volatile and are not suitable for all investors.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The MSCI Japan Index covers approximately 85% of the free float-adjusted market capitalization in Japan and is designed to measure the performance of the large and mid-cap segments of the Japanese market.

The MSCI China Index covers about 85% of this China equity universe and is designed to capture large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs).

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All