US equity market returns have been disproportionately driven by the so-called Magnificent Seven (Mag 7) stocks this year. Their dominance has created style imbalances within large-cap benchmarks that deserve closer attention from investors.

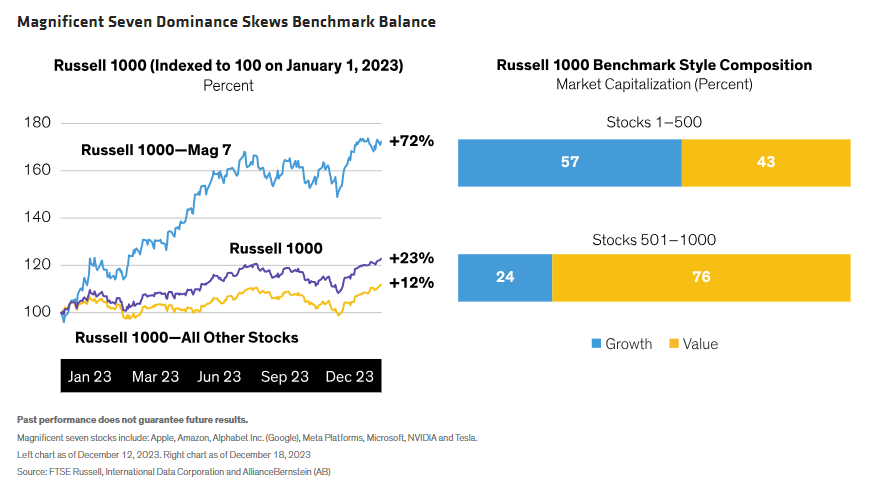

In a dramatic year for equity markets, the biggest actors on the US market stage hogged the limelight. The seven largest stocks in the Russell 1000 Index, which account for about 28% of the large-cap benchmark, surged by 72% through December 12—eclipsing returns for the rest of the market (Display). Similar trends were seen in global markets, such as the MSCI World, where the US Mag 7 stocks account for 19% of the benchmark.

The heavy market concentration in the Mag 7, which are seen as the big winners from the artificial intelligence revolution, profoundly affected investor outcomes. Portfolios that held all seven—Apple, Amazon, Alphabet Inc. (Google), Meta Platforms, Microsoft, NVIDIA and Tesla—enjoyed supercharged returns. Actively managed portfolios that didn’t own some of these stocks were saddled with big underweight positions, making it almost impossible to beat the benchmark—especially since the rest of the market underperformed.

Backstage at the Benchmark

Extreme market concentration has had other, less visible effects on the market. In particular, the style composition of key equity benchmarks has been skewed in surprising ways.

Index providers typically target a balanced style split between growth and value stocks in broad market benchmarks. Since the Mag 7 are mostly growth companies, their weight in the Russell 1000 creates a skew across the market-capitalization spectrum. The largest 500 companies in the Russell 1000 are somewhat tilted toward growth stocks. And as a result, the next 500 companies are heavily skewed toward value stocks—accounting for 73% of the weight in this segment of the market.