The election outcome is unlikely to change the status quo for the Taiwan Strait, U.S.-China relations, or global markets which have seemed to price in geopolitical risk.

Over the weekend, Taiwanese voters didn't just choose their next president and legislature, they also helped set the course for U.S.-China relations over the next four years. Voters chose between a ruling party determined to maintain Taiwan's independence and an opposition that sees closer ties with China as Taiwan's only viable path.

What's at stake

China's leadership considers Taiwan declaring independence as a "red line" that must not be crossed. China views eventual control of the self-governed island as vital to its national security, and frequently conducts military exercises into the Taiwan Strait. The U.S. officially acknowledges the People's Republic of China's claim to Taiwan but remains a staunch supporter of the status-quo (a self-governed, fully democratic society, with its own economy, currency, military, and elected officials). U.S. Defense Secretary Blinken defused tensions last year by explicitly saying that the U.S. does not support independence, paving the way for a meeting with Chinese President Xi and President Biden in November. Yet, President Biden has repeatedly said the U.S. would come to the defense of Taiwan if attacked, seemingly abandoning the U.S.'s long-maintained "strategic ambiguity" on Taiwan, and has stepped up military exercises with allies across the Indo-Pacific. It is possible that Taiwan's next president could upset the balance in tensions between these two superpowers.

Domestically, the election was seen differently. Surveys have shown it wasn't the relationship with China, rather domestic economic issues that were the main concern of Taiwanese voters, including wage growth, inflation, housing affordability and energy security. In 2023, wages trailed the pace of inflation and the cost of housing ranks among the world's most expensive relative to income. While the presidential candidates have made similar pledges addressing most these issues, there are some key differences. One being the future of Taiwan's nuclear power plants. According to comments made during the 2nd presidential candidates' debate, the Democratic Progressive Party (DPP) pledged to close them down and the Kuomintang (KMT) proposed to delay those closures in favor of a slower energy transition.

The outcome

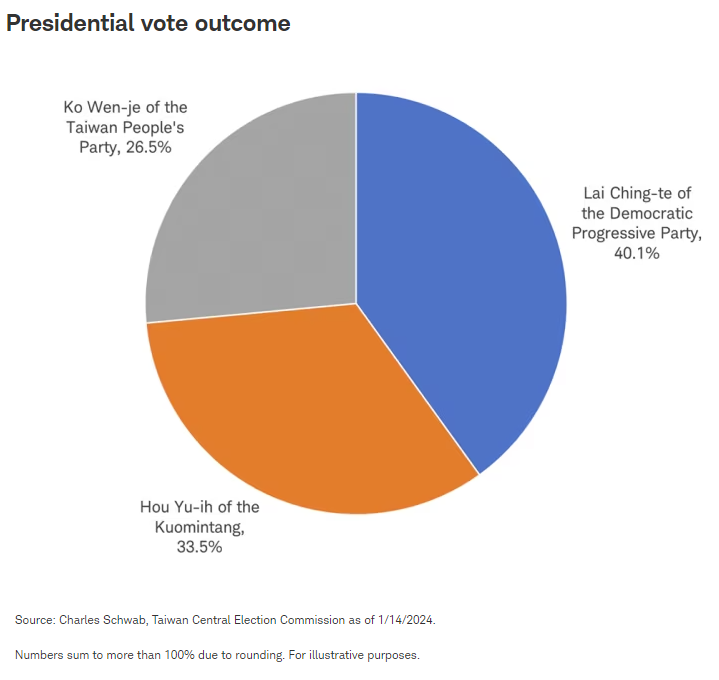

The winner of the Presidential election, the ruling pro-independence DPP, did not see a decisive victory, winning 40% of the vote. The conservative KMT—which has eventual reunification with China in its charter—came in second with a 33.5% share of the vote. The relatively new Taiwan People's Party (TPP), which has a more pragmatic view of Taiwan-China relations, came in third at 26.5%.

The victory by the DPP is likely to be market-neutral, with continued risk to U.S.-China tensions for the next four years. But there are offsets to how China may view the outcome:

- First, President-elect Lai Ching-te, stressed in his campaign that he has no plans to upset the status quo with China. Writing in the Wall Street Journal on July 4, he said he would "support the cross-strait status quo."

- Second, the outcome was closer than in 2016 and 2020 when the DPP's candidate led the KMT candidate by double-digits and went on to win comfortably with more than 50% of the vote. This rise in support for the party that most favors closer ties with China may ease Beijing's concerns that Taiwan is drifting further from its grasp.

- Third, the DPP losing its majority in the legislature demonstrates political support for parties in favor of greater dialogue with China.

The ongoing U.S.-China reengagement that took place over the summer of 2023, culminating with a Xi-Biden meeting in November took a lot of work on both sides. China would have to consider the cost of losing its hard-earned goodwill and stabilization in U.S. relations should they decide to engage in an aggressive response to the election. China's response is more than likely to be symbolic, perhaps involving some economic sanctions or military drills—a comparison may be the military drills that followed then U.S. House Speaker Pelosi's visit in 2022.

Market impact

It's possible the election outcome may hold little overall market significance given these offsetting factors. Despite the shifting tensions in 2023, Taiwan's stock market outperformed peers, as you can see in the chart below.

Yet the outcome could hold impacts for certain sectors if China suspends tariff concessions on Taiwanese agricultural, fishery, and machinery products, as well as auto parts and textiles. The election outcome may have implications for the global computer chip supply chain and foreign capital flows to Taiwan's tech sector. One reason Taiwan's stock market fared well in 2023 was an artificial intelligence boom and a turnaround in the semiconductor cycle. Currently, Taiwan Semiconductor Manufacturing Co. produces around 90% of the world's most-advanced chips, according to research conducted by the Boston Consulting Group and the Semiconductor Industry Association. The DPP administration will likely continue to maintain Taiwan's status as an independent location to fabricate chips and assemble AI servers. A KMT victory might have led to firms attempting to diversify their supply chain away from the island. How the new administration manages U.S. and European relations will be crucial in ensuring access to chip-making equipment from Western providers such as the Netherland's ASML.

Taiwan's future

Beijing has long described reunification with Taiwan as a goal. However, China knows that using military force would likely result in the developed world inflicting negative economic consequences in response. China is much more integrated with the global economy, compared with Russia prior to attacking Ukraine. The threat of sanctions from the rest of the world could cause significant damage to China's economy.

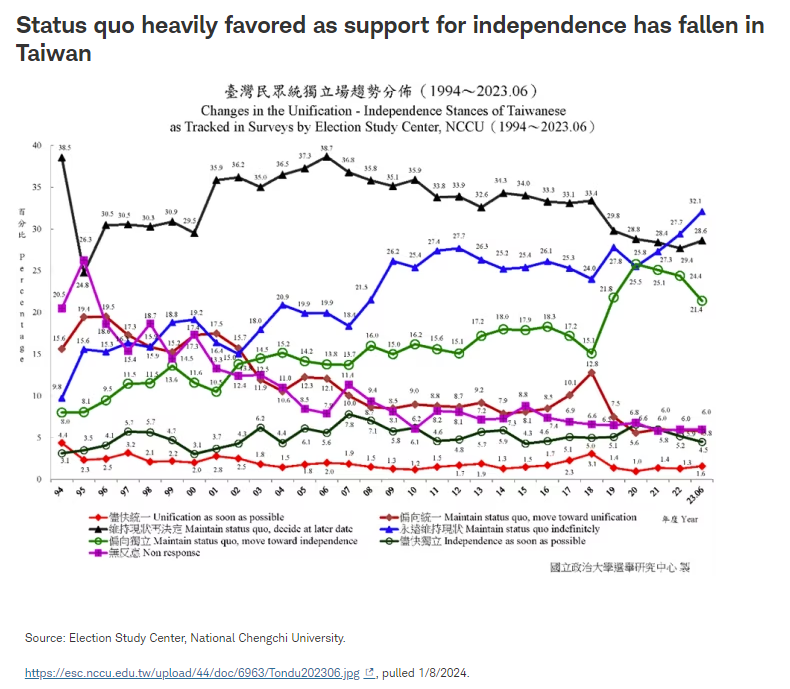

Furthermore, the election outcome may not hold much significance for Taiwan's immediate future. We maintain our view that an invasion of Taiwan by China is a low probability over the intermediate term. The chart below from Taiwan's National Chengchi University tracks sentiment among the Taiwanese on independence versus reunification with China over several decades. The latest reading from the middle of last year (the next 6-month update should be published soon) has continued to show an overwhelming majority of Taiwanese in favor of the status quo, rather than a shift to either independence or reunification. In fact, sentiment favoring independence has declined in recent years, even as tensions over such a shift have increased. The takeaway is that the people of Taiwan don't seem to favor a change in the Taiwan-China relationship no matter who won the election.

Key takeaways

- The Taiwanese election is unlikely to change the status quo of tense U.S.-China relations, as both the U.S. and China aim to support their own economic growth independently, perhaps through protectionist measures.

- China-Taiwan tensions may rise but are unlikely to result in a military conflict. The overwhelming majority in Taiwan are favor of the status quo and Beijing is averse to economic sanctions resulting from taking military action.

- The outcome is likely neutral for Taiwan and China stocks, due to an already elevated geopolitical risk premium in anticipation of a response by China in the form of sanctions and military drills.

- China excels at the long game and may take some comfort in the gains by the KMT in the Presidential and legislative elections.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The MSCI EMU Index (European Economic and Monetary Union) captures large and mid cap representation across the 10 Developed Markets countries in the EMU, covering approximately 85% of the free float-adjusted market capitalization of the EMU.

The TAIEX Index is capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The MSCI AC Asia Pacific Index captures large and mid-cap representation across 5 Developed Markets countries and 8 Emerging Markets countries in the Asia Pacific region covering approximately 85% of the free float-adjusted market capitalization in Australia, China, Hong Kong, India, Indonesia, Japan, Korea, Malaysia, New Zealand, Philippines, Singapore, Taiwan & Thailand.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab