Credit quality in the muni market likely has peaked, but we believe states' strong rainy-day funds and other attributes will lend stability in the near term.

Two states that account for one-third of the municipal bond market, New York and California, are projecting multi-billion-dollar budget gaps for the upcoming fiscal year. Is it cause for concern?

We don't see this as a major cause for concern, but the muni market is likely past the peak in credit quality for this cycle, which could affect issuers' ability to repay debts. However, most states have built up their reserve levels to record-level highs and have many credit strengths, which lends itself to credit stability in the near term, according to ratings agency Standard and Poor's.

Even though credit quality is showing signs of weakness, some bonds in states with a high income tax rate are yielding less than AAA-rated bonds,1 the highest level of credit quality. This generally shouldn't happen, because bonds with greater credit risk should yield more than bonds with less credit risk. The implication is that most investors, even those in high-tax states, may be able to achieve higher after-tax yields by adding munis from other states instead of sticking with only bonds from their home state.

A primer on state debt

Most states issue bonds to fund specific projects, help with cash-flow planning, or for various other purposes. Like most municipal bonds, state general obligation bonds pay interest that is usually exempt from federal income taxes. If purchased by a taxpayer in the issuer's state, they're often exempt from state income taxes, too. As a result of the tax benefits, they may be an attractive option for high-income earners looking for a relatively stable income source.

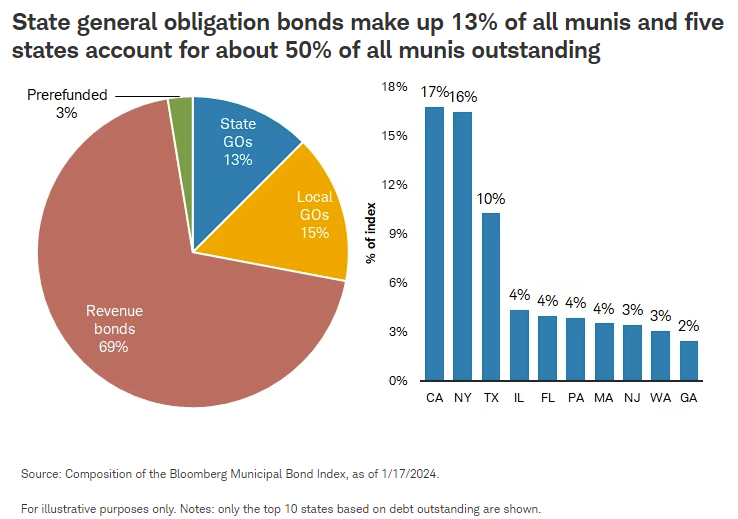

Bonds issued by states account for about 13% of the muni market. Nearly half of the bonds in the market, including munis issued by states, are from issuers in five states: California, New York, Texas, Illinois, and Florida. Given the high concentration of the market, it can be difficult for investors outside of those states to find enough issuers with differing credit risks to achieve adequate diversification.

States issue different types of debt, but the most common is a general obligation bond that is paid from the general fund and backed by the taxing authority of the state. States generally have high credit quality due to the broad authority they are granted to raise or lower tax rates and implement new taxes or fees.

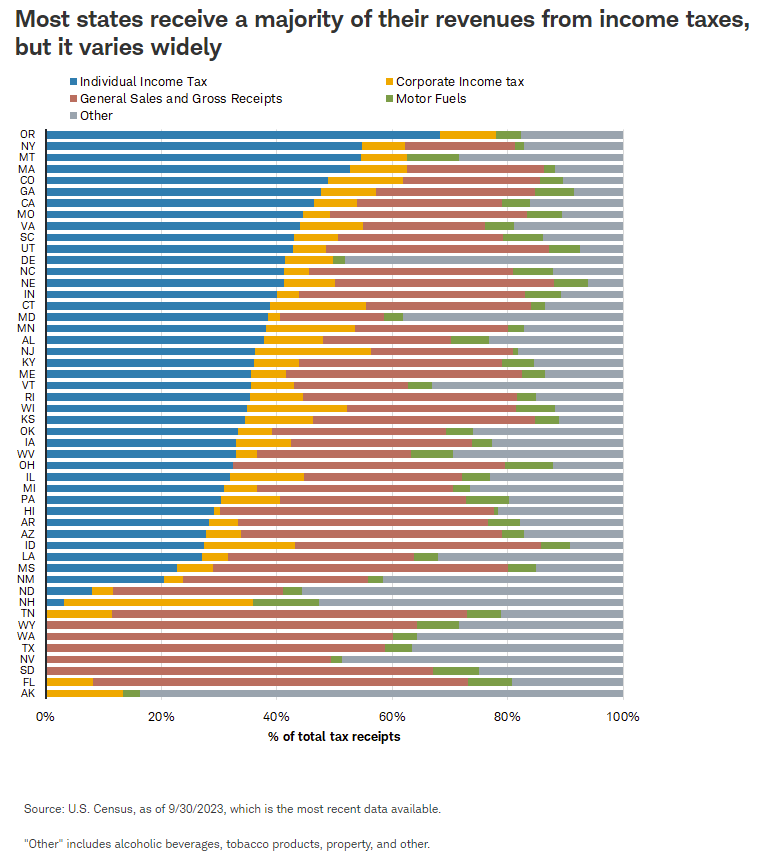

Most states derive the majority of their revenues from corporate and individual income taxes, but this can vary widely, as illustrated in the chart below. For example, the state of New York derives about two-thirds of its tax revenues from corporate and personal income taxes combined. This compares to Texas, for example, which doesn't rely at all on those two revenue sources but instead has a much greater reliance on general sales and gross receipts.

The outlook for most states is stable, but likely to get worse

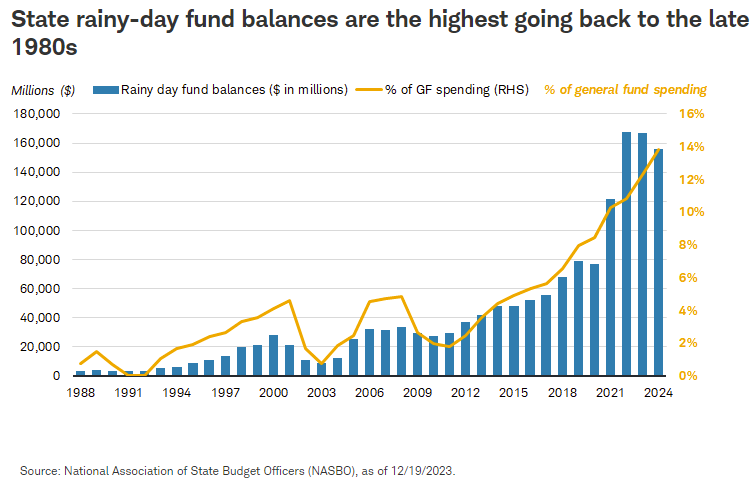

Since 2020, state tax revenues increased rapidly but are now showing signs of slowing. Many states used the better-than-expected growth in tax revenues, combined with the ample fiscal aid, to build up their reserve levels to record level highs. The aggregate state rainy-day fund is nearly 14% of general fund spending, which is the highest level going back to the late 1980s, according to the National Association of State Budget Officers. A rainy-day fund is akin to a savings account that states can tap into, with restrictions, if they need to offset a decline in revenues.

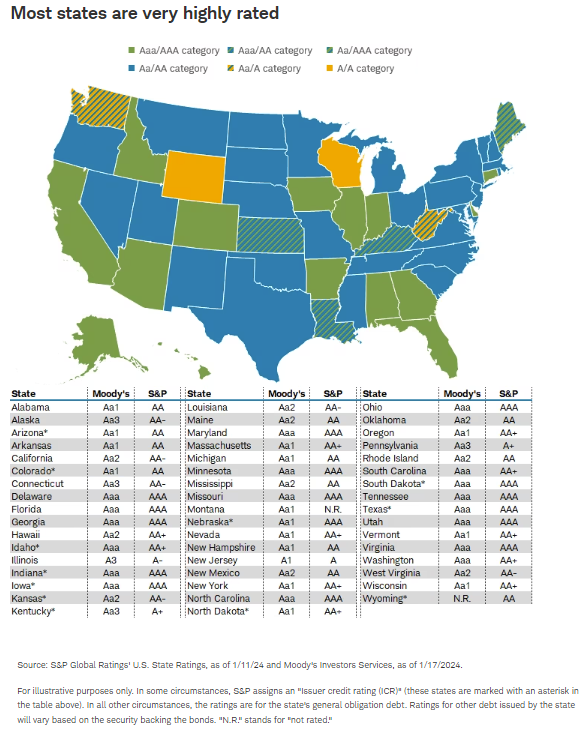

According to Standard and Poor's, the high levels of reserves and other resources "should provide a liquidity credit cushion for the coming year and beyond." Partly because of strength in tax revenues, the credit ratings for most states are the highest they've been in quite some time. In fact, all states are rated at least A by Standard and Poor's, which is the first time that's happened since 2016.

Going forward, the outlook for most states isn't as rosy as it has been in the past few years. Partly due to the better-than-expected tax revenues and ability to build up reserves to record levels, 25 states have reduced personal income tax rates since 2021. Some states have lowered their tax rates multiple times since 2021. This is a risk because if the economy slows, as is expected by Bloomberg consensus estimates, it could create revenue pressures that states will have to manage through. For states with a high reliance on sales tax revenues, a slowdown in consumer spending could result in less sales tax revenues as well. Rating agency Moody's expects that state tax revenue growth will "be in the low single digits because of continuing weakness in capital gains, lower oil and gas severance taxes, and slow sales taxes."

Additionally, federal fiscal policy is another area of uncertainty for states. The risk of a federal government shutdown has recently risen and if it were to occur, it could have negative revenue implications for states, in our view. Later in the year, the election could be another area of uncertainty for states. According to S&P, 11 states will hold gubernatorial elections this fall, while 85% of all House of Representatives seats and 65% of Senate seats will be up for election. The election has the potential to shape fiscal decisions going forward. S&P expects that states will receive less federal fiscal aid in the future compared to what they received following the onset of COVID regardless of the election outcomes.

Most muni investors should consider bonds from outside their home state

We generally suggest that only investors in New York and California consider a portfolio of all in-state municipal bonds. The combination of a high state tax rate and large number of issuers justify sticking with only in-state munis. However, given where yields are today for California and New York state general obligation bonds, an investor who is not in the top tax bracket may be able to achieve higher after-tax yields with bonds from an issuer outside of New York or California.

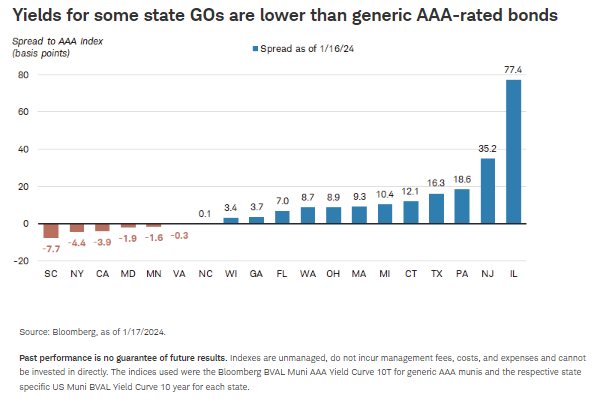

The chart below compares the spreads on indices that are available from Bloomberg of 10-year state general obligation bonds to that of an index of generic 10-year AAA munis. Some states don't have enough general obligation bonds outstanding to construct an index, so that's why not all 50 states are shown. A spread is the difference in yields between the two indices, and is often viewed as the additional compensation for taking credit risk. Even though the credit rating for states like California and New York are below AAA, their bonds are paying less than a generic AAA index. That shouldn't occur, because investors should be compensated for taking some credit risk. This is likely the case because tax rates in those states are very high and the 2017 Tax Cuts and Jobs Act eliminated many tax itemizations that were beneficial to high-income earners in these states. As a result, demand for bonds from these states increased, driving their yields lower than AAA-rated bonds.

It's important to note that these spreads are just for an index of 10-year general obligation bonds of the state. Other bonds within the state, either of lower credit quality or from different issuers, may have different spreads and therefore could justify a greater weight toward in-state munis.

What to do now

The outlook for states has implications for other municipal bonds because many other issuers receive some form of state aid or financial support. If states have less funding, then the ability to support the issuers could decline. Overall, the outlook remains stable but it is starting to show cracks. We don't believe this will result in widespread defaults or downgrades, but we would suggest focusing on issuers in the AA/Aa and AAA/Aaa categories. For investors who can tolerate some credit risk, we suggest adding some lower-rated investment-grade issuers with revenue streams that aren't overly dependent on current economic activity, as the outlook for the economy is for it to slow.

1 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

All names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Charles Schwab & Co., Inc. does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab