Market expectations have established a high bar for central banks' rate cuts. Any disappointment like stronger inflation or economic growth could spark market volatility.

The central banks in the eurozone, China, Japan, and Canada met last week. The U.S. Federal Reserve and the Bank of England are meeting this week. No policy changes so far—but are we getting close?

It's a Mad (-Lib) world

Time spent analyzing central bankers' messages is all about the seemingly subtle details. It reminds me of Mad Libs,® the word game where one player asks others for a list of adjectives, verbs, and nouns to substitute for blanks in a story before reading it aloud. The often-hilarious outcomes result from the power of word choice; the change of a word can change the meaning of the entire story and possibly spark a wild reaction.

Central bankers recognize that word choice has the power to move the markets—sometimes wildly, which is why they are intentional and exacting in their communications. For example, they may settle on using a slightly firmer adjective than in their last missive to describe a change in the economic environment or their confidence in achieving a particular objective. The desired result is to nudge market expectations toward an intended direction without triggering a big surprise market reaction when a policy change is eventually made.

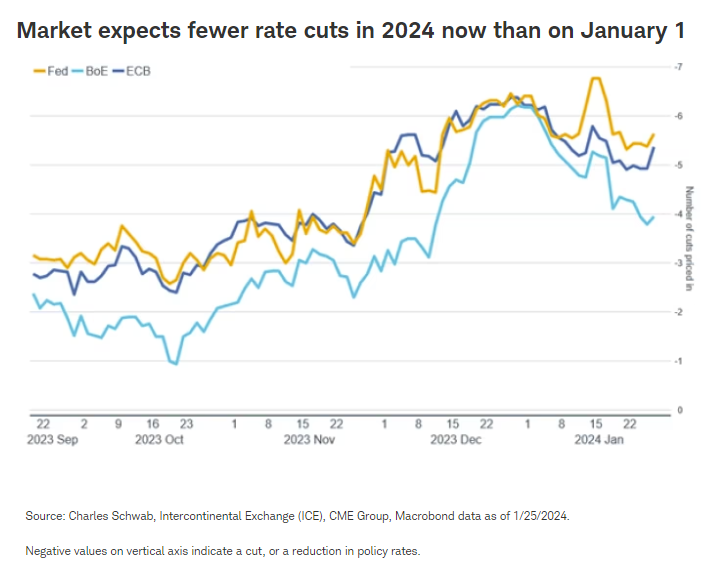

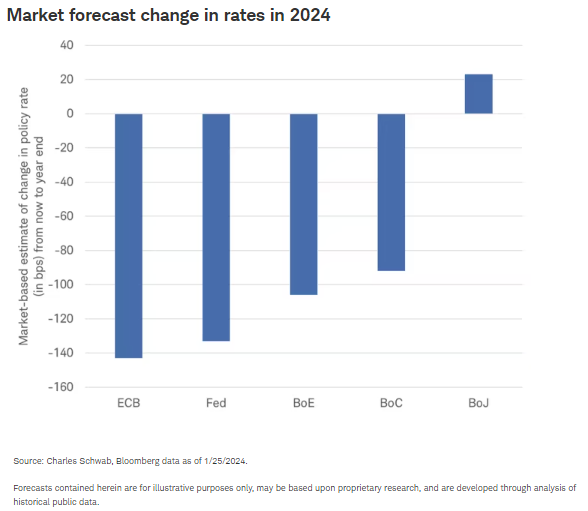

Taking it back

The first half of January seemed like the return of a Christmas gift after the holidays; stock markets took back the gains from Santa Claus rally on signs of a later start to rate cuts from policymakers given strong economic data. The chart below shows how the market has been reevaluating the number of rate cuts by some major central banks in 2024. It may be no coincidence that as we heard from these policymakers last week, stock markets stabilized.

European Central Bank

In January, the European Central Bank (ECB) sent a clear message to the markets that cuts are coming soon—but not in the first quarter. The first paragraph of the ECB's statement asserts that incoming information "has broadly confirmed its previous assessment." This suggests that developments around inflation and economic growth have been playing out as expected, rather than surprising on the downside in a way that would force a rate cut at the next meeting in early March.

Yet, a rate cut can be expected this summer, according to ECB President Lagarde. She was interviewed by Bloomberg in Davos at the World Economic Forum just a day before the start of the quiet period which precedes ECB monetary-policy meetings. When asked if there could be majority support for such a move she replied, "I would say it's likely, too. But I have to be reserved, because we are also saying that we are data dependent, and that there is still a level of uncertainty and some indicators that are not anchored at the level where we would like to see them." Betting on inflation receding faster than the ECB forecasts resulting in an earlier pivot, markets continued to price in the first 25-basis-point (bp) cut at the April meeting, followed by another at every meeting for the rest of 2024. An ongoing risk to this view is upside inflation pressures. There has been a 500% increase in shipping costs from Asia to Europe (based on the Drewry World Container Index cost of moving a container from Shanghai to Rotterdam), driven by the conflict in the Middle East.

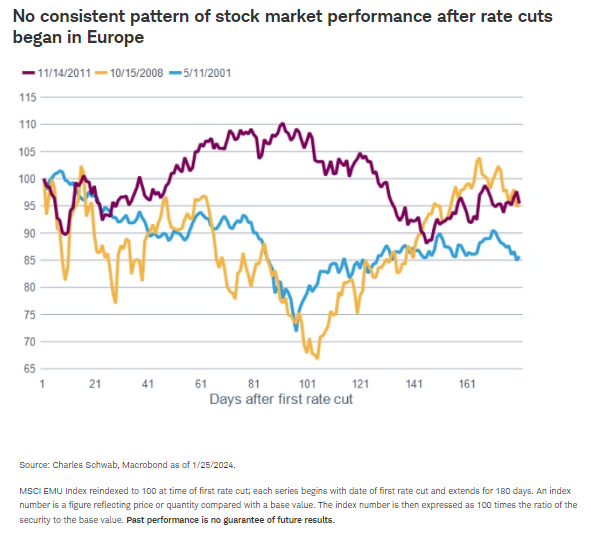

What does this mean for European stocks? Historically, the stock market reaction during the 180 days after the first rate cut has been mixed for Europe. The chart below shows the market's path following the start of the last three rate cutting periods in Europe that began in 2001, 2008, and 2011. The economic and earnings environment was different in each of these periods, and this time is no exception. In theory, lower rates should boost demand and market liquidity—but much will depend on the pace and timing of an economic and earnings recovery from Europe's 2023 recession.

People's Bank of China

The People's Bank of China (PBoC) held off on cutting policy interest rates last week, signaling another rate cut following the last one in August may be coming soon. However, China's central bank did step up support for the economy by a larger-than-expected 50 bp cut to the reserve requirement ratio for banks in an effort to encourage lending. The announcement of additional funding support for property developers coupled with rumors of intervention in the stock market to prop up prices and discourage selling boosted equity prices.

While PBoC rate cuts may take place in the coming months, high interest rates have not been what ails China's economy–it's consumer, business, and investor confidence. Attempts to intervene in the stock market last year only saw a temporary reprieve before stocks continued their downward trend. While further measures to revive the economy have been hinted at, the slow drip of policies, which are often reactive, uncoordinated, and targeted rather than prompt and broad, have thus far not been sufficient to spark a turnaround. Consumer confidence remains low due to the hangover from the zero-COVID-19 policies and weakness in consumers' biggest asset: property. Business confidence is also likely low, due to weak demand and regulatory flip-flops.

What could turn economic momentum? A government guarantee of homebuyer deposits at troubled property developers could help boost consumer confidence from its recession-like lows. Measures to reduce government regulations into the operations of business and encourage entrepreneurship could support business confidence. The current focus on supply side stimulus amid excess capacity seems to be fueling a deflationary environment, with China's consumer price index (CPI) below zero for the past three months.

Bank of Japan

The Bank of Japan (BoJ) meeting last week included a signal that the central bank is on track to raise rates from negative levels for the first time in 17 years. A hike from -10 basis points to zero may come as early as April. The "Outlook for Economic Activity in Prices" report reflected an increase in the confidence for Japan achieving the central bank's 2% inflation target in the medium term. The BoJ noted specifically that they are closely monitoring the spring wage negotiations, or shunto, which brings together unions and management to set monthly wages ahead of the start of Japan's fiscal year in April. This suggests the policymakers are so far encouraged that the wage negotiations taking place might deliver the right amount of growth in wages to sustain 2% inflation. Those negotiations are expected to conclude prior to the April Bank of Japan meeting.

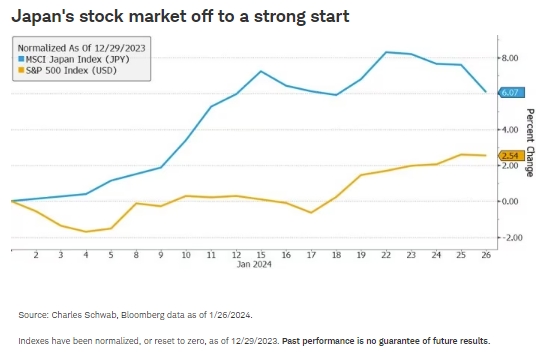

Any rate hikes in Japan could offset some of the excitement over rate cuts by other major central banks in 2024. Any rate hikes over the next year hold the potential to prompt Japanese investors to sell foreign assets and bring them home, a move incentivized by a potentially stronger currency, higher interest rates, and the 28% gain in Japan's NIKKEI 225 Index for 2023. In fact, Japan's Ministry of Finance data showed that Japanese investors turned net sellers of foreign stocks for back-to-back months in November and December after the central bank signaled the coming shift in policy at the October meeting. The size and speed of the reversal of over a decade's worth of investment flows could weigh on non-Japanese investments. The MSCI Japan Index is off to a strong start for this year, compared to the S&P 500.

Bank of Canada

The Bank of Canada (BoC) held their policy rate steady last week but signaled a pivot from being prepared to hike rates further to the timing of a rate cut. Additionally, they seem increasingly comfortable with Canada's inflation outlook, nudging down the inflation forecast for the end of 2024 to 2.4% from 2.5%. In a change relative to December, the bank's statement did not signal preparedness to raise the policy rate further if needed. During the press conference, Governor Macklem indicated that "future discussions will be about how long to maintain the current restrictive stance."

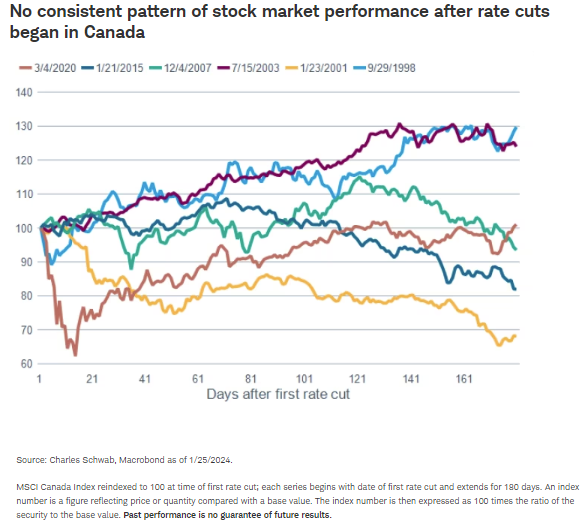

As with other central banks, the stock market reaction in Canada over the first 180 days following the start of rate cuts is mixed: in three periods stocks were up (1998, 2003, 2020) and in three (2001, 2007, 2015) they were down. Often rate cuts come during periods when economic and earnings growth is weak. Canada's stock market is uniquely tied to natural resources, so a stronger outlook for global manufacturing may be more relevant to Canada's stock market than rate cuts intended to encourage domestic demand alone.

A high bar

The expectations for over 100 bps of rate cuts by the Fed, ECB, and BoE beginning as soon as March establish a high hurdle for central bankers to deliver on the market's expectations, setting up the potential for disappointment and a volatile first half of 2024, similar to what the markets experienced in January.

Ultimately, we believe describing 2023 as a year of rate hikes and 2024 as a year of rate cuts isn't particularly helpful to investors given the varied market reactions influenced by the differing economic and earnings environments that accompanied rate cuts in the past. Nevertheless, ahead of any actual rate cuts the market is likely to welcome signals by central bankers of a nearer and more aggressive path toward them.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author’s views as of that date. It will be kept solely for historical purposes, and the author’s opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Currency trading is speculative, volatile and not suitable for all investors.

Commodity-related products, including futures, carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions, regardless of the length of time shares are held. Investments in commodity-related products may subject the fund to significantly greater volatility than investments in traditional securities and involve substantial risks, including risk of loss of a significant portion of their principal value. Commodity-related products are also subject to unique tax implications such as additional tax forms and potentially higher tax rates on certain ETFs.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

Drewry World Container Index is a global freight rate index that tracks freight costs for eight major routes expressed as an average price per 40-foot container (in US$).

The MSCI EMU Index (European Economic and Monetary Union) captures large and mid-cap representation across the 10 Developed Markets countries in the EMU, covering approximately 85% of the free float-adjusted market capitalization of the EMU.

The MSCI Japan Index captures the performance of the large and mid-cap segments of the Japanese market, covering approximately 85% of the free float-adjusted market capitalization in Japan.

The MSCI Canada Index captures the performance of the large and mid-cap segments of the Canada market, covering approximately 85% of the free float-adjusted market capitalization in Canada.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab