Market folklore provides an easy, but inaccurate guide for investing in today's interconnected and complex market. Indicators based on economic or market behavior may be preferred.

As investors ponder what this year may hold for the markets, the inter-relationships between politics, economics, fiscal policy, monetary policy, and corporate actions can seem very complex. This year could feature seemingly chaotic movements in economic data as we wrote about in our 2024 Outlook. Investors may feel overwhelmed and seek a simple answer, a rule of thumb, to help make decisions when things seem too complicated to analyze.

We don't place any value on market folklore like the "January Effect" or the "Super Bowl indicator," but we are often asked about them during this time of the year. Jittery investors are looking for clarity in an environment where little is certain. We're revisiting these indicators this year to remind investors that they only appear to have stood the test of time.

Super Bowl

Market prediction for 2024: Loss

Historical accuracy claim: 85%

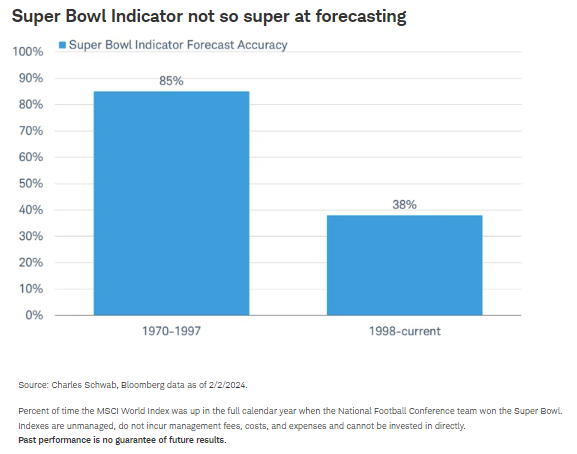

The Super Bowl indicator claims that the stock market goes up for the year when the winner of the Super Bowl comes from the National Football Conference (NFC), but when an American Football Conference (AFC) or expansion team wins, the market falls. Up until the underdog Denver Broncos (AFC) defeated the Green Bay Packers (NFC) in the 1998 Super Bowl, the indicator had been correct in 23 of 27 years, or 85% of the time, as measured using the MSCI World Index.

However, since 1998, the Super Bowl indicator has had a poor record; it has been correct less than half of the time. The most notable failure was the New York Giants' (NFC) upset win in 2008 over the New England Patriots (AFC), which if theory held, predicted a bull run for stocks. Instead, stocks plunged that year as the financial crisis took hold. This year's win by the Kansas City Chiefs on February 11 was widely watched, but not for its forecasting ability.

January Effect

Market prediction for 2024: Gain

Historical accuracy claim: 79%

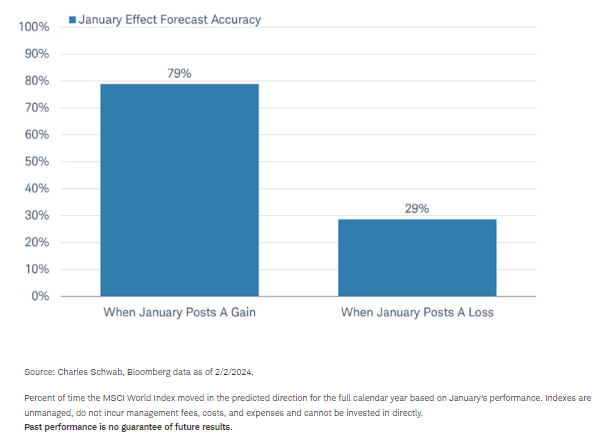

As January goes, so goes the year according to this market adage. It is true that January has more consistently indicated the direction of the stock market for the year than any other month. When the MSCI World Index has posted a positive return in January, the year as a whole ended with a gain 79% of the time since 1969, when the index began.

Again, this sounds impressive, but when January was negative, the year suffered a loss less than one-third of the time. It seems January doesn’t really have much of an “effect.”

First five days

Market prediction for 2024: Loss

Historical accuracy claim: 79%

This popular piece of market folklore says that the direction of the stock market during the first five days of the year determines whether the world's stock markets will be up or down for the year. The support for this indicator comes from the fact that over the past 44 years, full-year gain followed in 19 of the 24 times the first five days of January posted a net gain for the MSCI World Index—at first glance a 79% accuracy level. But is it significant? Not very. Here are two things to keep in mind:

- The MSCI World Index has posted a gain for the year more than 70% of the time, no matter what the first five days have done.

- A decline in the first five days has been accurate only about 25% of the time at predicting a down year.

Groundhog Day

Market prediction for 2024: Loss

Historical accuracy claim: 72%

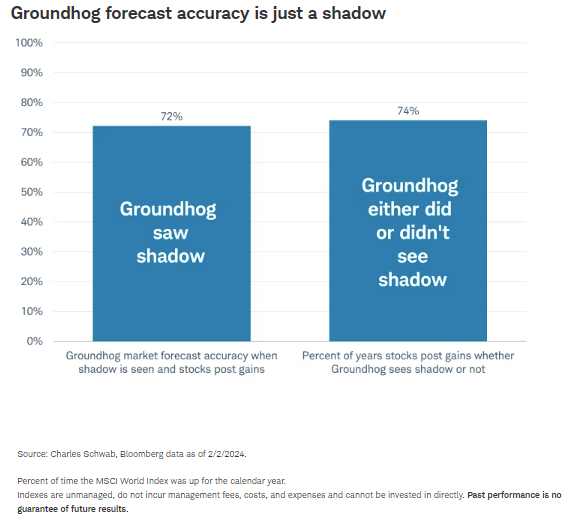

If the world's most famous forecasting groundhog, Punxsutawney Phil, sees his shadow we are expected to get six more weeks of winter. If he does not, it's predicted that the cold gives way to an early spring. A lesser-known prediction that accompanies seeing his shadow is for a gain in the stock market. When Phil has seen his shadow, temperatures have been colder than usual in the U.S. 47% of the time since 1969—a statistical coin flip. However, is he much better at predicting stock market performance? Stocks around the world (MSCI World Index) have been up 72% of the years Phil has seen his shadow. This year, on February 2, he did not.

Of course, the fact that the stock market has posted a positive total annual return 74% of the time since 1970, whether Phil saw his shadow or not makes Phil's stock market prediction about as useful as his weather prediction.

Lunar New Year

Market prediction for 2024: Gain

Historical accuracy claim: 75%

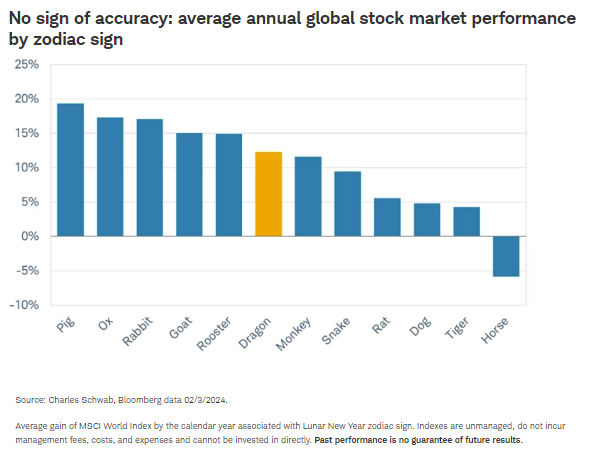

2024 is the year of the dragon in China, South Korea, Taiwan, and Vietnam. A look back at average annual world stock market returns by Chinese zodiac sign shows us that the year of the dragon has been close to the average in terms of performance.

However, there have only been four prior years of the dragon since the inception of the MSCI World Index and the return for the MSCI World Index has been mixed: 1976 +10%, 1988 +21%, 2000 -14%, and 2012 +13% demonstrating the lack of a substantial basis for any accuracy claim for this indicator of market performance.

No easy answers

As those five indicators illustrate, no indicator can provide a guarantee of future performance. Fortunately, we do have some economic and market indicators to help guide us on what may lie ahead for the markets in a complicated year, including these five:

- Purchasing Managers' Index – S&P Global produces this monthly leading indicator that may signal a shift in economic and market leadership in 2024 as a potential recovery follows 2023's manufacturing recession while the strong service sector of 2023 weakens. The preliminary reading for each month by economy comes out around the 20-25th of the month, while the final reading for the global manufacturing index in aggregate is produced on the first day of every month covering most major countries.

- Global Supply Chain Pressure Index – The New York Federal Reserve's monthly comprehensive measure of potential supply chain disruptions derived from shipping costs and delivery times can help gauge any potential inflationary impact stemming from weather- and conflict-related trade disruptions. The index is updated on the fourth business day of each month.

- Consumer price index – The U.S. Bureau of Labor Statistics and similar agencies in other countries produce this monthly measure of inflation. Policymakers around the world are watching inflation closely to ensure it continues to trend sustainably towards the 2% target adopted by the world's major central banks.

- Equal-Weighted Index – Most stock market indexes are capitalization-weighted, where the biggest stocks have the biggest weighting in the index and the biggest impact on index performance. But most also have an equal-weighted index counterpart, where each stock gets an equal weighting, providing a measure of what the average stock is doing rather than merely a handful of the largest ones. In general, the greater the number of stocks that are helping push the overall market higher, referred to as market breadth, the more support the market has.

- Yield curve – The government bond market tends to signal a global recession when short-term yields rise above longer-term yields, referred to as an inversion of the yield curve. The bond markets of all but one of the Group of Seven countries (Canada, France, Germany, Italy, Japan, United Kingdom, United States) had inverted yield curves in 2023 (the exception being Japan) and only one of them, the United States, avoided having at least one quarter of zero or negative GDP growth last year. A return to a more normal, or upwardly sloping, yield curve in 2024 may signal a brighter outlook for economic and earnings growth.

The enduring popularity of market folklore for investment decision making—despite their history of an at best coin-flip accuracy when examined closely—is a testament to the very human desire for an easy answer on how to invest in today's interconnected and complex markets. The truth is, no indicator provides a guarantee of future performance, which is why diversification, and a long-term perspective are so important to achieving investment goals in the stock market.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

More Fixed Income Topics >