Confidence Catches Up

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSentiment data is beginning to match relatively strong "hard" economic data.

U.S. consumer confidence has finally begun to catch up with relatively strong "hard" signals such as jobs and inflation data. This is potentially positive news for the stock market, where we expect a continued broadening-out in market breadth. However, the fixed income market is likely to experience continued volatility for similar reasons: The resilience of the economy is complicating the Federal Reserve's timing on potential interest rate cuts, which is sending mixed signals to the markets.

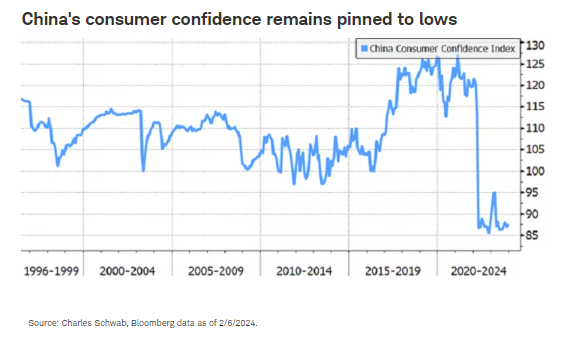

Meanwhile, the unpredictability of Chinese government policy is adding to uncertainty in its stock market. Measures to revive the Chinese economy have been a slow drip of policies so far, and have not been sufficient to support a sustainable turnaround in Chinese consumer confidence, which remains low due to weakness in the property market.

U.S. stocks and economy: Revived confidence

A key theme over the past year has been the strong disconnect between soft and hard data. Soft data—which are survey-based—measure attitudes and are qualitative in nature. Conversely, hard data are quantitative and represent concrete data points. Understanding the difference between both has been key to comprehending why the current economic cycle has looked so different relative to others.

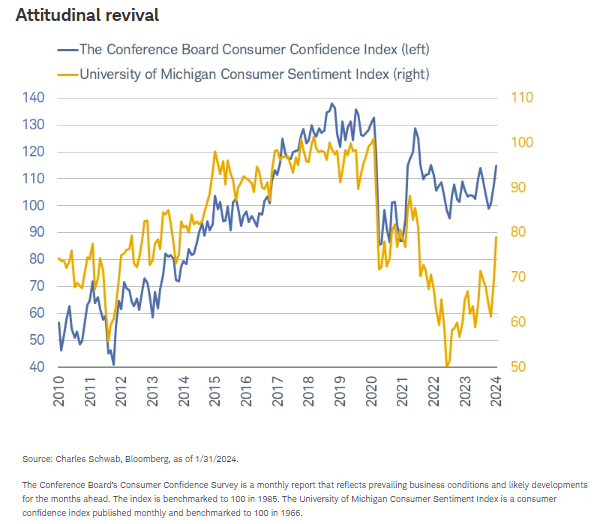

On the sentiment side, consumers didn't feel cheery for most of the past year, but that has started to change lately. As shown in the chart below, the Consumer Confidence Index (CCI) from The Conference Board and the Consumer Sentiment Index (CSI) from the University of Michigan have turned sharply higher over the past couple of months. It's worth noting that the CSI experienced a much larger drop from its pre-pandemic heights, given that the index is driven relatively more by inflation dynamics. Conversely, the CCI is more tied to the health of the labor market.

The CCI's stronger tie to labor explains why it has held up much better over the past couple of years. Even as inflation started to rise in early 2021, the unemployment rate continued to move lower. In fact, as of January, the unemployment rate has been below 4% for 24 consecutive months—the longest streak since the 1960s.

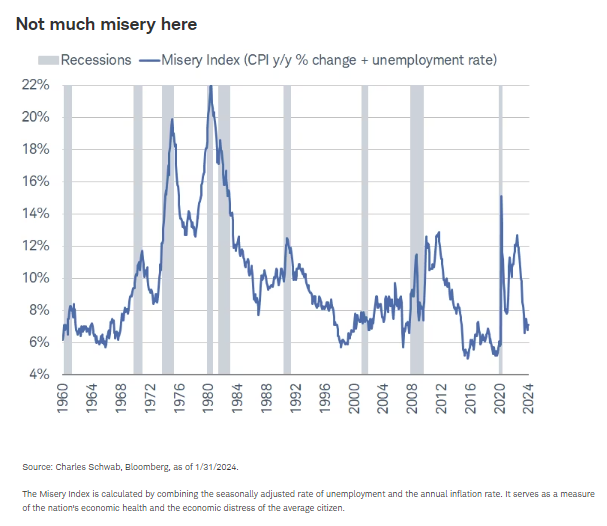

The improvement in confidence and sentiment has looked more like a catch-up to relatively resilient hard data. For example, the Misery Index—which combines the year-over-year percent change in the Consumer Price Index (CPI) and the U.S. unemployment rate—has stayed quite low relative to history, countering the notion that we are facing another inflation-driven economic shock akin to the 1970s.

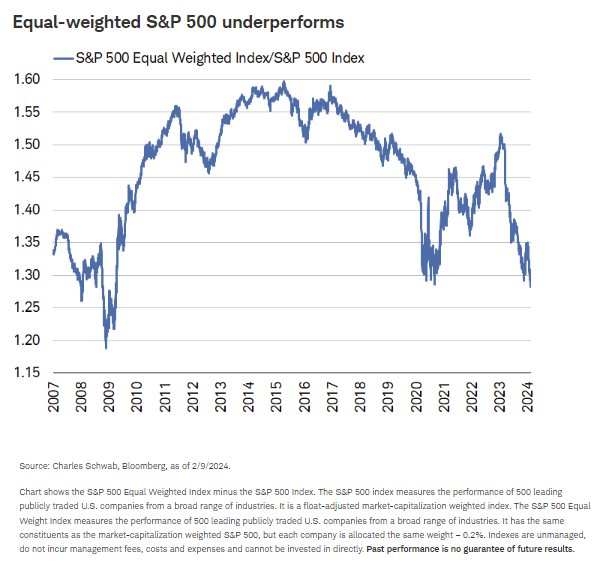

One of our expectations for the stock market this year is a continued improvement in market breadth—that is, the number of stocks whose prices are rising versus the number whose prices are falling—especially if consumer sentiment improves as hard data remain resilient. At first glance that might not appear to be the case, given that the equal-weighted S&P 500® index has underperformed the market capitalization-weighted S&P 500 of late. As shown in the chart below, the ratio of the former relative to the latter has fallen to its lowest since 2009.

However, it's worth noting that the equal-weighted S&P 500 is not experiencing an outright decline; the above ratio is being driven lower by the outperformance of some of the largest companies in the index. If the equal-weighted index were to reverse course and start falling again, we would view that with a heightened degree of caution. So far this year, it hasn't happened.

Fixed income: Expect a bumpy road

Bond yields rose over the past month as hopes for a near-term interest rate cut were dashed at the January Federal Reserve Open Market Committee (FOMC) meeting. The Fed not only left its policy rate—the federal funds rate—unchanged, but Fed Chair Jerome Powell went on to indicate that a cut in March was unlikely, citing lack of confidence that inflation would stay low amid a resilient economy. Consequently, Treasury yields have risen by 15 to 25 basis points over the past month.1

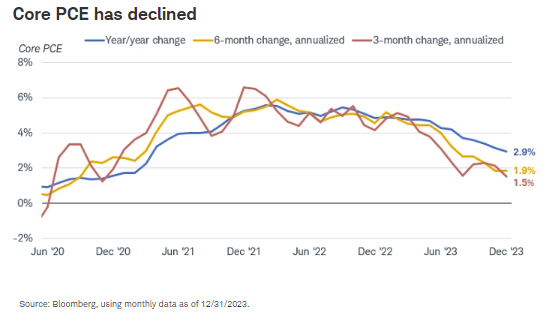

We continue to expect the Fed to begin a rate-cutting cycle mid-year, likely at the May or June FOMC meeting. By then, inflation should have been near the Fed's 2% target for nearly nine months. Based on the Fed's benchmark inflation measure—the deflator for personal consumption expenditures excluding food and energy (or core PCE)—inflation is already at 2% when measured on a three- or six-month rate-of-change basis. A few more tame monthly readings and the year-over-year change should be down to 2%.

In the interim, we expect the Fed to announce a plan to slow its quantitative tightening program (QT), a process it began in 2022 that involves not reinvesting all the proceeds of maturing securities, thereby reducing the amount of bonds on its balance sheet. Tapering QT would be a signal that the Fed is laying the groundwork for an interest-rate-easing cycle.

Despite the recent disappointment from the Fed, investor demand for bonds remains strong. Bidding in the quarterly Treasury auctions was firm, capping the uptrend in yields (which move inversely to prices). Demand for corporate and municipal bonds remains strong as well, with yield spreads relative to Treasuries holding below long-term averages, despite increased issuance.

Looking ahead, volatility is likely to remain a key feature of the fixed income market. The resilience of the economy is complicating the Fed's job and sending mixed signals to the markets. The economy's ability to weather the impact of sharply higher interest rates suggests more underlying strength than previously believed. However, strong productivity growth suggests that a weak economy and/or recession isn't necessary for inflation to keep falling. There are also concerns about smaller banks with exposure to the commercial real estate market having a negative impact on the larger economy.

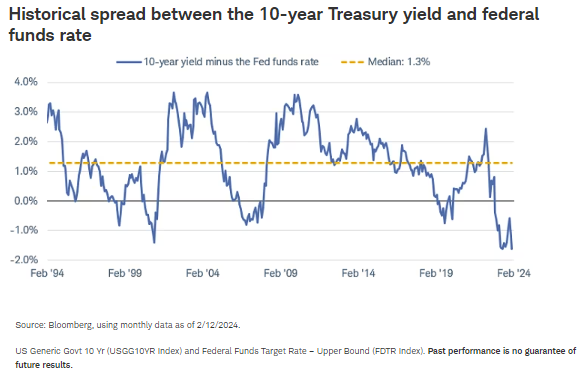

Overall, we expect a gradual easing cycle in the second half of the year, with the Fed cutting three to four times in 25-basis-point increments, bringing the upper bound of the federal funds rate down to a range of 4.5% to 4.75%. The yield curve is likely to steepen as short-term rates fall faster than long-term rates. Nonetheless, yields are likely to drop across all maturities. Based on the deeply negative long-term spread between the federal funds rate and 10-year Treasury yields, there is room for yields to fall from current levels.

For investors, we see opportunities in core bonds—Treasuries, other government-backed securities, and investment-grade corporate and municipal bonds—to lock in attractive yields in the vicinity of 5%. It may be a bumpy ride, but overall trends suggest positive returns are likely in the fixed income markets this year.

Global stocks and economy: China policy mystery

One of the big challenges analysts face is policy changes, which have had a big impact on China's economy in recent years. Policies like zero-COVID rules, the crackdown on big tech companies, and restrictions on leverage at property developers have seemed to come with no warning and little clarity.

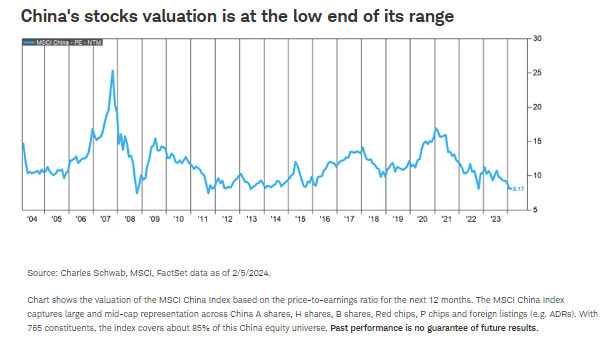

Stocks in China, representing nearly a quarter of the MSCI Emerging Market index, are inexpensive relative to their history. Their single-digit price-to-earnings ratio is close to the bottom of its 20-year range, as you can see in the chart below.

We saw much of the pressure on China's stock market begin in 2020, when a new government policy enacted restrictions on the property market in an effort to crack down on the buildup of leverage in the industry and curb housing speculation. The result starved developers of capital. Could we see China make a policy announcement addressing this issue, sparking a sharp stock market rebound? We saw a similar response when the zero-COVID restrictions were dropped in late 2022; China's stocks shot up 60% over a three-month period. On March 5, there is a meeting of the National People's Congress when China's leaders are expected to announce their economic target for the year (likely to be around 5%), which may be accompanied by new policies intended to support that growth.

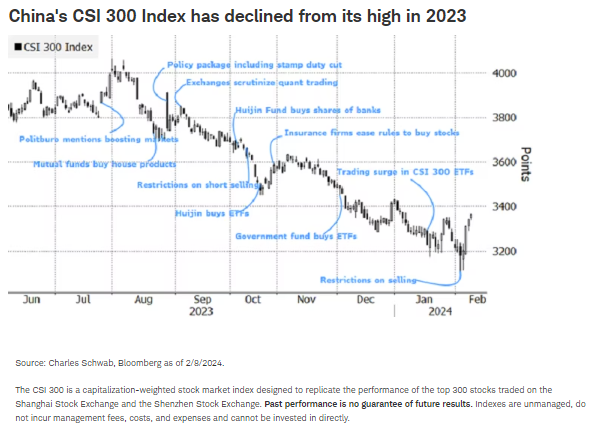

Recent policy changes announced by China's government have not inspired analysts and investors. For the 11th time in six months Chinese officials targeted the stock market, tightening trading restrictions, banning some hedge funds from placing sell orders, and adjusting margin calls to limit forced selling. The head of its securities regulator was also replaced. Earlier changes have included curbs on short selling as well as government share purchases in the nation's largest banks. Yet these measures have shown little success in restoring investor confidence. China's CSI 300 Index tumbled to a five-year low in early February and is still down about 40% from its peak of three years ago. The recent policy announcements targeting the stock market have only resulted in temporary pauses in selling over the past six months.

These policy failures persist because the stock market reaction is a symptom, not the problem. Measures to revive the Chinese economy have been a slow drip of policies, characterized as reactive, uncoordinated, and targeted rather than prompt and broad. They have not been sufficient to support a sustainable turnaround in consumer confidence, which remains low due to weakness in their biggest asset: property.

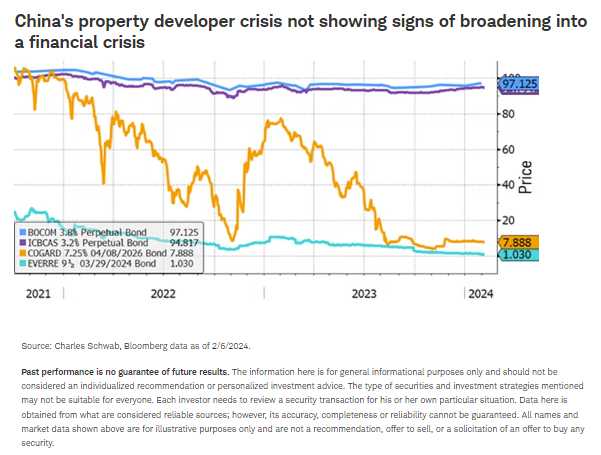

Homeowners who put down big deposits with developers to build a home are now worried about not receiving their home or not getting their money back from failing developers, so they've pulled back on their spending. A policy change in the form of a government guarantee of homebuyer deposits at troubled property developers could help boost consumer confidence from its recession-like lows. This solution could be effective since China does not appear to be experiencing a housing-driven financial crisis. Country Garden (COGARD) was China's largest developer by contracted sales in 2022 after it took the top spot from Evergrande (EVERRE); the bonds of those two troubled property developers are both priced to go out of business, trading at less than 10% of face value. Meanwhile, other high-yield Chinese bonds, including banks like Bank of Communications (BOCOM) and Industrial and Commercial Bank of China (ICBCAS), are trading near par value (we are using these bonds as examples only to illustrate a point).

Focusing policy changes on the stock market misses the point and is likely to fail again without further policy measures to address the real problem. There are no signs of an imminent and major shift in policy—but one could come with no warning, explaining why the gains in China's stock market often come in brief surges amid longer periods of malaise.

Kevin Gordon, Senior Investment Strategist, contributed to this report.

1 A basis point is one one-hundredth of a percentage point, or .001%.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Supporting documentation for any claims or statistical information is available upon request.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or 'Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits