2024 Elections: What Are the Trade Risks?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGlobal elections may lean towards nationalist policies that could hinder trade in goods via tariffs, but also boost growth in domestic industries to counter inflationary effects.

It may seem to many investors that the U.S. election is the only political event in 2024 given how much time has been devoted to coverage and how long the campaigns have been featured in the daily flow of news despite still being 239 days away. Election campaigns in other countries are much shorter and seem to garner much less coverage, despite their significance:

- In Mexico, the campaign spans 90 days.

- In Australia, it lasts 38 days.

- In the United Kingdom, its 25 days.

- In France, the presidential campaign is only 14 days long.

- In Japan, it is limited to 12 days.

While this makes us wonder what citizens of other countries do with all their free time and the money saved from campaign donations, the question we're exploring is how will all the election activity this year impact investors? Voters in over 80 nations and territories—representing more than half the world's population—are expected to head to the polls this year. These span the year from January's election in Taiwan, to India holding the world's largest election this spring, the European Union's 27 countries electing a new European Parliament during the summer (amid other important regional and national European elections this year), the U.S. election in the fall, and a U.K. election this coming winter (by January 2025).

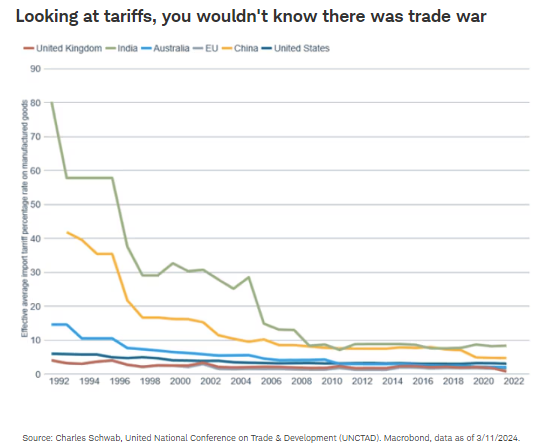

A broad theme may emerge across elections this year: the potential for outcomes that encourage nationalist policies that may hinder trade in manufactured goods. Markets could respond negatively to an outlook for rising tariffs and trade frictions that could boost inflation and weigh on exports. Despite all the talk of trade war over the past eight years, tariffs have moved very little, as you can see in the chart below. Will that change given the sweeping elections of 2024?

Taiwan (January)

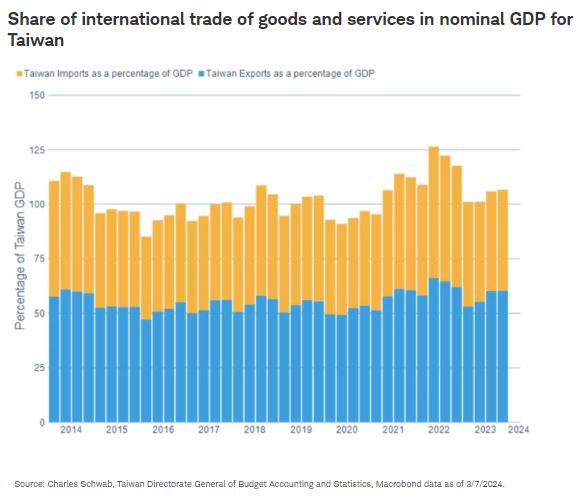

Taiwan holds an important position in the global economy. It is a top player in the world's information and communications technology industry as well as a major supplier of goods across the industrial spectrum. Taiwan's economy is highly dependent on international trade, with exports making up more than 60% of GDP, well above the share tied to domestic consumer spending, according to official data from Taiwan's Directorate General of Budget Accounting and Statistics. Exports and imports combined sum to over 100% of Taiwan's GDP, as you can see in the chart below.

China makes up 22% of Taiwan's exports, more than double the next largest country's (Japan) share of 9%. This export-dependent economy may be impacted by any Chinese efforts to isolate it from the rest of the world. Seeking to lessen this dependence on China, Taiwan has been seeking to join a major regional alliance called the Comprehensive and Progressive Agreement for Trans-Pacific Partnership. However, China has also applied to join the CPTPP and has sent a clear message through their Chinese Foreign Ministry to countries in that trade agreement that they are only to admit China, not Taiwan, consistent with the "one China" view. Taiwan has also been seeking to form a network of bilateral free trade deals. For example, under the ruling pro-independence DPP (Democratic Progressive Party), Taiwan has sought to expand the trade agreement with the U.S. into one that more closely resembles a free trade deal. However, these efforts could be made harder by the DPP's loss of control of the Legislature in January's election and the rise in influence of the KMT (Kuomintang) which seeks a closer relationship with China and has eventual reunification in its charter.

India (April-May)

Prime Minister Modi and his BJP party dominate Indian politics and are likely do well in the upcoming elections. While India has demonstrated protectionist tendencies, the Modi administration is shifting focus towards further lowering trade barriers to increase India's share of global manufacturing exports. In fact, the Modi administration is nearing the final stage of trade talks with the U.K. and negotiations are ongoing with Australia and the European Union, according to government officials. Rather than fight trade battles using tariffs, India seems to focus more on subsidies.

When deep-pocketed governments try to outspend each other to lure investment, less-wealthy nations are often negatively impacted because they can't compete to offer the same incentives. As with tariffs, subsidies undermine the goal of a level competitive playing field in global trade. They raise costs for companies and consumers and, sometimes, hinder the industries they were designed to help. India has as long tradition of favoring domestic industries with subsidies but is now extending them in order to lure foreign manufacturers to India. India's Production Linked Incentive (PLI) program is delivering subsidies to 27 of the world's biggest tech hardware companies, including Apple supplier Foxconn Technology Group and computer giant Lenovo Group, to boost domestic manufacturing and lure businesses from other Asian countries to become a major hub in the global electronics supply chain.

Mexico (June)

In contrast to the other election in North America this year between two men who have both held the presidency before, the winner of Mexico's election will almost certainly be a woman for the first time in North American history. While both female candidates lead the pack of contenders by a wide margin, the preferred candidate of Mexico's populist President Obrador, Claudia Sheinbaum, has a comfortable lead.

A win by Sheinbaum may continue Obrador's initiatives which included a subsidy to Mexico's state-owned oil firm Petroleos Mexicanos, or Pemex, of approximately $4.1 billion in tax relief in February. Sheinbaum has stated that she wants to use subsidies to Pemex as a platform to build out Mexico's renewable technology landscape, but a heavy debt burden may require more state aid. In contrast, her opponent, Xochitl Galvez, has criticized government subsidies to the oil firm. She wants to "modernize" Pemex while giving private companies a larger role in Mexico's energy production markets.

The United States-Mexico-Canada Agreement (USMCA), which substituted the North America Free Trade Agreement (NAFTA) during Trump's first term, helped propel Mexico to become the U.S.'s largest trading partner. A joint review of the agreement is required six years after its entry into force which would be July 2026. The next presidents of both the U.S. and Mexico will review the USMCA's performance in a global environment that has shifted toward more trade protectionism since the agreement was made. Failure to renew the USMCA would likely complicate investment and business planning and reintroduce significant uncertainty in trade relations between the two nations.

Europe (June)

Potential market-moving elections in Europe include the European Parliament elections, nine national elections, and regional elections in major countries like Germany. Across Europe, populist parties focused on nationalist agendas are on the rise. The list of populist successes in 2023 include Geert Wilders in the Netherlands and Giorgia Meloni in Italy—though both have shifted away from more extreme positions they or their parties had held earlier. In contrast, the October 2023 election in Poland saw the ouster of a populist party after eight years in power, replaced by a coalition. But discontent with recessions and elevated inflation in 2023 has fueled the momentum for populists into 2024 with Germany’s populist AfD party polling in second place. In France, populist Marine Le Pen's National Rally party is ahead of President Emmanuel Macron's Renaissance party in opinion polls for the European Parliament elections.

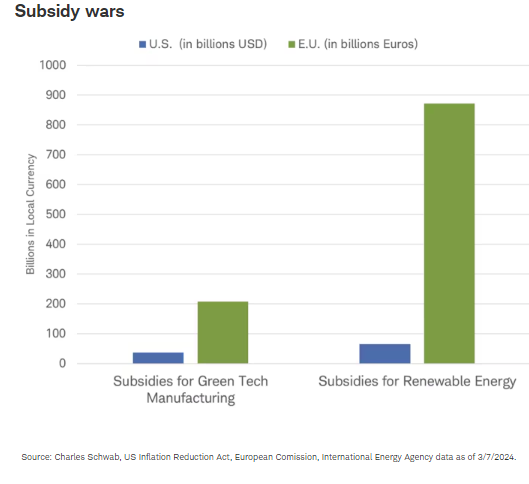

Following the lead of U.S. populists, Europe may move toward a "my country first" system, with higher barriers to the movement of goods and services. The election could also give momentum to a growing "subsidy war." European Commission President von der Leyen responded to the 2023 Inflation Reduction Act in the U.S. that included hundreds of billions in green subsidies from which EU companies will be excluded by declaring that "the new assertive industrial policy of our competitors requires a structural answer." As an example, in January, the European Commission approved 902 million euros in state aid from the German government to Swedish battery maker Northvolt to locate an electric vehicle battery production plant in Germany. This is the first aid to be approved under the new EU state aid regime's "matching clause," which allows member states to match state aid offered by non-EU countries if that financial support risks diverting investment away from the EU. Northvolt had threatened to relocate production plans to the United States to benefit from higher financial incentives available under the U.S. Inflation Reduction Act, according to interviews with the company's cofounder, Paolo Cerruti.

France has been advocating for government subsidies and lobbying for a "Buy European Act" that would incentivize consumers to purchase products made in the EU. Germany, the largest car manufacturer in Europe, appears to be warming up to the French proposals according to statements by German Economic Affairs Minister Habeck. In February, the European Union finalized a deal on a new law to bolster local green tech manufacturing. This Net-Zero Industry Act prioritizes permitting and funding for green technologies, aiding in the fight against mounting competition from the U.S. and China.

United States (November)

The election with the farthest-reaching impact on the world is the one taking place in the United States. Both candidates have had one term in office and were increasingly restrictive on imports. In 2018, President Trump imposed a 25% tariff on approximately $250 billion of imports from China and a 7.5% tariff on approximately another $112 billion of Chinese imports. President Biden retained Trump's trade approach and built upon it including subsidies to attract and retain businesses deemed strategically important, like semiconductors. Continuing the policy of President Trump, Biden has so far held up appointments to the World Trade Organization (WTO) body in charge of dispute settlement, keeping the trade court effectively paralyzed. These trade frictions could extend no matter who wins in November.

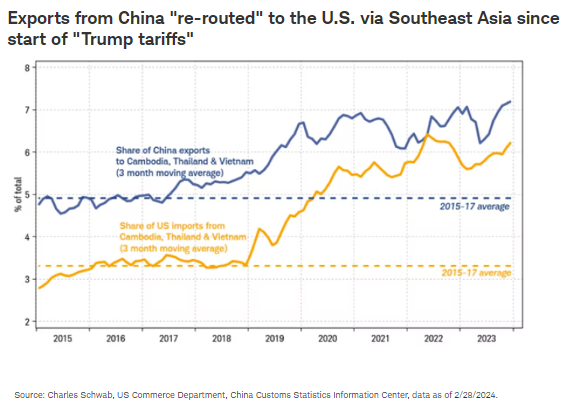

Trump has recently suggested a much larger 60% tariff on China and a 10% universal tariff on other countries. The impact of earlier tariffs targeting China did not lead to any de-globalization of manufacturing nor a rise in inflation. The mild deflationary trend continued uninterrupted in 2018 and 2019, before the pandemic struck in 2020. One reason inflation remained subdued is that U.S. importers seemed to be able to get around the tariffs by importing from other emerging market countries, rather than being forced to buy from U.S. manufacturers. The drop in imports to the U.S. from China looks to have been offset by the increase in imports to the U.S. from Vietnam, Cambodia, and Thailand. China exports to those three countries look to have increased by the same amount. The same scenario could play out with additional tariffs, mitigating any potential China tariff impact.

United Kingdom (by January 2025)

Conservatives are widely assumed to lose the upcoming U.K. parliamentary election, making the election an outlier from the global trend pointing toward right-leaning nationalist party wins. This suggests a closer UK-EU relationship ahead on defense, regulation, and trade after years of a Brexit-induced widening. Yet, the United Kingdom remains highly unlikely to reach a free trade agreement with the United States, which was touted as one of Brexit's key benefits, due to a lack of support in Washington for new free trade agreements.

One of those times

We often remind investors that economics and markets typically have a bigger impact on elections than the other way around. That may again be seen in election outcomes this year given the lingering voter dissatisfaction with the economic and inflation environment. But there are periods when elections can have a significant impact on the markets and economy. The scale of elections in 2024 and the cross-border theme of rising nationalism and trade frictions suggest this may be one of those times.

Yet before we brace our portfolios for the potential for tariffs to slow manufacturing export growth and lead to higher inflation, it is significant that "my country first" trade policy involves more than just tariffs. It increasingly includes incentives to support domestic industries, such as: subsides, tax breaks, accelerated depreciation, and R&D grants. These could result in more capital spending and production, in turn fostering more growth and less inflation and act as an offset to tariffs. While the overall trends may be increasingly clear—the outcomes for investors are not. There will be a lot to monitor in the election outcomes and campaign promises over the course of 2024.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author’s views as of that date. It will be kept solely for historical purposes, and the author’s opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits