Schwab Market Perspective: Under the Surface

The U.S. economy has continued to sail relatively smoothly, although there is a lot going on below the surface. The Federal Reserve is waiting for inflation to drop low enough—and to stay there—before cutting interest rates, but lingering concerns about potential inflation pressures have put the timing of rate cuts in question. Meanwhile, a manufacturing recovery appears to be underway globally.

U.S. stocks and economy: Economic and market divergences

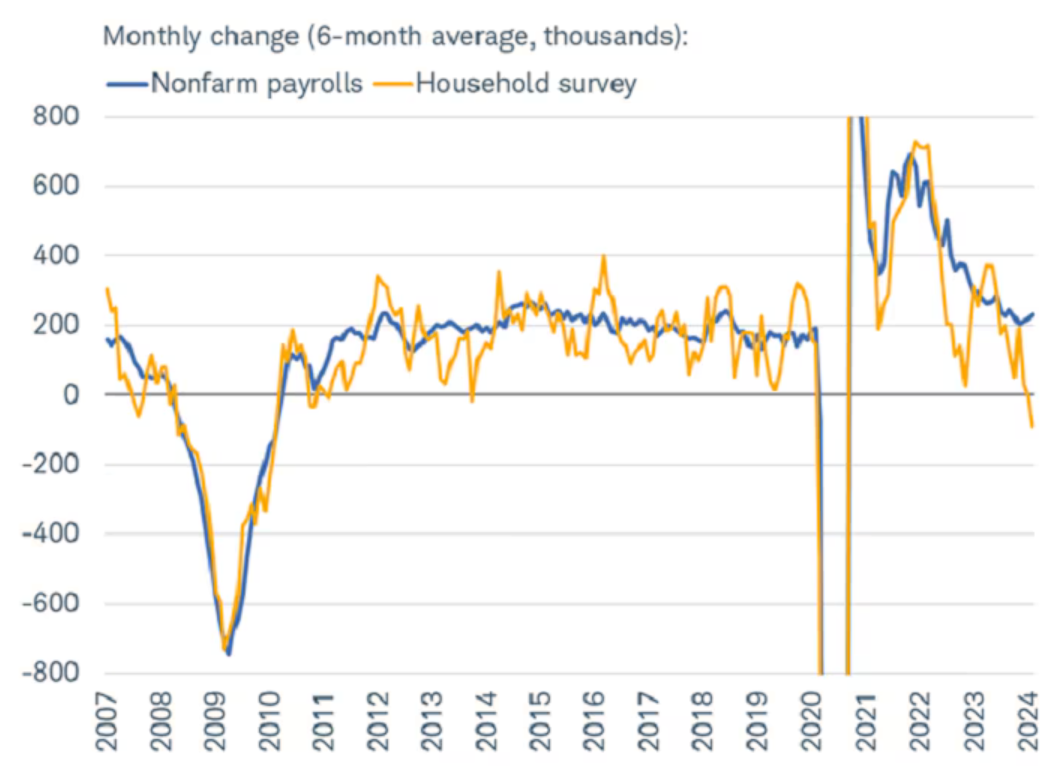

We previously have described the current U.S. stock market environment as resembling a duck: calm on the surface but paddling hard underneath. The same can be said of the labor market. On the surface, data points like payroll gains and the unemployment rate continue to look resilient. The U.S. economy has added 231,000 jobs per month, on average, during the past six months, as of the February employment report, while the unemployment rate has been below 4% for 25 consecutive months.

Yet there are still cracks under the surface. Revisions to prior months' payroll data continue to skew negative, full-time job growth has been anemic, and the closely watched household survey (from which the unemployment rate is calculated) has declined for three consecutive months. The decline in household employment might not sound alarming at first, but looking at the average gain (or lack thereof) during the past six months, the trend has continued to worsen, as shown in the chart below.

Household employment has weakened

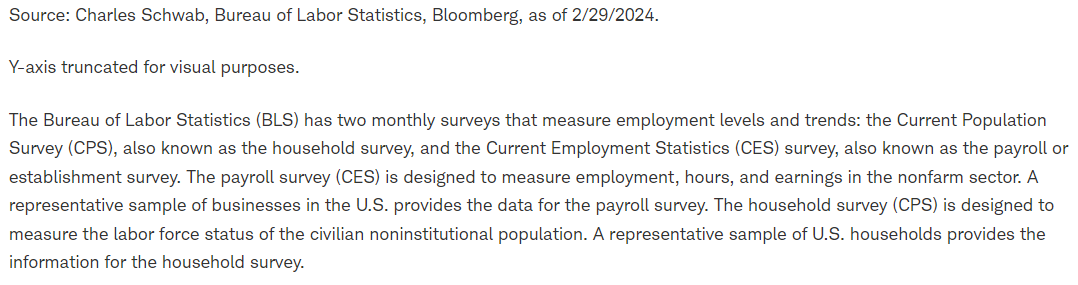

We think that any continued deterioration in the labor market ultimately will be the determining factor for when and how aggressively the Federal Reserve starts cutting interest rates. This also hinges on a continued downtrend in inflation, however. While the Fed's preferred metric, personal consumption expenditures (PCE) minus food and energy (or "core" PCE), has been moving lower and closer to the Fed's target, Fed officials do not appear confident that monetary policy should be adjusted in the near term.

One driver of uneasiness might be that unit labor costs—or how much a business pays its workers to produce one unit of output—are still growing at a 2.5% annual rate, at least as of the end of 2023. This is remarkably lower than the high of 6.5% reached earlier in this rate-hike cycle, which began in March 2022, but it's faster than the average pace during the prior cycle (2015-2018).

Disinflation trend in place

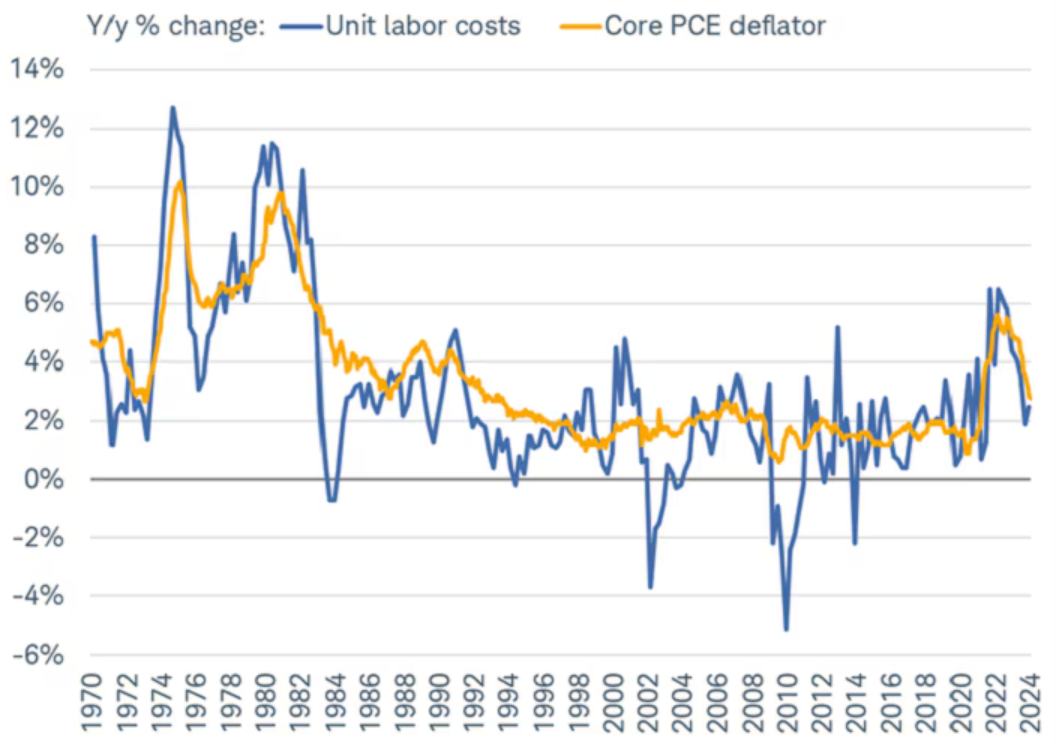

In general, there has been a broadening out in the rally since last October, when the S&P 500® index reached the trough of its most recent 10% correction. Although the "Magnificent 7" mega-cap stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla, which together make up about one-third of the S&P 500 index market capitalization) have, when viewed as an index, outperformed the broader market, both the market-cap-weighted and equal-weighted S&P 500 indexes are tracking closely with each other—a welcome shift given the dominance of the market-cap-weighted index last year.

Not just a mega-cap world

While the "average stock" (represented by the equal-weight S&P 500) has done better over the past handful of months, there has been a narrowing in performance within the Magnificent 7. Three of its members—Apple, Tesla, and Alphabet—were down year-to-date as of March 8th, while the top performer in the group, Nvidia, was up by more than 70% year-to-date. We think this continues to underscore the benefits of volatility-based rebalancing as well as diversification within and across sectors.

Fixed income: Waiting on the Fed

Treasury yields have shifted lower during the past month, but the move was muted by uncertainty about the direction of Federal Reserve policy. It's likely that the trend toward lower interest rates will remain bumpy, but we continue to see potential opportunities in the fixed income markets for investors.

Federal Reserve Chair Jerome Powell recently confirmed that the direction of travel for the federal funds rate is lower. In congressional testimony in early March, he said the Fed likely will cut interest rates later this year but didn't provide any guidance on the magnitude or pace of those cuts. He indicated that the Fed needed more data before initiating rate cuts, to be confident that inflation is heading toward its 2% target level and will stay there. His comments, along with evidence that inflation and the labor market are cooling off, provided the basis for a strong rally in the bond market.

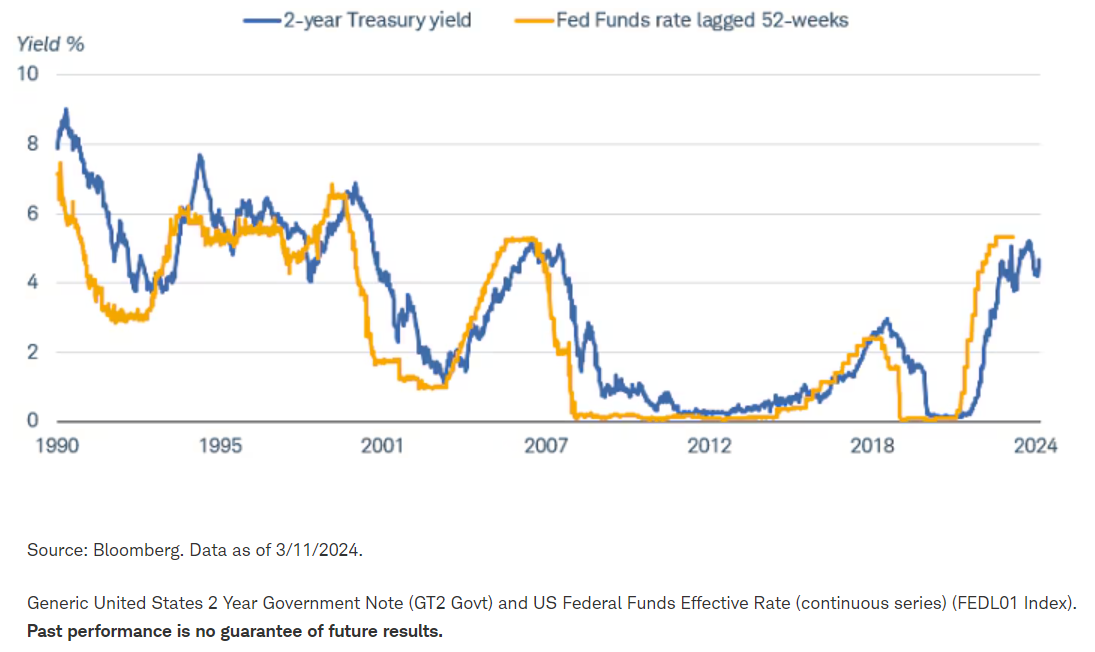

Two-year Treasury yields have fallen more than 20 basis points from the February high of 4.70% to 4.58% (a basis point is one one-hundredth of a percentage point, or 0.01%). Because two-year yields tend to correlate with expectations for the federal funds rate one year into the future, the level implies expectations for 75 to 100 basis points in rate cuts over the next year, which is aligned with our view.

Two-year Treasury yield tends to correlate with expectations for federal funds rate one year in the future

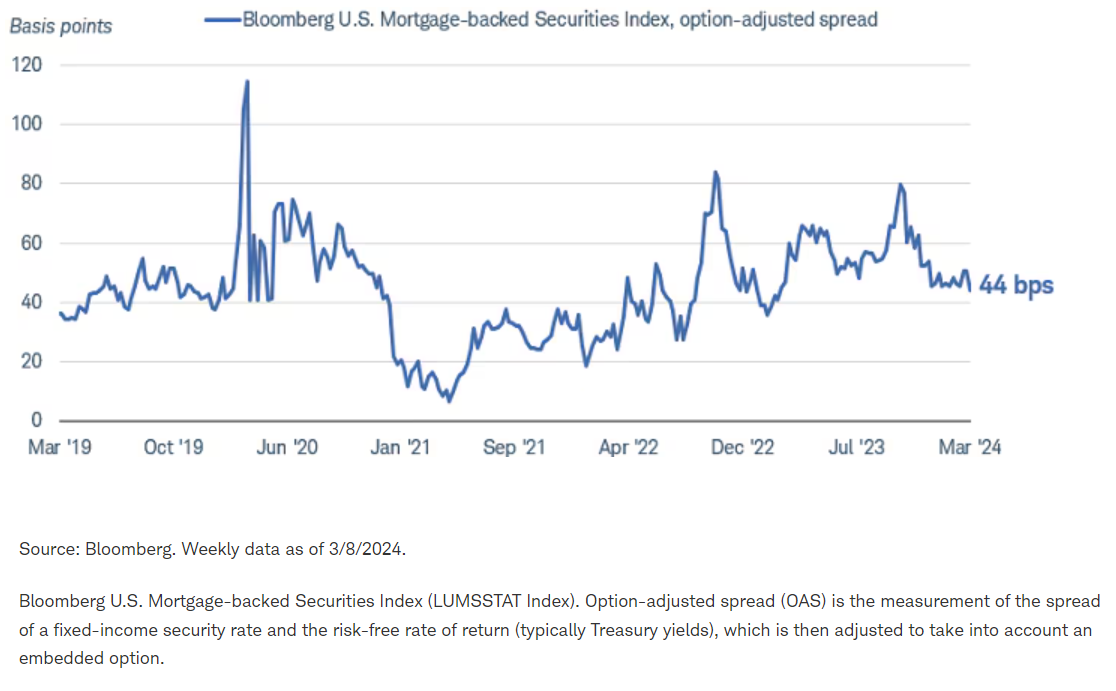

Although yields have fallen significantly from their highs and there is still uncertainty about the timing of rate cuts going forward, we do see potential opportunities in the fixed income markets. We continue to believe investors should consider extending duration1 to avoid reinvestment risk (the risk that proceeds from maturing securities will need to be reinvested at lower rates) as interest rates fall. One alternative to Treasuries would be mortgage-backed securities—those either explicitly or implicitly backed by government agencies, such as the Government National Mortgage Association, Federal National Mortgage Association or Federal Home Loan Banks. These securities currently offer yields that are about 40 to 45 basis points higher than Treasuries of comparable maturity.

Mortgage-backed securities currently offer higher yields than Treasuries

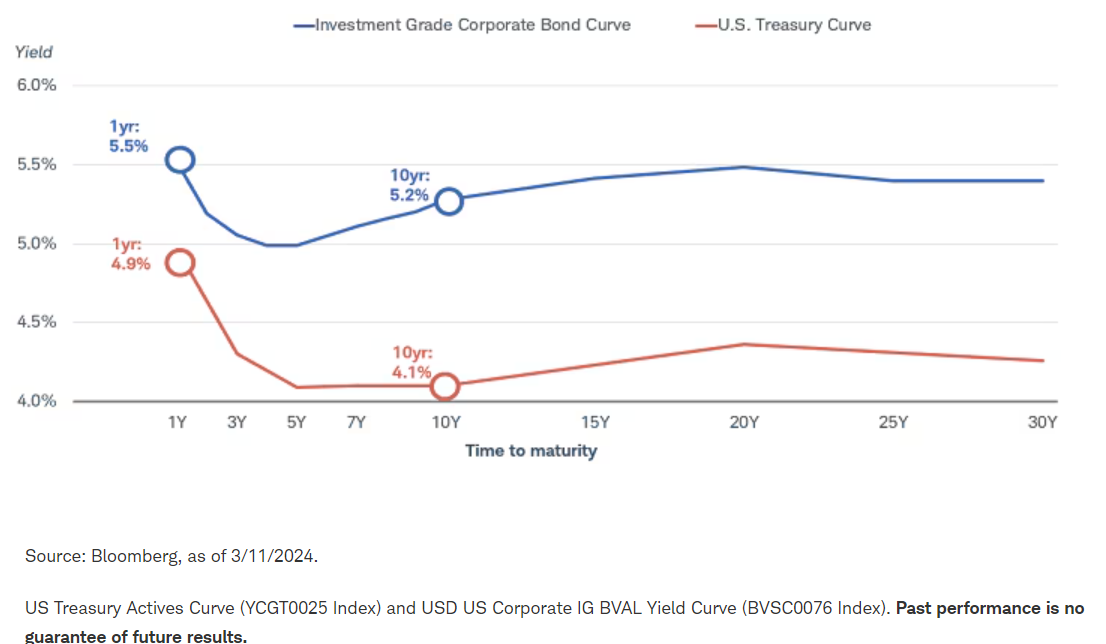

For those aiming to maintain yields near the 5% level and willing to take on a degree of credit risk, it may make sense to use investment-grade corporate bonds rather than Treasuries when adding duration. Yields for maturities of five years and beyond are still higher than 5% and, unlike the Treasury market, the corporate bond yield curve is mostly positively sloped. That means investors potentially will receive more yield when adding duration to portfolios.

The investment-grade bond curve is more positively sloped than the U.S. Treasury curve

There is credit risk compared to Treasuries, but with the economy remaining resilient, the investment-grade corporate bond market outlook is generally positive, in our view. After more than a decade of low yields, we see attractive choices for investors looking to generate income over the next five to 10 years without taking excessive risk.

Global stocks and economy: Cardboard box recovery

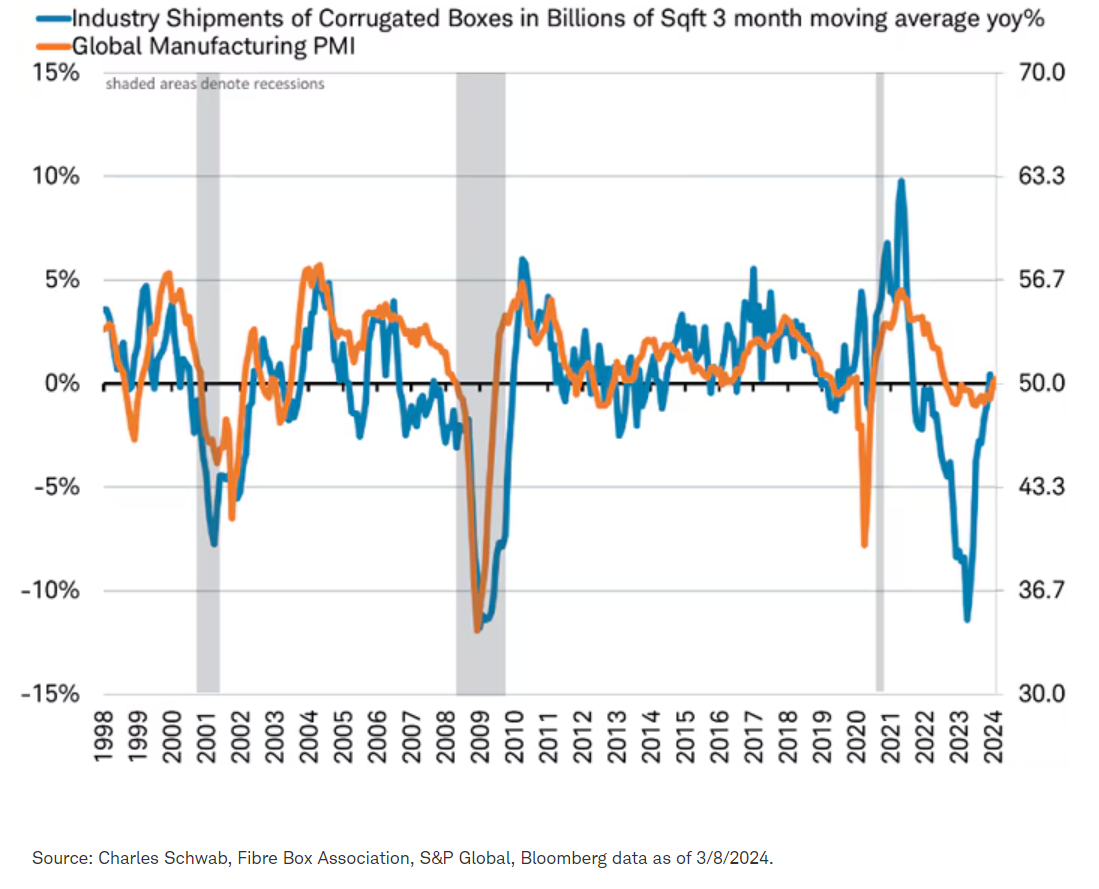

We use the phrase "Cardboard Box" recession to describe the 2023 global downturn, which included last year's recessions in Japan and the United Kingdom, because the weakness was concentrated in manufacturing and trade of goods—things that tend to go in cardboard boxes.

But as we forecast in our 2024 outlook, it appears a "Cardboard Box" recovery is now getting underway. The latest data show that both actual demand for cardboard boxes and sentiment by business leaders in manufacturing have moved back to expansion. The global manufacturing purchasing managers index (PMI) hit 50.3 in February, its first reading in 18 months above the 50.0 mark that divides growth from contraction. A rise in the new-orders component of the survey signaled more growth is likely.

Global manufacturing returns to growth

If the recovery continues, we might see a change in economic and market sector leadership from last year. We expect a brighter outlook for economic and earnings growth from more manufacturing-based sectors and economies, such as Japan. As measured by the Nikkei 225 Index, Japan is the best performing stock market in the world so far this year, rising 19% in yen and 14% in U.S. dollars.

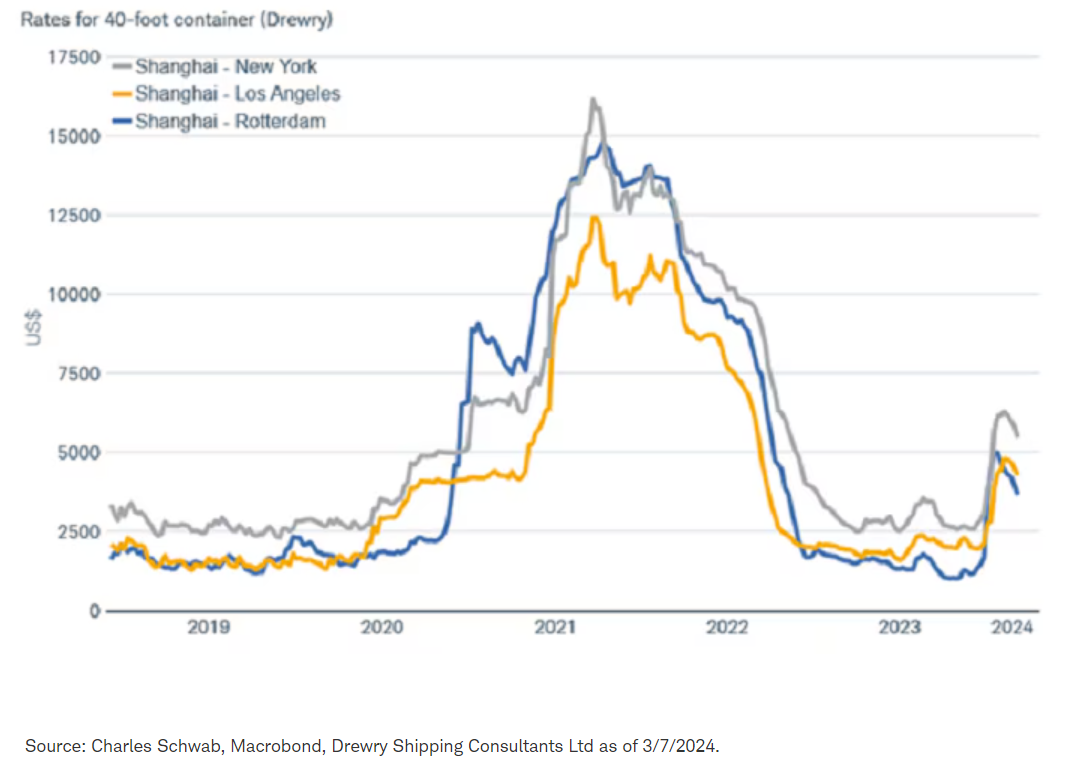

Do supply chain issues pose a problem for this recovery? Back in January, Houthi attacks began diverting container ships from the Red Sea/Gulf of Aden and forcing them to go around Africa, a much longer and more expensive journey. The Panama Canal also experienced dramatic weather-related restrictions on the number of ships passing through the vital global shipping chokepoint, forcing them to take the long trip around South America.

The rise in costs from the sudden shortage of shipping capacity as ships took longer to reach their destinations no longer appears to be worsening, although prices remain elevated. While seasonal factors have been muted in the wild swings of recent years, spring in the Northern Hemisphere is a period historically associated with declining container shipping prices.

We acknowledge that there could be a seasonal driver to the decline, and perhaps there may still be price increases (on a seasonally adjusted basis) signaling continued rising supply chain pressures. We will have to keep an eye on it, but for now it seems that the shipping cost increases related to the rerouting of container ships may have peaked.

Soaring container shipping rates now may be fading

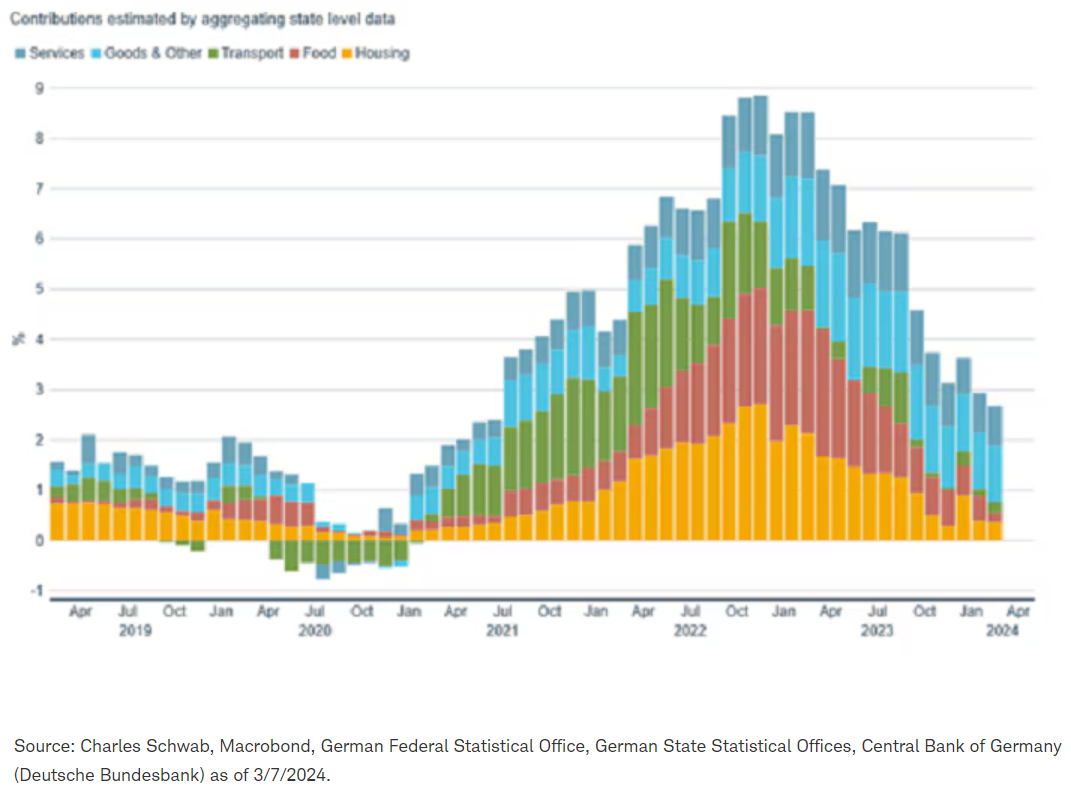

Inflation in Germany, France, and Spain slowed in February, despite rising shipping rates. In the breakdown of the German consumer price index (CPI) data, transportation costs (green in the chart below) rose only slightly despite the substantial rise in February's seaborne costs. That suggests that higher shipping costs may have limited impact on inflation and may not be enough to offset other factors keeping inflation trending lower. If shipping prices peaked in February, the declines may further the disinflationary trend and keep the European Central Bank on a path toward rate cuts in June.

Germany: Contributions to inflation

Kevin Gordon, Senior Investment Strategist, contributed to this report.

1 Duration measures the sensitivity of a bond’s price to changes in interest rates. It's not the same as time to maturity, which does not change with the interest rate environment. Duration is nonlinear and accelerates as the time to maturity lessens.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.