Too many companies with solid earnings growth haven’t been rewarded in narrow equity markets. That may be about to change.

Global equities advanced briskly in the first quarter as investors reconciled themselves to a new reality of interest rates staying higher for longer than expected. With macroeconomic concerns beginning to recede, we think earnings growth is poised to take center stage as a driver of stock returns for a wider group of companies across equity markets.

When the year began, many investors believed that a series of interest-rate cuts from major central banks was imminent. While the range of potential macro outcomes was wide, the consensus anticipated a rapid succession of rate cuts early in the year to signal that the battle against inflation had been won.

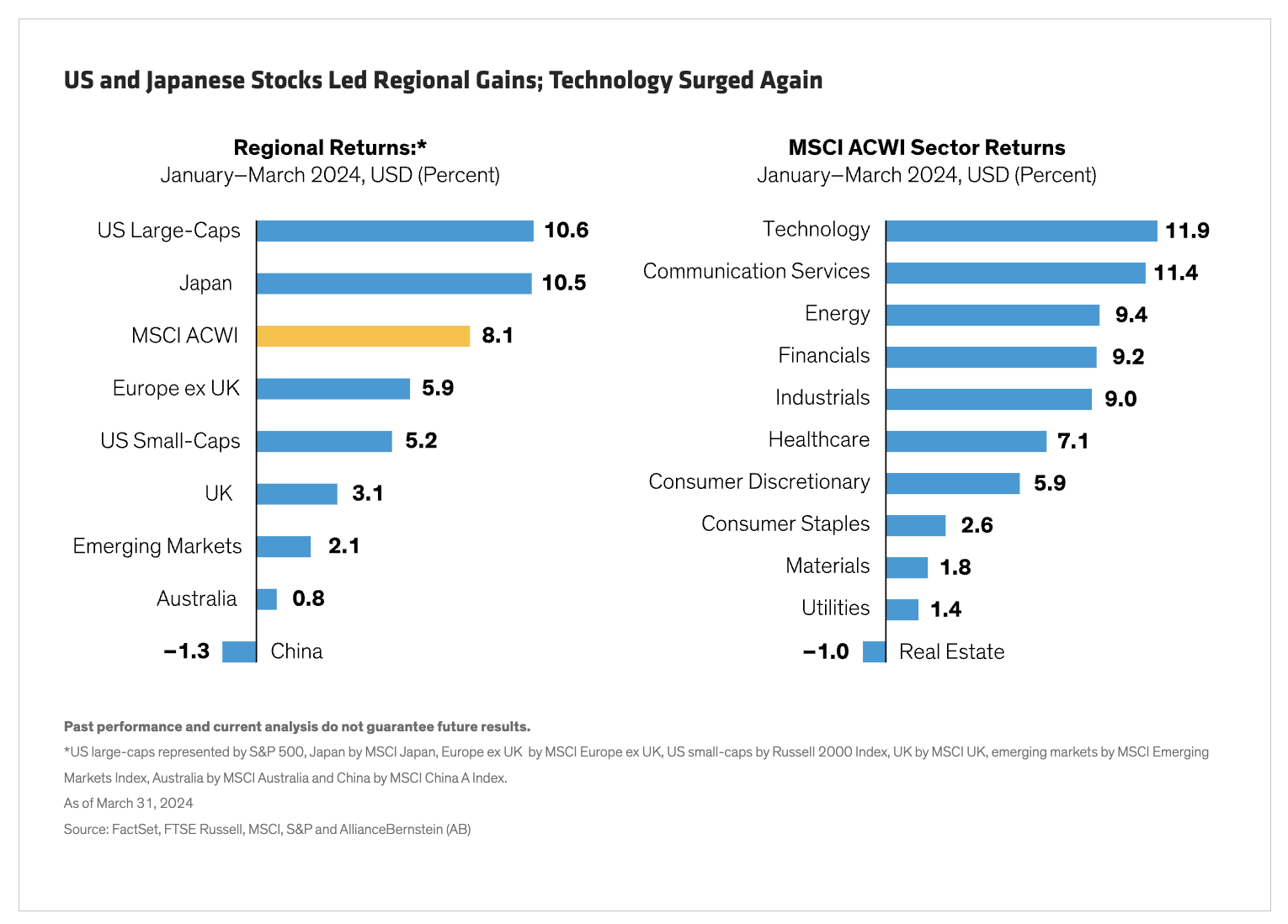

That didn’t happen, and yet the MSCI All Country World Index (ACWI) climbed by 8.1% in US-dollar terms in the first quarter. Strong gains in Japanese stocks weren’t undermined after the Bank of Japan raised interest rates for the first time in 17 years in late March. Investors in US equities shrugged off the Federal Reserve’s deferral and reduction of rate cuts; markets had started the year anticipating six cuts starting as early as March. In Europe, the rate-cutting cycle is also expected to begin midyear. Investors seem to have accepted that relatively high interest rates in fact reflect a stronger economy and have recalibrated expectations accordingly.

Turning Point for Equity Markets?

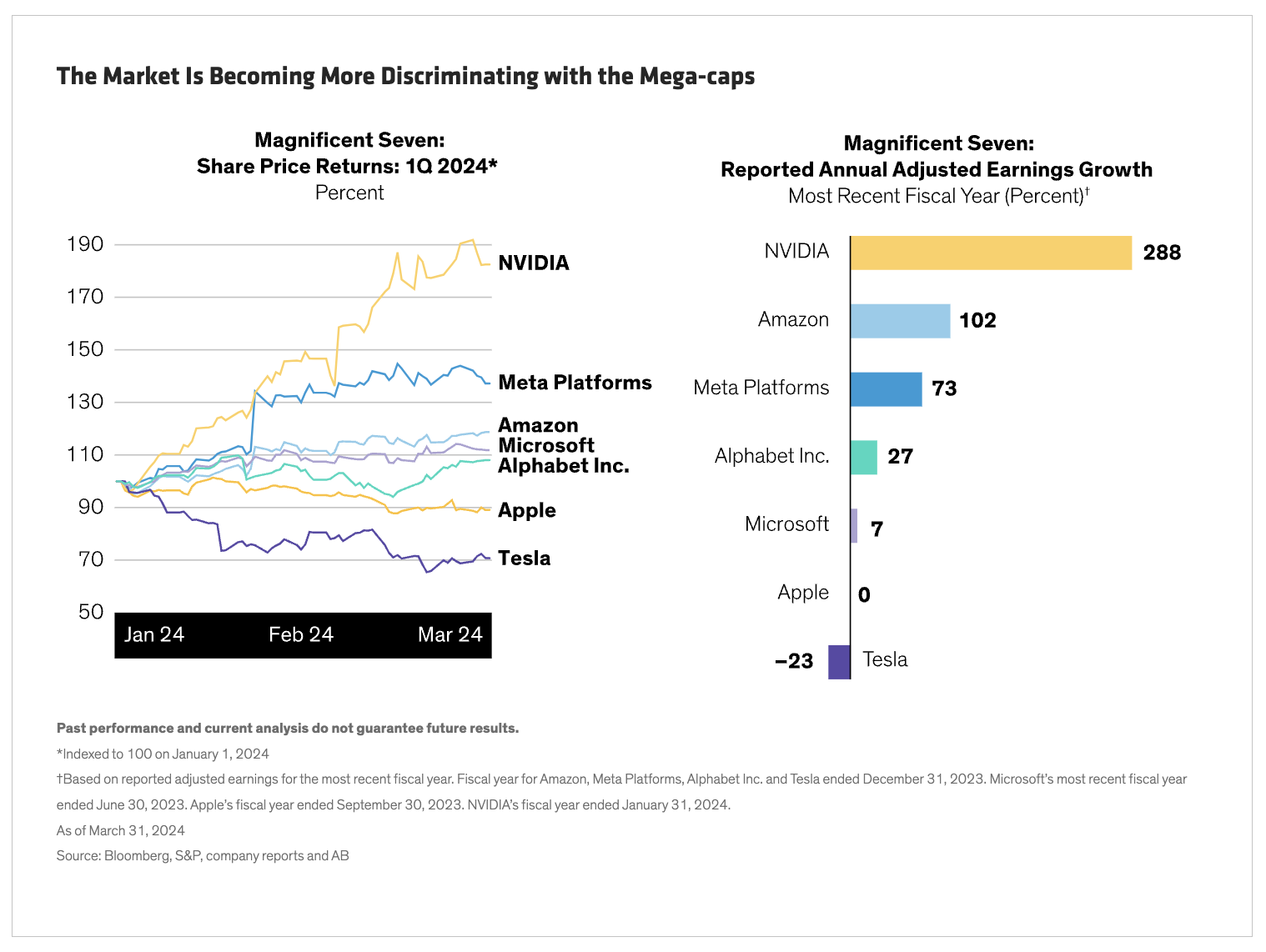

The market’s resilience reflects a potential turning point for equity investors, in our view. After a prolonged period during which concerns about inflation, growth and interest rates dominated return patterns, we think corporate profits are regaining prominence—and growing optimism on the earnings outlook has propelled markets in the first quarter. If this trend continues, we expect equity returns to broaden, following the extreme concentration of markets in the Magnificent Seven, a small group of US mega-cap stocks, over the last year.

On the surface, it might seem as though little has changed. During the first quarter, global growth stocks outperformed value stocks, as they did last year. Technology remained firmly at the top of US and global sector returns.

But beneath the surface, this doesn’t look like a rerun of 2023. For one, the Magnificent Seven, seen as the biggest beneficiaries of artificial intelligence (AI), didn’t behave like a cohesive cluster. NVIDIA towered above the group while Apple and Tesla declined sharply. We don’t think AI enthusiasm is a bubble about to burst, because it’s being driven by real earnings growth across the technology industry, unlike during the dot-com bubble. However, diverging returns within the Magnificent Seven did reflect differences in each company’s business results, based on reported earnings growth for the full-year 2023.

Change Is in the Air: Key Indicators Begin to Shift

It’s too soon to say whether these patterns will persist within the mega-caps or across the broader market. But there is a whiff of change in the air, which we’ve sensed in some key indicators.

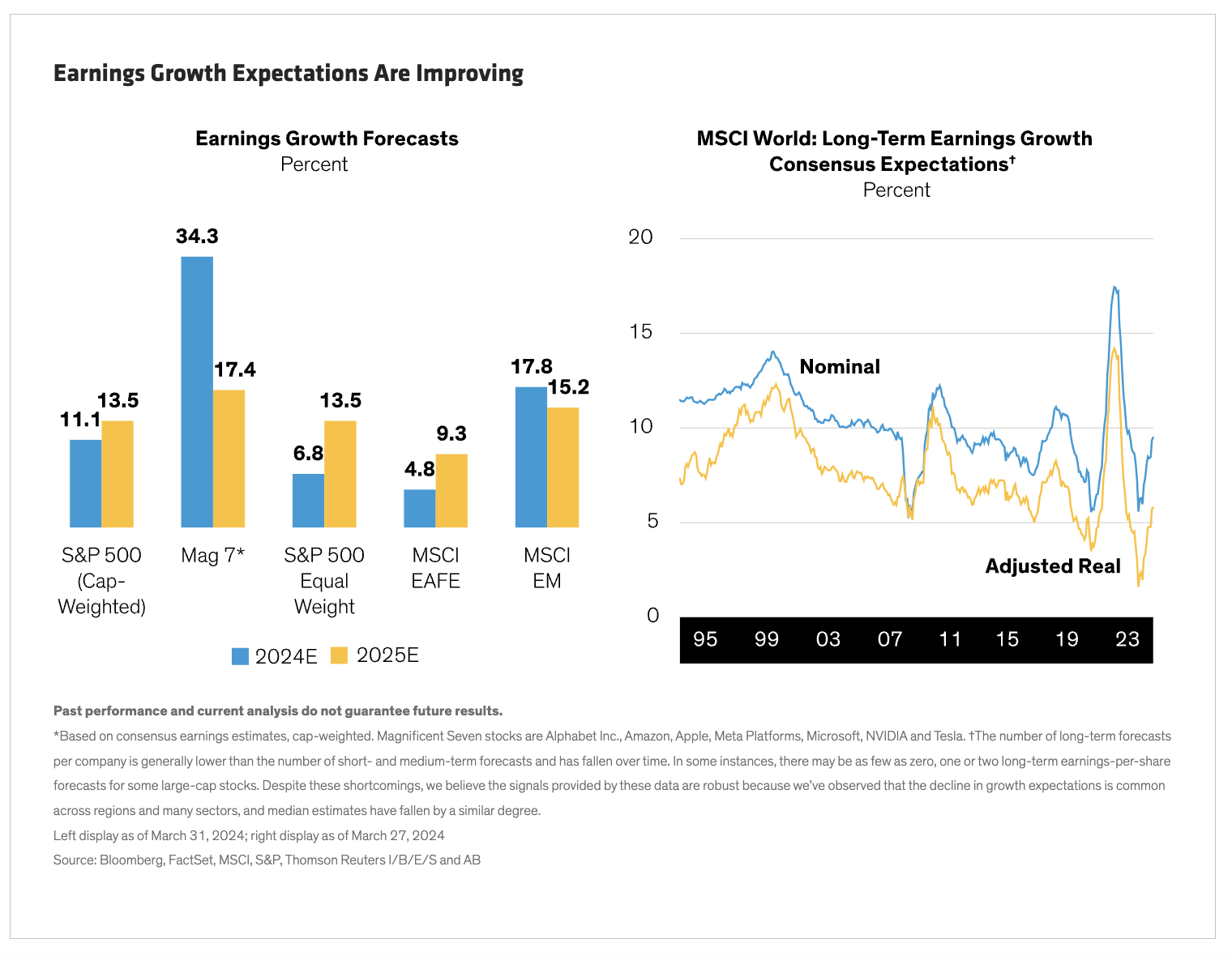

Earnings growth looks promising, in our view, and not just for the mega-caps. While the Magnificent Seven stocks as a group still boast higher earnings growth potential than the broader market, we believe investors must be very selective in how they access this; the divergence of first-quarter returns within the cohort reinforced this lesson.

Beyond the mega-caps, consensus earnings forecasts are picking up. Despite regional differences, we believe investors can find pockets of attractive growth opportunities in Europe and emerging markets, and even in China, despite its struggling economy.

Globally, we think the long-term earnings outlook is promising, too. Our research indicates that global earnings growth forecasts for three to five years ahead have risen from extreme lows a year ago in nominal and real terms yet remain low in historical perspective. In other words, now is a good time to capture the potential for further improvements ahead.

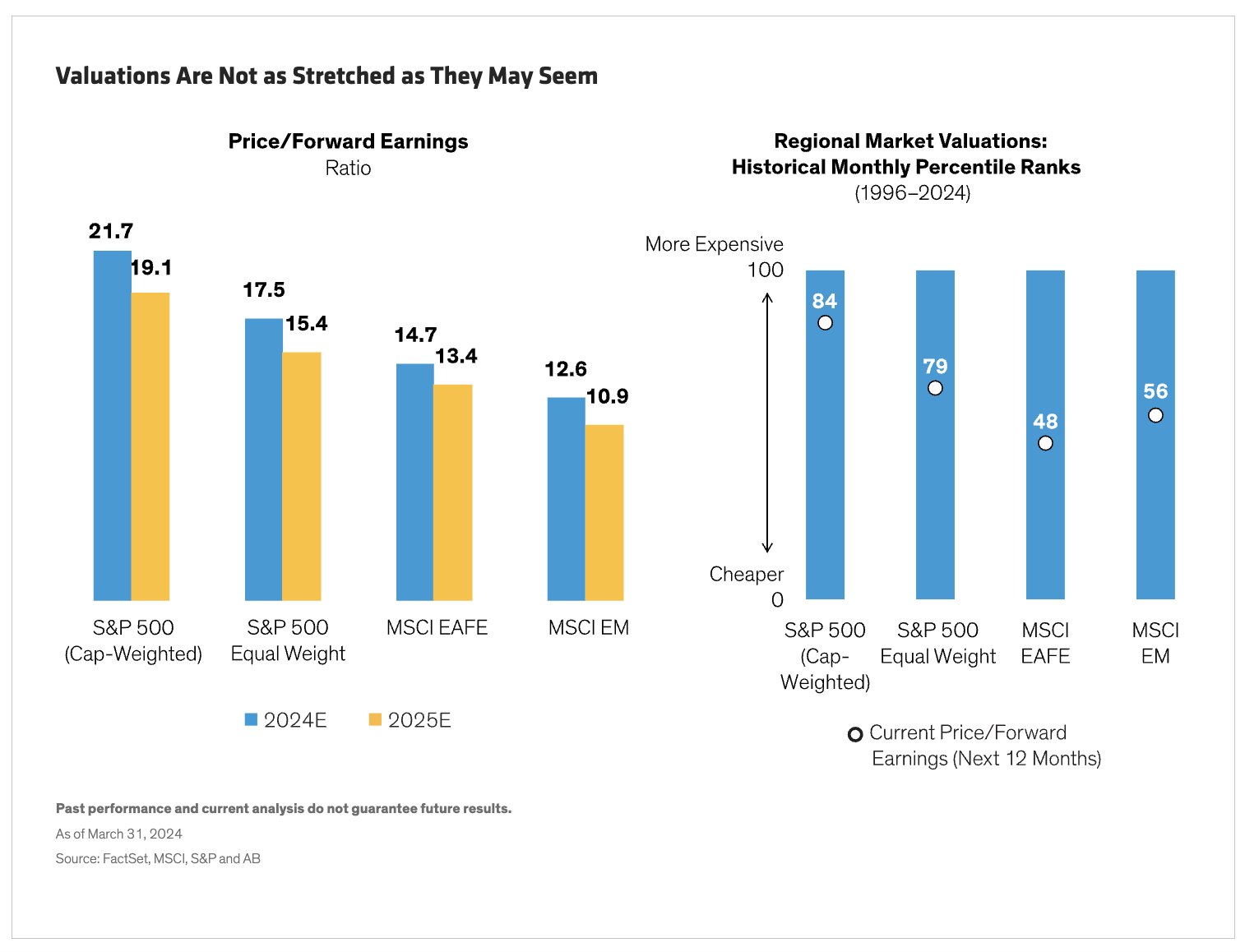

Meanwhile, valuations are not as extreme as they may seem. US stock valuations have been stretched by the Magnificent Seven. But beyond the mega-caps, we believe attractively valued opportunities can be found in companies with unappreciated earnings growth potential. The S&P 500 Equal Weight index, which better represents the broader US equity market, is trading at significantly lower price-to-forward earnings valuations than the cap-weighted index. Outside the US, valuations are lower, with shares in Europe, Australasia and the Far East (MSCI EAFE), as well as emerging-market stocks, trading at reasonably attractive levels relative to their long-term history.

Strategic Mindset for a Changing Environment

Identifying attractively valued stocks with strong earnings growth potential will require a strategic mindset that is attuned to the changing environment. We believe equities will remain vital for investors to generate real returns, above levels of inflation that are higher than we’ve seen over the last decade. However, the hurdle to achieving positive real returns will be higher. And even if interest rates come down, a higher level of nominal rates will compound the challenges to companies and investors.

In this environment, we believe companies that can consistently earn above their cost of capital will be rewarded, while those that cannot do so will likely lag behind. High-quality businesses and fundamentals will be prized. Healthy balance sheets, sound business models, competitive advantages and management skill will all be vital to delivering earnings growth in the years ahead that can support equity returns above inflation.

Unfamiliar and evolving conditions will affect the fortunes of companies. As this process unfolds, we expect the dispersion of earnings outcomes and stock returns to continue to widen—as seen this quarter in the divergence between NVIDIA and Apple. This, in turn, should create fertile ground for active managers to select stocks of companies that have not yet been recognized for their resilience and growth prospects. Even after a strong first quarter for stocks, we think equity portfolios that focus on business fundamentals through a clear earnings lens can capture attractive long-term return potential for investors as the market transitions to a new normal.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

References to specific securities discussed are not to be considered recommendations by AllianceBernstein L.P.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein