Economic indicators are released every week to provide insight into the overall health and performance of an economy. They serve as essential tools for policymakers, advisors, investors, and businesses because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending on April 4th, the SPDR S&P 500 ETF Trust (SPY) fell 1.91% while the Invesco S&P 500® Equal Weight ETF (RSP) was down 2.34%.

Among all economic indicators, some of the most closely watched are those surrounding the labor market. Not only do they provide insight into the health of the economy, but they impact individual’s lives and play a central role in government policy decisions. Last week featured a handful of employment updates including the BLS’s March Employment Report, February’s Job Openings and Labor Turnover (JOLTS) report, and March’s ADP Private Employment Report. Each of these reports offer insights into different aspects of the U.S. labor market. This article will highlight the key data points from each report and explore their potential implications.

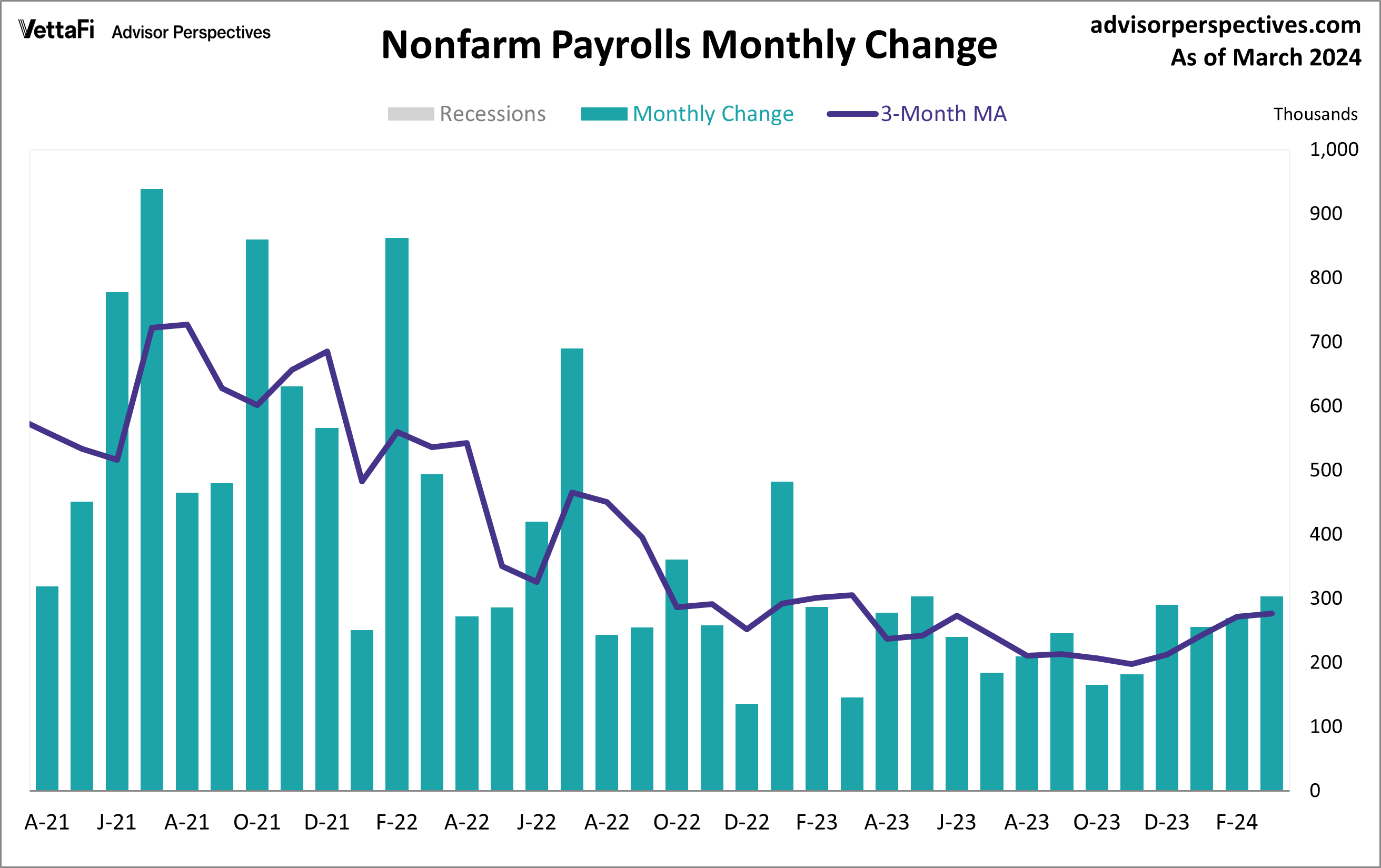

Employment Report

The U.S. labor market added more jobs than expected last month while the unemployment rate inched down, pointing to a strong and resilient labor market. The March employment report revealed 303,000 jobs were added last month, surpassing the expected 212,000 addition. March’s jobs numbers were a pickup from February’s revised 270,000 addition and the largest monthly gain in over a year.

The report also indicated that the unemployment rate fell to 3.8% while the labor force participation rate increased to 62.7%. Additionally, wage growth increased 0.3% from February and slowed to 4.1% on an annual basis.

Overall, the latest jobs report showed a much stronger than expected labor market and reinforces the Fed’s position of patience with regards to when they will begin cutting rates.

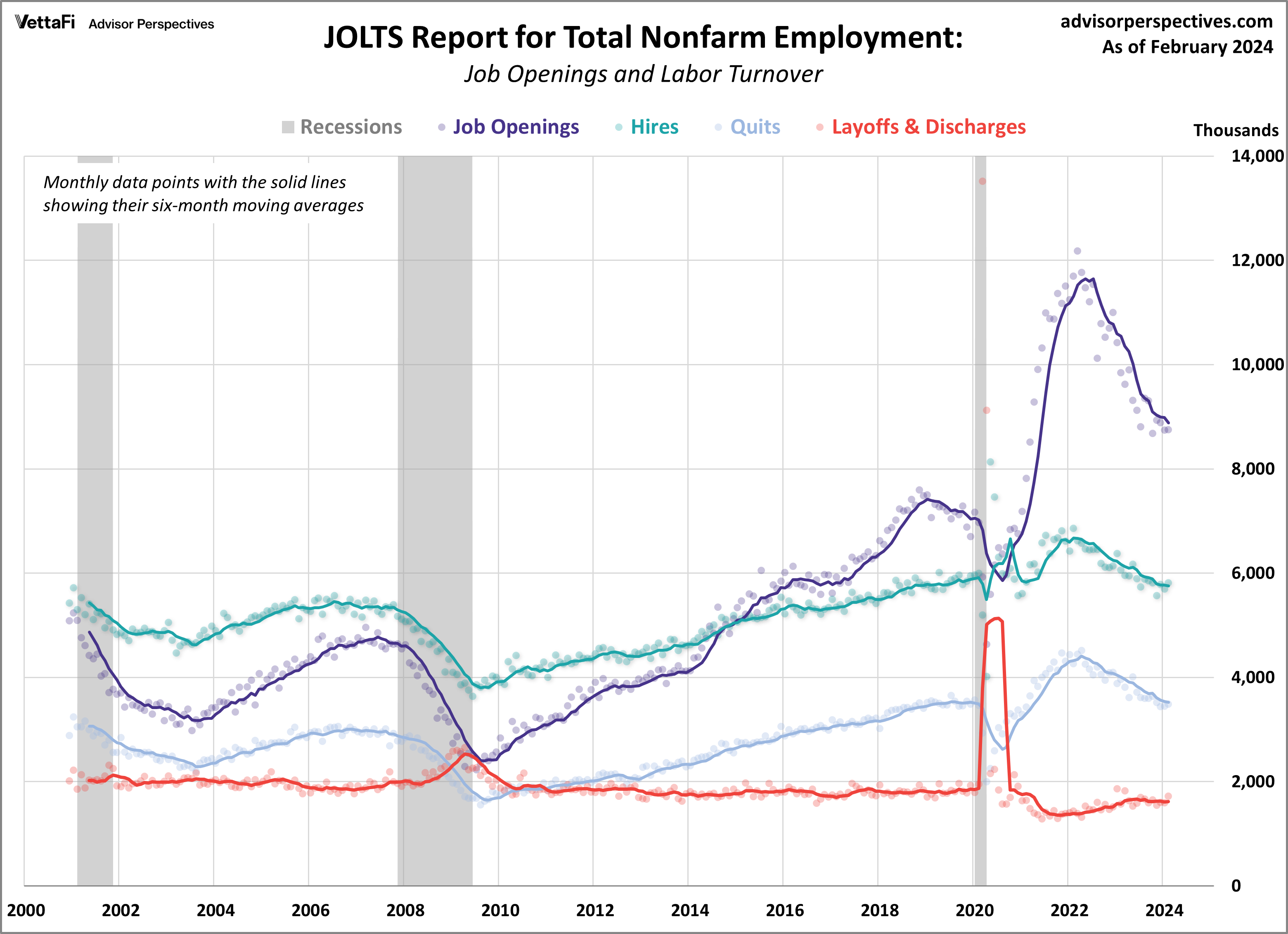

Job Openings and Labor Turnover (JOLTS)

The latest JOLTS report revealed that the labor market was little changed for a second straight month in February. The number of job openings inched up by 8,000 from January to 8.756 million and came in just below the predicted 8.760 million vacancies. Other key data points from the report showed that the number of hires, quits, and layoffs each rose from the previous month. Most notably, the number of layoffs reached an 11-month high at 1.7 million.

The JOLTS data serves as a barometer for assessing labor demand, and any disparity between workforce demand and supply could potentially exert upward pressure on inflation. For much of 2023, the gap between the two had consistently narrowed as the overall trend in job openings steadily declined from its 2022 peak. In February, the number of job openings per employed worker dropped to 1.36, its lowest level in the past four months.

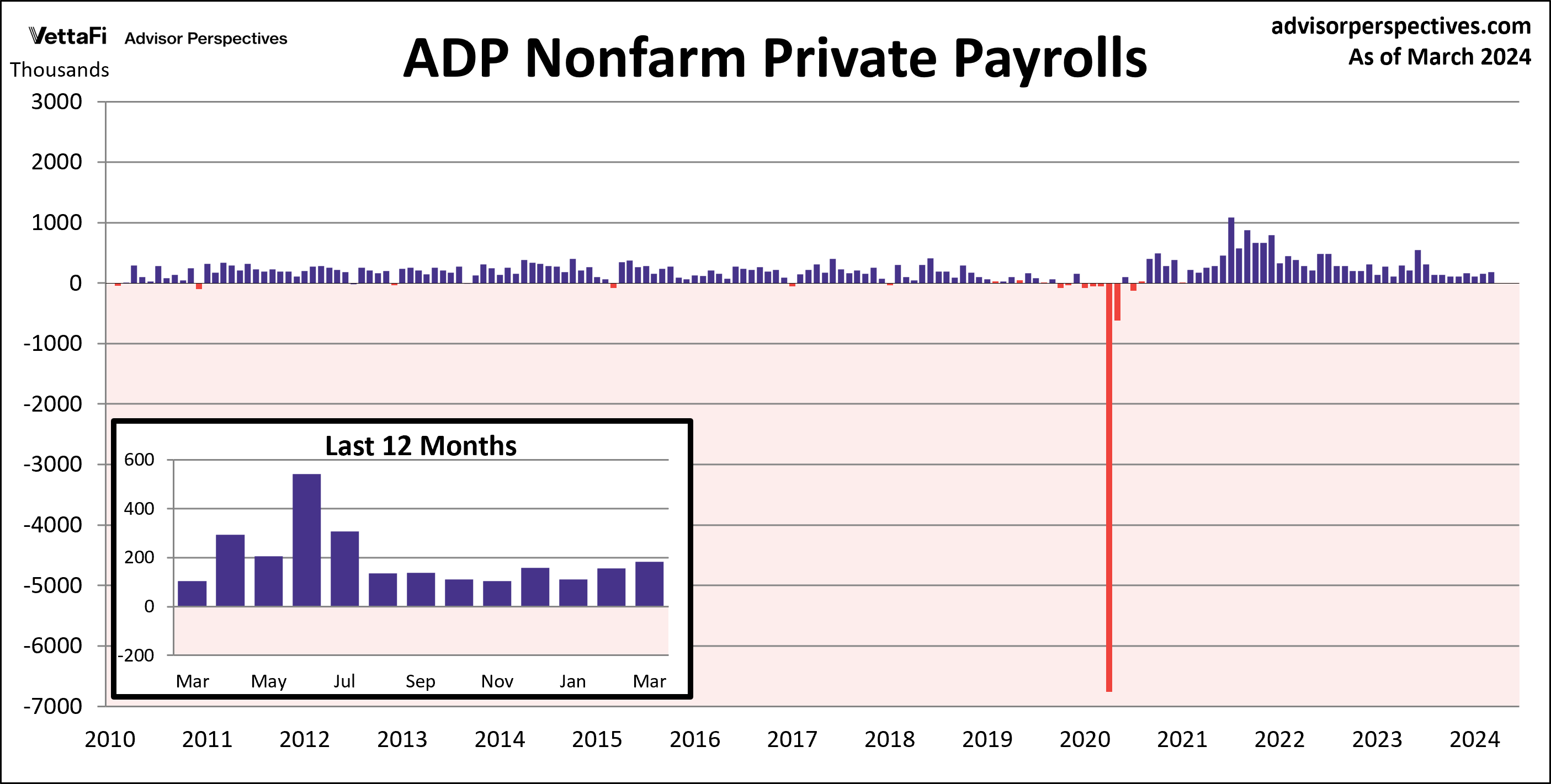

ADP Employment Report

Private sector hiring grew at its fastest pace since July 2023 last month, yet another sign of the labor market’s continued resilience. The ADP employment report showed that 184,000 private jobs were added in March, more than the projected 148,000 addition. The report also revealed a steadying of annual pay growth, with pay gains for job-stayers remaining at 5.1%. Meanwhile, pay gains for job-changers jumped for a second straight month to 10%.

The pickup in March was most notable among large (500+ employees) to mid-size (50-249 employees) companies, as they added 150,000 jobs combined, accounting for approximately 82% of March’s private job growth. The six-month moving average, a more stable indicator amid monthly volatility, increased for a second straight month to 137,000. With that said, the latest average is the third lowest level since November 2020 during the peak of COVID-19 layoffs, beating out only January and February of this year.

Overall, the strong job growth and steady wage gains support the Fed’s position to not rush into a rate-cutting cycle just yet.

Economic Indicators and the Week Ahead

The upcoming week will feature the latest inflation and sentiment data. On Wednesday, the Bureau of Labor Statistics will release March’s Consumer Price Index (CPI) followed by the Producer Price Index (PPI) on Thursday. Consumer prices are expected to increase 0.3% from February for both the headline and core indexes. Producer prices are expected to increase 0.3% and 0.2% for the headline and core indexes, respectively. Then on Friday, the preliminary report for the Michigan Consumer Sentiment Index, which could impact interest in the Consumer Discretionary Select Sector SPDR ETF (XLY), is predicted to remain at March’s final reading of 79.4.

For more news, information, and analysis, visit the Innovative ETFs Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more commentaries by VettaFi