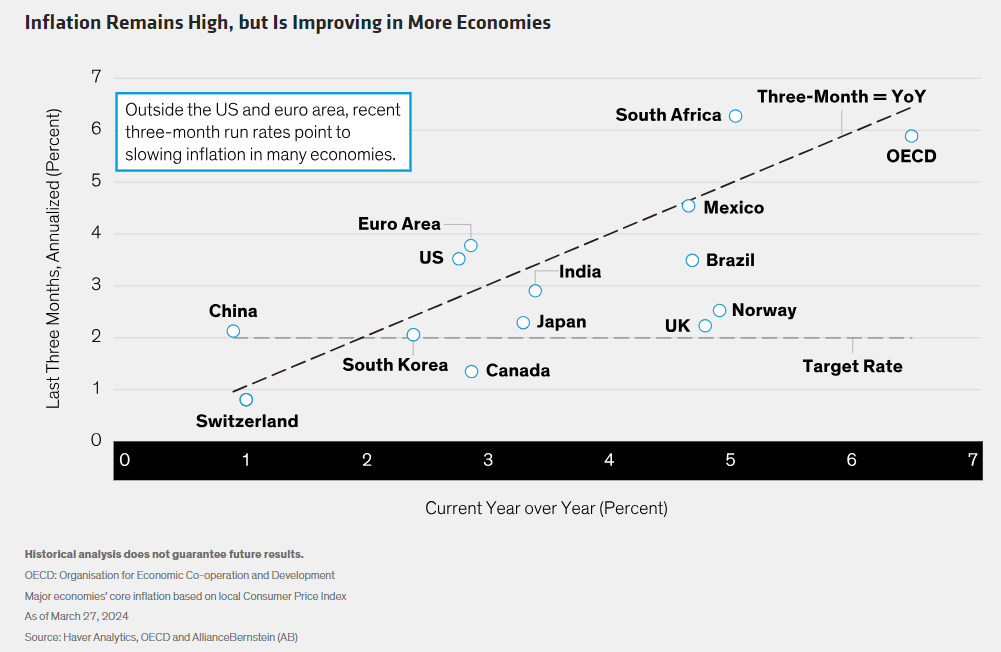

Inflation, one of many inputs to multi-asset decision-making, cooled substantially last year, but upside surprises in early 2024 for the US and Europe have many investors concerned that the path back to normal has hit a roadblock. We don’t think so. In fact, inflation remains in steady retreat—and in more major economies.

In Switzerland and China, for example, inflation is already below 2% year over year. While year-over-year inflation in Canada, Japan, Norway and the UK are above that mark, their three-month run rates point to significant slowing there too.

Progress in reducing inflation slowed somewhat in the US and euro area in early 2024, but core inflation levels are well below 2022’s peaks. It remains just under 3% in the euro area and the US—the latter’s figure based on the Personal Consumption Expenditures Price Index, the Fed’s preferred inflation measure. And potential indicators of sustained inflation—such as home prices and wages—remain well behaved. In the meantime, the consensus on global economic growth has strengthened, suggesting a soft landing ahead.

Fighting inflation is a long game, and global central banks seem to be making continued progress, with most likely to maintain their policy-easing bias despite recent upticks. The Swiss National Bank led the pack with a rate cut of 25 basis points in March, and the ECB appears likely to follow in June. US rate cuts seem likely to be delayed until late 2024, but we believe they’re still on the table.

Inflation and the economic outlook are only two of many inputs to strategic and tactical multi-asset decisions, but we think they represent positive signs for risk assets, including stocks. Of course, investors should also stay nimble and ready to respond to an evolving environment.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

© AllianceBernstein

Read more commentaries by AllianceBernstein