Declaring Independence From the U.S.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDollar strength resulting from central banks' independent policies on rate cuts is unlikely to be tampered by China's deflation or geopolitics.

The Federal Reserve looks to emerge as a global outlier on policy interest rates, likely cutting rates later in this cycle than other major central banks. As the Fed delays the start of cuts, other central banks are declaring independence from the U.S.'s Fed with the European Central Bank's (ECB) Lagarde making that clear in the press conference following the April meeting when she explicitly stated, "We are not Fed dependent." The heads of the Bank of Canada (BOC) and the Bank of England (BOE) also expressed similar sentiments last week. And March saw Swiss officials delivering the first interest rate cut of the current cycle by a central bank with one of the world's 10 most-traded currencies and is expected to lower rates again in June.

Diverging paths

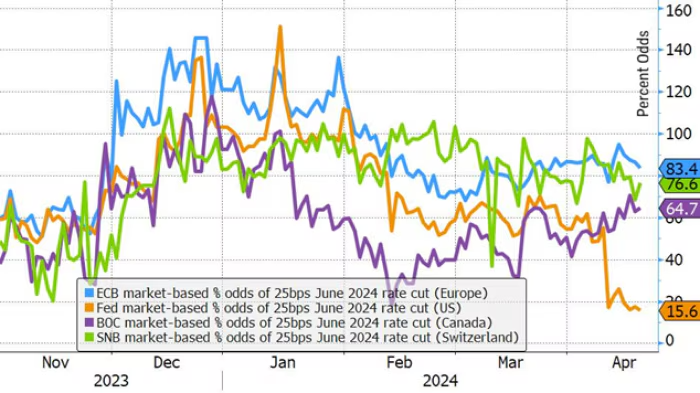

The odds of a 25-basis-point (bp) rate cut by the Fed in June have come down from a "sure thing" at the start of the year to merely a 15% chance in the eyes of the interest rate futures market. At the same time, the odds remain well over 50% for other major central banks, as you can see in the chart below.

Market-based percentage likelihood of a rate cut in June

Looking past June, the outlook for the number of rate cuts priced in for all of 2024 has slipped from between six to seven at the beginning of the year to between one and two for the Fed, and between three and four for the ECB, as you can see in the chart below.

Market-based number of rate cuts priced in for 2024

Source: Charles Schwab, Macrobond, Intercontinental Exchange (ICE), as of 4/18/2024.

Futures, and Futures options trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure Statement for Futures and Options prior to trading futures products. Past performance is no guarantee of future results.

The widening divergence between the outlook for rate cuts in 2024 for the Fed and those of other major central banks is strengthening the dollar since higher interest rates on cash can make holding a currency more attractive. This can have multiple implications for stock market investors:

- A stronger dollar could eventually hurt earnings for U.S. companies through making exports less competitive and weighing on the earnings growth of U.S. companies' overseas-sourced profits. Earnings growth of non-U.S. companies on their U.S. sales could benefit.

- A stronger dollar also boosts commodity exporters and acts as a drag on commodity importers because crude and other industrial goods are typically quoted in dollars. The Energy and Materials sectors tend to do well in this environment (see our latest Sector Views).

- Stock market valuations in countries where rates are likely to be cut more aggressively may rise, offsetting the drag on performance from a falling currency for U.S.-based investors. We have been seeing this effect with the price-to-earnings ratio rising for much of this year for the MSCI EAFE Index, contributing to its total return and offsetting the drag from currency impacts.

Rising valuation offsetting falling currency on total return

Is China the answer to U.S. inflation?

It appears that the stronger and more resilient U.S. inflation picture is helping to drive the diverging policy outlook that is currently lending support to the U.S. dollar. The consumer price index (CPI) surprised on the upside in the U.S. for the past three months, while being lower and surprising on the downside in Europe, Canada, and Switzerland.

Data represents change in CPI from a year ago for each country.

Source: Charles Schwab, Bloomberg data, Statistics Canada, Eurostat, Ministry of Internal Affairs & Communications Swiss Federal Statistical Office, UK Office for National Statistics, US Bureau of Labor Statistics as of 4/18/2024.

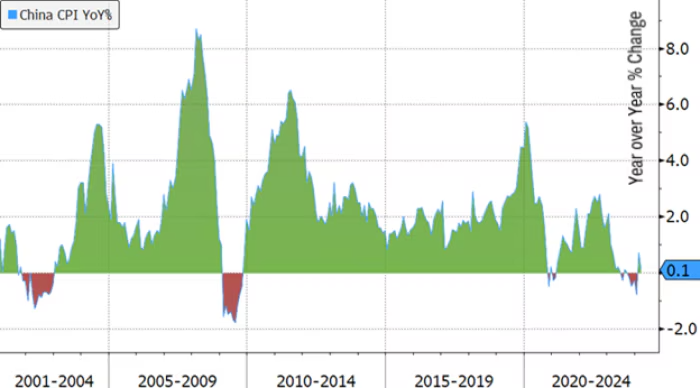

Last week's China first-quarter GDP release illustrated the imbalance between business investment (solid) and consumer spending (weak), as government stimulus efforts remain directed to increasing supply over supporting demand contributing to non-existent inflation.

Inflation in China remains near zero

Source: Charles Schwab, Bloomberg data as of 4/18/2024.

Green areas are periods of positive inflation, and red areas are periods of negative inflation.

However, we believe it is misguided to believe that excess manufacturing capacity in China will result in an export of deflation from China to the rest of the world to help to bring down stubborn U.S. inflation.

- First, among developed economies like the U.S., imports from China make up less than 2% of overall household consumption—with most of the current pace of inflation coming from services which are not imported from China. Services contributed 3.2% of the 3.5% headline CPI for the U.S. in March, and 1.8% of 2.4% headline CPI in the eurozone. Using the same periods, goods prices subtracted from overall U.S. CPI and contributed to only 0.3% to eurozone CPI. The modest impact of lower goods prices is unlikely to offset still high services prices.

- Second, import prices are only a small portion of the final price of a good, which is often more influenced by wholesale and retail services performed in the destination country. The San Francisco Fed estimates nearly half of spending on imports stays in the U.S. paying for the local components of these goods. One example indicated $25 of the $100 price of athletic shoes manufactured in China by a U.S. company went to the Asian factory, while the rest of the price represented profits of the U.S. company, transportation costs, wages for workers in U.S. warehouses and retail stores, rental cost for retail space, insurance, etc.

- And third, China's infrastructure spending and manufacturing stimulus could add to global inflation pressures if greater demand boosts commodity prices, like those for base metals which have tend to be up sharply this year.

Moreover, excess capacity in China is nothing new that would prompt a sudden trade shock. Low levels of capacity utilization have been a feature in China for over a decade, rotating among different industries, with current excess in the automobile industry, according to comments by U.S. Treasury Secretary Yellen and EU Commission chief Ursula von der Leyen. So, it is unlikely that China is the solution to the U.S. inflation problem. Counterintuitively, very low export prices may incite higher tariffs. If the export price is low enough that it prompts lawmakers to institute new and bigger tariffs in efforts to protect domestic industry, it can increase prices for consumers. It would follow then that additional U.S. tariffs on Chinese produced goods, such as the recently proposed rise to steel tariffs, may further boost U.S. inflation and serve as a counterpoint to any arguments for deflationary effects from inexpensive imports.

Is geopolitical risk driving the dollar?

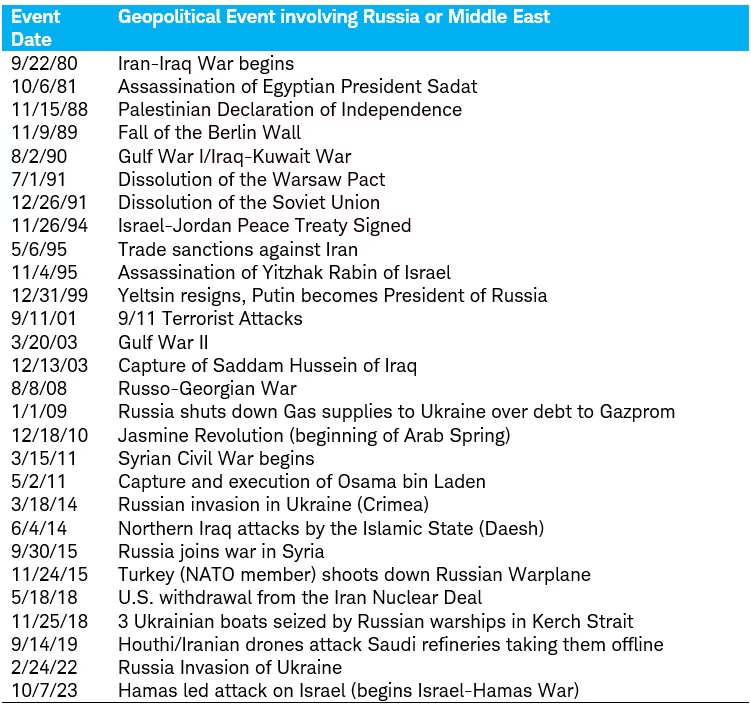

Is the dollar's strength merely a temporary boost tied to geopolitics over the Russia-Ukraine and Hamas-Israel conflicts rather than tied to the diverging outlook for rates? History suggests it isn't likely to be a major factor. We composed this list of 28 past geopolitical events that were indicative of conflicts involving Russia or Middle Eastern countries to illustrate the limited impact those events have had on the markets and the dollar.

Geopolitical events involving Russia or Middle East

Source: Charles Schwab as of 4/15/2024.

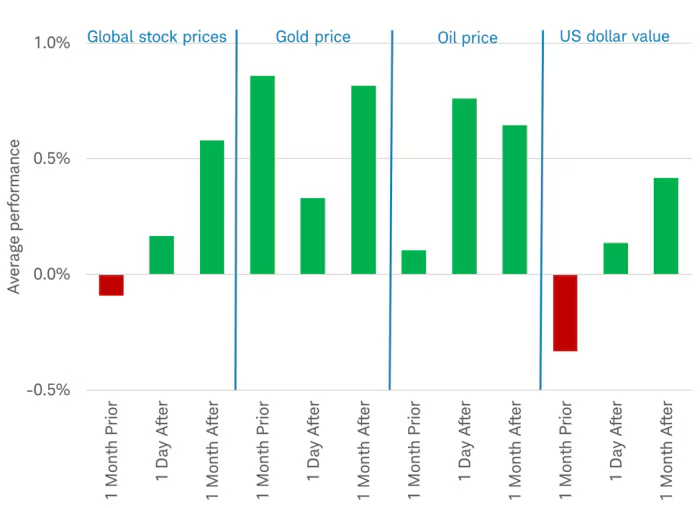

In general, markets tend to move in anticipation of what may come, rather than merely reacting to what already happened. In contrast to a rising dollar on perceived fears of a conflict escalation, the dollar has typically been down in the month leading up to a geopolitical event (43% of the periods in the above table).

Market reactions leading up to and following geopolitical events

Source: Charles Schwab, Bloomberg data as of 4/18/2024.

Global stock prices are illustrated using performance of the MSCI World index. Gold prices are illustrated using Gold/USD futures. Oil prices are illustrated with Brent Crude futures contracts. The value of the U.S. Dollar is illustrated using the U.S. Dollar Index (DXY). Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Global stocks, as represented by the MSCI World Index which includes both U.S. and non-U.S. companies, were up nearly 70% of the time immediately after the events occurred, despite being down slightly most of the time in the lead-up to those events. Gold, oil, and the dollar also climbed on average post-event—although the consistency of those gains (50-61% of the time) was not as high as with stocks (68%).

Of the 28 total periods, global stocks were up in the month prior to the event during 15 of them—a little more than a coin flip and slightly less than the two-thirds of the time that a month posted an average gain over the full 55-year period. Perhaps this softer performance in the month prior to an event reflects some concern over heightened geopolitical tensions. Of those same 15 periods, stocks were down five times one month after the event, three of which were during recessions, making geopolitics unlikely to be a key reason that stocks were down. As for the remaining two periods? The ascendancy of Putin as president of Russia in December 1999 preceded the start of the 2000 Dot Com market crash and the capture of Osama Bin Laden in May 2011 aligned with the European Debt Crisis. In our opinion, these two geopolitical events happened coincidentally with major economic events, making them unlikely to have been a key driver of stocks' declines during those periods.

A 55-year-long look at history shows very few times—if any—that a geopolitical event was a major factor in changing market trends. Of course, there is always the potential for a first time.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Currency trading is speculative, volatile and not suitable for all investors.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0424-YBCT

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All