Do You Have Questions About CRTs? We Have Answers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

It’s complex and confusing, and it’s not a baby anymore. Since its debut in 2013, the credit risk transfer (CRT) market has grown to more than US$50 billion and references roughly US$2 trillion of single-family mortgage loans in the larger $13 trillion mortgage market. But even though it’s over ten years old, the CRT market can feel unfamiliar to investors. Below, we answer your most frequently asked questions.

Why were CRTs created?

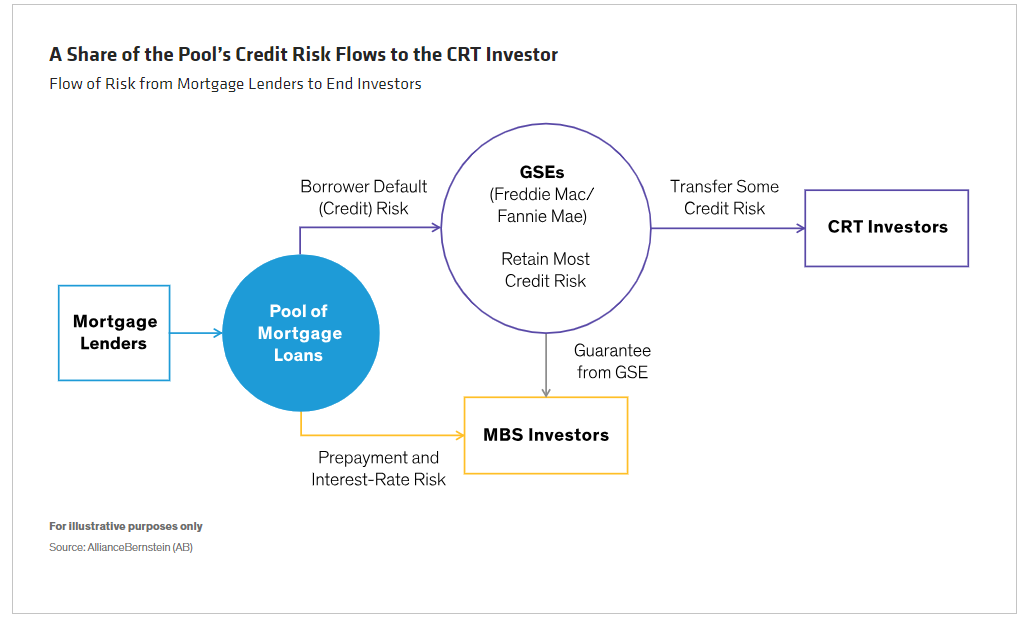

The US government–sponsored enterprises (GSEs) Fannie Mae and Freddie Mac don’t originate mortgage loans themselves. They leave that to banks and other lenders. Instead, the GSEs bundle tens of thousands of individual mortgage loans into mortgage-backed securities (MBS) in which they guarantee that investors will receive all interest and principal.

In exchange for writing these insurance policies, the GSEs charge a “guarantee fee” that functions as an insurance premium. Like any insurance company, the GSEs determine this fee based on what they believe they need to adequately cover losses and expenses. Unlike other large insurance companies, though, the GSEs historically never purchased reinsurance. Thus, the GSEs bore all the risk of homeowner default.

When the global financial crisis struck in 2008, US homeowners defaulted on their mortgages in record numbers, leaving the GSEs—and US taxpayers—on the hook for huge losses. In response, the government placed the GSEs under the authority of the newly created Federal Housing Finance Agency (FHFA).

FHFA assessed ways to reduce the chance that massive losses could strike the federal government and US taxpayers in the future. The GSEs decided to issue securities that would transfer some of the credit default risk of the underlying mortgage loans from the GSEs to investors, with the securities effectively functioning as reinsurance for the GSEs. From the FHFA’s perspective, this transfer of credit risk would not only protect Fannie Mae and Freddie Mac in the event of another housing crisis but would also lower systemic risk.

How do CRTs differ from agency MBS?

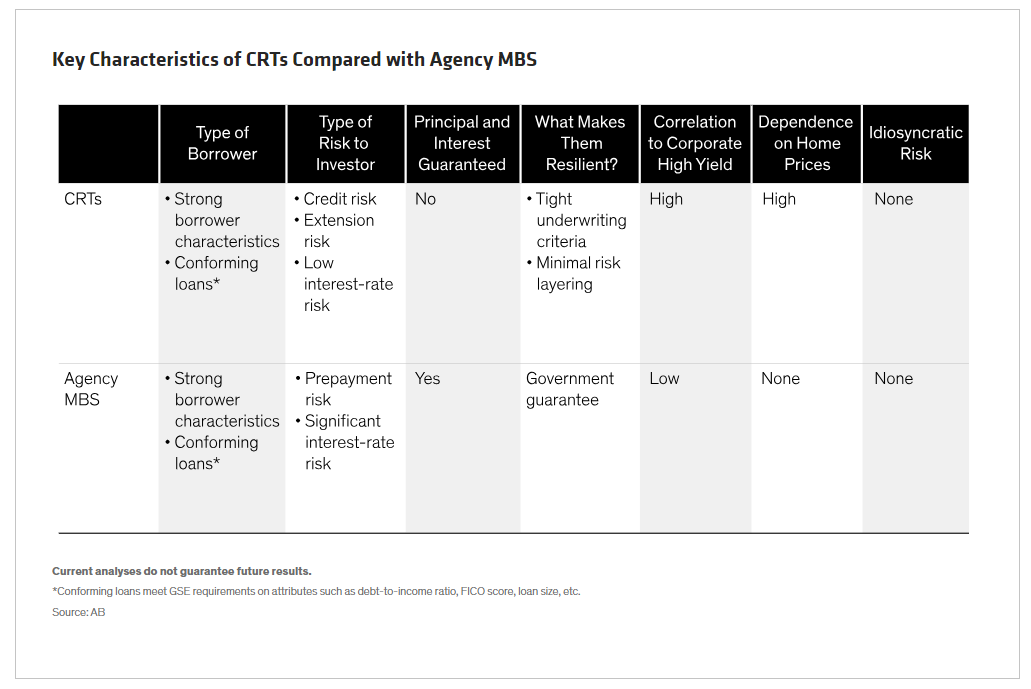

Both CRTs and agency MBS reference the same underlying pools of home loans that conform to the same strong credit standards. While the risk of the underlying mortgages is the same, the risk profiles of these two securities are very different. An investor who buys an agency MBS assumes all the interest-rate risk and prepayment risk of the underlying pool but none of its default risk. By contrast, an investor who buys a CRT takes on borrower default risk but not much interest-rate risk.

In fact, CRTs have floating rates tied to the Secured Overnight Financing Rate (SOFR), while most MBS have fixed rates. Floating-rate securities tend to perform well in an environment of rising interest rates. Other differences between CRTs and agency MBS are shown in the Display below.

How can CRTs be floating rate when the underlying mortgages are fixed rate?

Coupon payments on CRTs comprise SOFR, which is a floating rate, plus a spread.

During the securitization process for an MBS, the GSEs collect a guarantee fee that compensates them for the mortgage pool’s credit risk; these proceeds are used to pay the spread-over-SOFR portion of the CRT coupon.

The SOFR portion of the coupon is generated from the proceeds of the CRT issuance; these proceeds are placed in a trust and invested in a money-market fund.

How are CRTs structured?

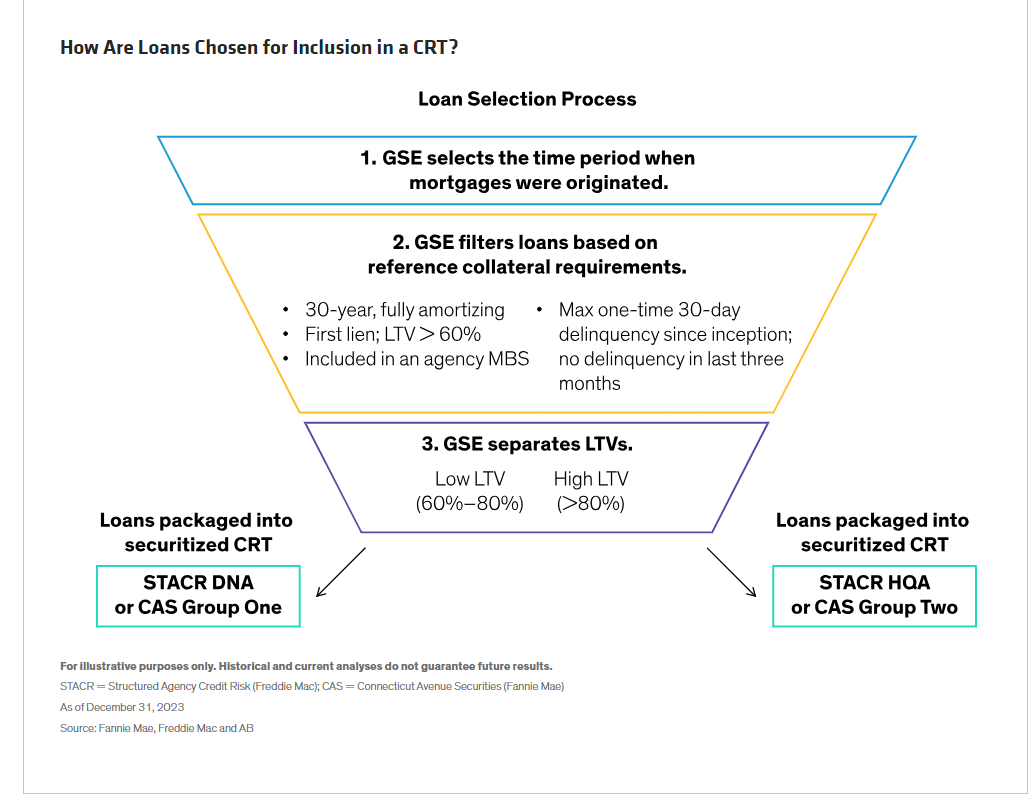

The process of creating a CRT begins with a series of filters.

Origination Date: First, the GSE filters all CRT-eligible mortgage loans by date of origination. For example, a CRT may include loans originated between April and September 2023.

Characteristics: Next, the GSE filters these loans according to the characteristics of the underlying collateral, such as the loan term (30-year mortgages only), loan-to-value (LTV) ratio or delinquency history.1

Segmentation by LTV Pool: The GSEs then divide loans into those with mortgage insurance (LTV above 80%) and those without (LTV below 80%).2

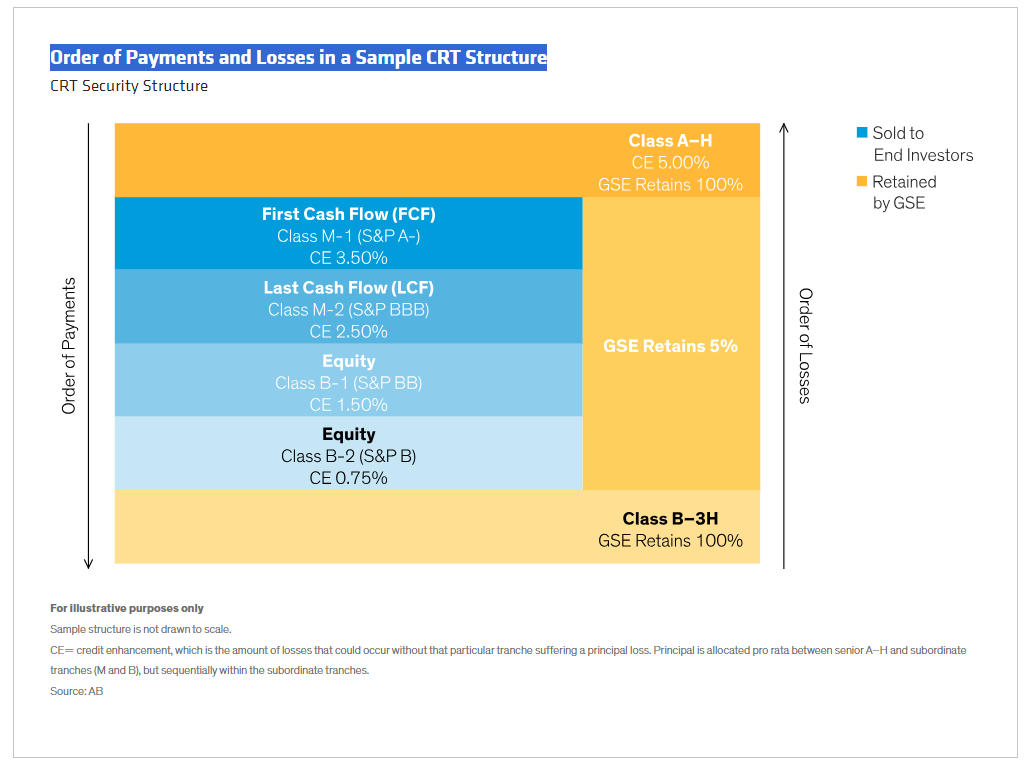

Risk Sharing: Lastly, the GSEs pass on a share of the credit risk to investors by issuing tranches. Only some of a CRT’s tranches are available to investors. The GSEs keep the entirety of the most senior tranche, which represents catastrophic risk that is not economical to sell. They also retain some of the subordinated risk to keep skin in the game and align their own interests with those of investors. While the structure of CRTs has changed over time, all CRT structures always retain a portion of the risk. The below Display describes the most recent structure.

Losses occur when a lender forecloses on a home and the sale proceeds don’t cover the mortgage balance.3 Lower-tiered tranches absorb losses first, followed by higher-rated tranches. A tranche begins to experience losses at its “attachment point” and cannot exceed losses beyond its “detachment point.”

For instance, if a tranche’s attachment point is 2.5%, as in the Last Cash Flow (LCF) tranche in the above graphic, then losses on the underlying pool will not affect the tranche until they surpass 2.5%. If its detachment point is 3.5%, the tranche experiences full principal loss when the pool’s losses reach 3.5%. Further losses on the pool cannot impact the tranche.

For prepayments, the direction of flows reverses. The most senior tranches receive prepayments first. Thus, in the display above, tranche A-H, which is held by the GSE, would receive 95% of prepayments on a pro rata basis (that is, proportional to the 95% of the capital structure retained by the GSE). The remaining 5% of prepayments would go to the subordinated tranches, where they cascade down (that is, not pro rata); the First Cash Flow (FCF) tranche would receive the remaining prepayments until it is paid off, with any prepayments not absorbed by the FCF tranche cascading down to the next tranche (LCF) until it is paid off, and so on. This structure usually creates an M1 bond that has a relatively short weighted average life of one to three years.

When a homeowner prepays their mortgage, CRT investors—especially those in the more subordinated tranches—tend to be happy, so long as their bonds are priced at or below par. After all, that’s one less borrower who might default. But when mortgage rates fall and homeowners refinance en masse, the payoff profile of the securities is affected, as their weighted average life may become shorter than expected. Further, if the tranches are prepaid, investors may find they need to reinvest at lower yields.

What could go wrong?

If the US were to experience a sudden and deep recession, a massive spike in unemployment and an influx of housing supply, that could precipitate a steep decline in home prices. (We do not currently expect any of these events.) Historically, high unemployment and deep recessions have led to high defaults on mortgages as homeowners were forced to sell.

However, today’s tight supply-and-demand technicals mean home prices are unlikely to fall, in our analysis. The government may also step in to prevent steep declines in home prices in the future.

How has the government prevented dramatic drops in home prices in the past?

In some instances, the government has taken measures to prevent home prices from spiraling down. For example, in 2020, when the US economy shut down due to the COVID-19 pandemic, policymakers enacted a forbearance program to assist homeowners—and they acted quickly, thanks to lessons learned from 2008. This program kept home prices from plunging. Borrowers who suffered economic hardship were able to pause their mortgage payments instead of defaulting on the mortgage or being forced to sell, which would have flooded the market with inventory.

What is your current outlook for CRTs?

We don’t see another housing crisis on the horizon. In fact, our outlook for CRTs today is good. There are two main considerations when assessing CRT fundamentals: the credit quality of the underlying pools of loans, and the outlook for the US housing market.

We expect home prices to rise modestly in 2024. With interest rates now relatively high, affordability has declined. But while rising mortgage rates have put a damper on demand, they’ve also contributed to a tight supply of single-family homes. The inventory of existing homes—which comprises 70% of all homes on the market—is extremely low. That’s because homeowners have locked in low interest rates from past years and don’t want to move. In turn, ongoing supply constraints provide support for home prices, even as demand moderates.

We expect housing demand to remain low due to affordability issues caused by higher rates and home prices. But, while renting has become more affordable than home ownership, the percentage of renters has been declining because of a general preference for owning, combined with fear of missing out on potential further home price appreciation.

Though mortgage rates are high, existing borrowers have locked in lower rates. Thus, all else being equal, their ability to service debt has remained unchanged even as mortgage rates have risen. (Of course, this could change if economic conditions were to deteriorate and homeowners were to lose jobs. However, given the massive appreciation in home prices in recent years, most homeowners would be more incentivized to sell their homes than to default on their mortgages.)

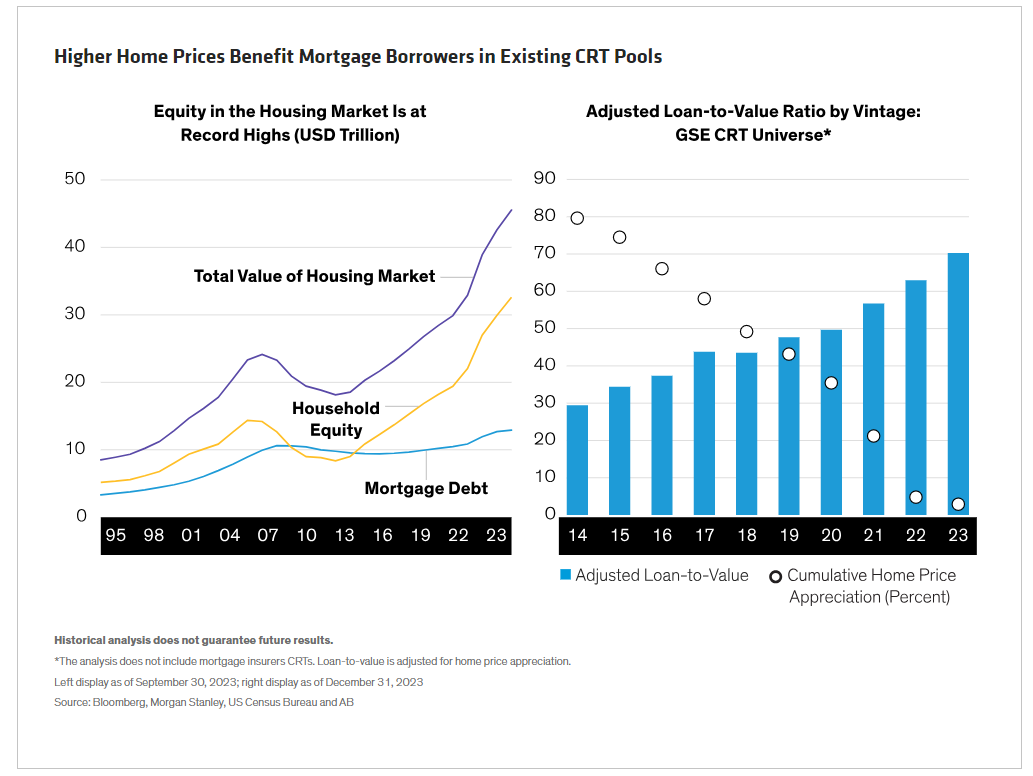

As to the credit quality of the CRTs, fundamentals appear to us to be very strong. The ratings agencies seem to agree; every bond issued before 2021 that was originally rated has received a rating upgrade.

Home price appreciation has also led to the natural deleveraging of CRT bonds. More seasoned bonds have especially strong LTV metrics. What’s more, as older-vintage CRTs have de-levered, the GSEs have been making tender offers to buy the bonds back from investors. After all, the GSEs issued these bonds to hedge their credit risk, so there’s no reason to keep them on the market once that risk is no longer there. As a result, investors today can potentially own CRTs with very little credit risk but with attractive spreads; they may also benefit from GSE tender offers, which, alongside limited issuance, have helped push CRT prices up.

Meanwhile, the mortgage loans underlying CRTs are particularly high quality: most of these borrowers have FICO scores above 750. And underwriting standards—already high after the 2008 crisis—tightened even more during the pandemic. As a result, more recently issued CRTs have exceptionally strong fundamentals, in our view. Further, as the Fed hiked, CRTs’ coupons reset higher.

That’s good news for CRT investors, who, in our analysis, may continue to benefit from favorable winds in the months ahead.

1. GSEs may retain loan credit risk for six to 12 months before passing it on to an investor. During this time, some borrowers may miss payments. Such mortgage loans are not included in CRT securities, even if they turn current.

2. A borrower who doesn’t have enough money for a 20% down payment can substitute a mortgage insurance policy.

3. Net of delinquent interest, expenses and principal forgiveness

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All