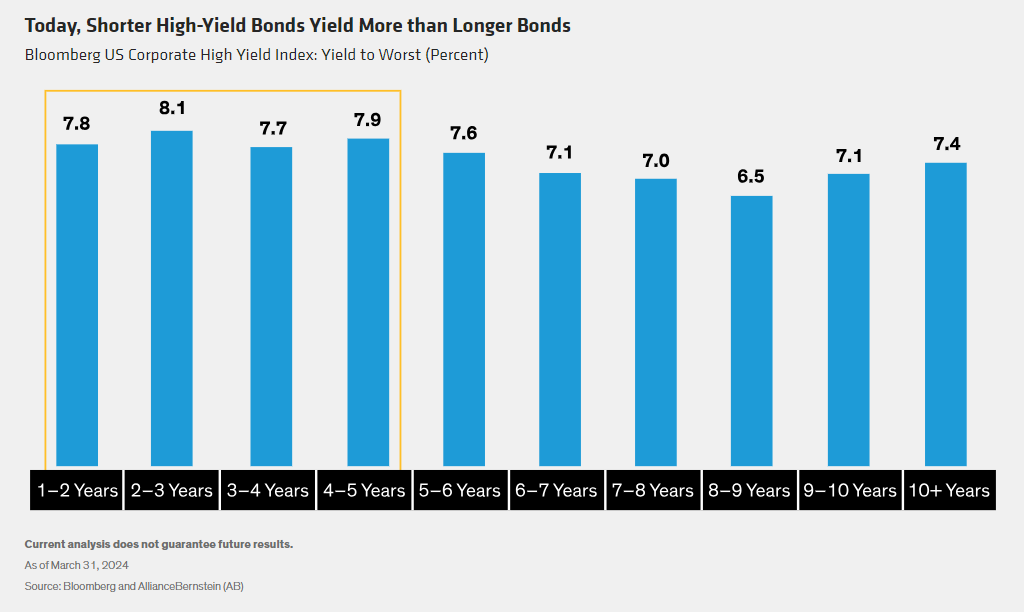

It makes sense that longer-maturity bonds typically provide higher yields than shorter-term bonds. After all, more bad things can happen in a longer period than a shorter one, and visibility is poorer for the next 10 years than for tomorrow. Investors expect to be paid for these risks.

But in an unusual—and prolonged—aberration, short-term high-yield debt is currently yielding more than longer-term debt, especially in the US (Display). An inverted high-yield curve is great news for high-yield bond investors who are concerned about near-term market volatility.

Even in normal times, a shorter-duration high-yield strategy can provide high levels of income with lower volatility than an intermediate-duration strategy. Historically, a shorter high-yield approach has provided nearly the same average annualized return as a longer-maturity mandate, with about two-thirds of the volatility.

But with the high-yield curve inverted, as it is today, investors are being paid more to take less risk. We think that’s an income opportunity worth sizing up.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.