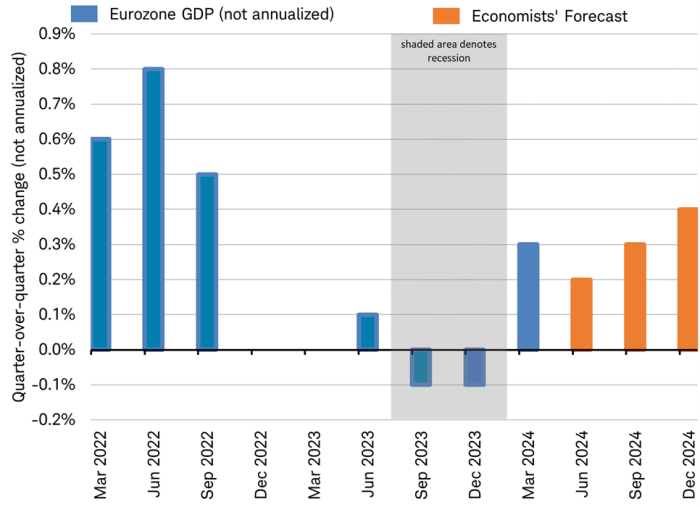

Last week's data revealed that Europe's mild recession ended with the first quarter of 2024. Two back-to-back gross domestic product (GDP) declines of -0.1% in the third and fourth quarters of 2023 were followed by growth of +0.3% in the first quarter. This growth for the quarter 1.3% on an annualized basis, approaching the U.S.'s annualized 1.6% growth in the first quarter of this year. After five quarters of economic stagnation following Russia's invasion of Ukraine and the European Central Bank's (ECB) acceleration of the monetary tightening due to the related surge in energy prices, Europe's economic growth is expected to continue over the coming quarters, according to the consensus of 50 economists tracked by Bloomberg. That consensus is in line with our forecast for a U-shaped recovery for the global economy detailed in our 2024 Global Outlook.

Europe's recession ended in 2023

Source: Charles Schwab, Bloomberg data as of 5/1/2024.

Bloomberg-tracked consensus economists' forecast. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

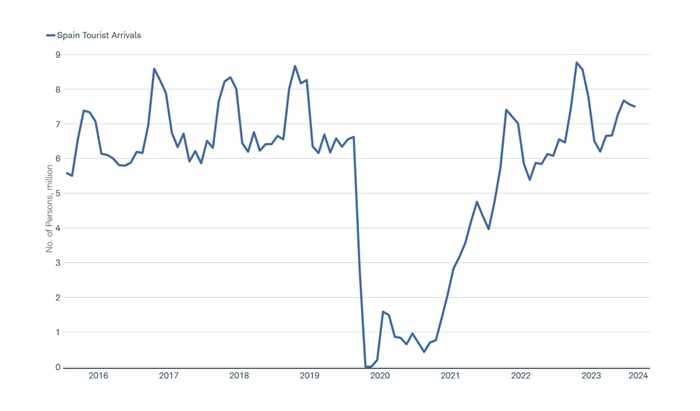

Over most of the past 15 years, it has been Europe's larger, northern countries that drove Europe's growth. But in the first quarter, Spain and Portugal were among the fastest-growing eurozone economies at +0.7%, while France and Germany were among the laggards, growing by +0.2%. One driver may have been the weaker euro relative to the U.S. dollar benefiting tourism, which accounts for around 10% of the economies of Spain, Italy, Greece, and Portugal. Southern Europe has seen international tourist arrivals return to pre-pandemic levels.

Tourism has returned to pre-pandemic levels

Source: Charles Schwab, Spanish National Statistics Institute, Macrobond data as of 5/1/2024.

Europe's momentum appears to be both improving and broadening since the end of the first quarter. In April, the Eurozone Composite Purchasing Managers' Index (PMI) rose above the 50 level that separates expansion from contraction for the second month in a row. The index initially fell below 50 in July 2023. Germany is the largest economy and has been the economic laggard in the region. However, in April, the Composite PMI for Germany moved into expansion for the first time in 10 months. Two components of the PMI saw particular improvement: employment expanded across the region and business confidence was the second highest in 14 months in April. We saw confirmation in German Ifo Business Climate Survey which moved higher in the last two months; the outlook for the next 12 months is anticipated to reach the highest level in a year. German industrial production also rose in February and March.

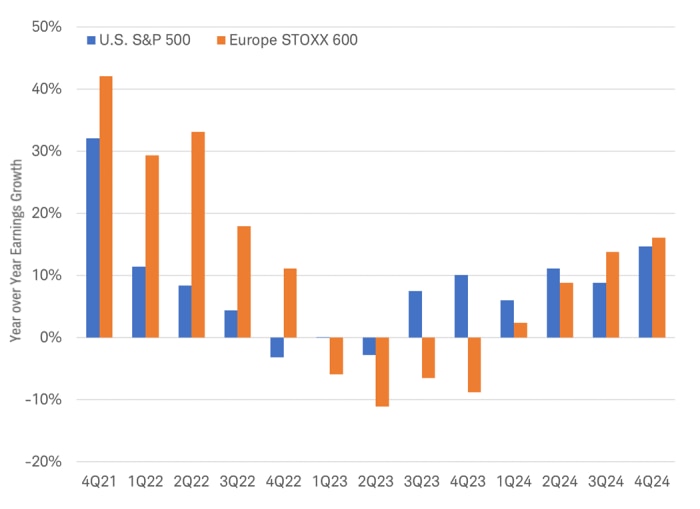

More important to investors, the economic recovery is accompanied by an outlook for corporate earnings growth set to rebound from last year's declines to double-digit growth by the fourth quarter. Earnings for European companies are expected by analysts to rebound and outgrow U.S. earnings by the third quarter.

Rebounding earnings growth

Source: Charles Schwab, LSEG I/B/E/S data as of 5/1/2024.

2Q – 4Q of 2024 are earnings growth estimates based on analysts' expectations. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

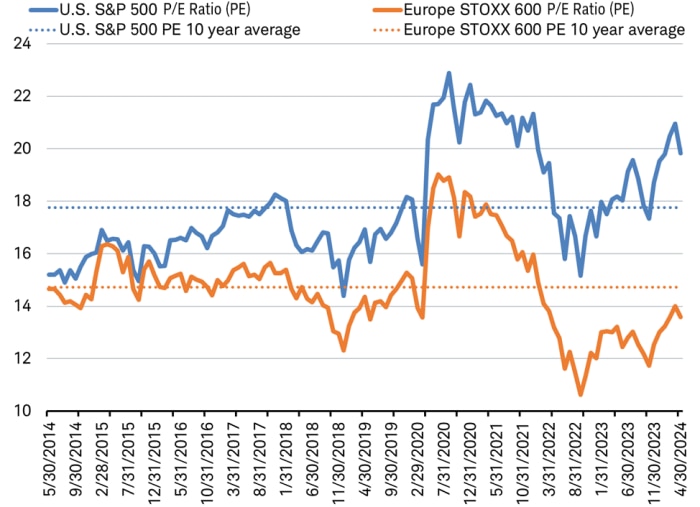

The brightening outlook of a recovery in economic and earnings growth combined with an outlook for interest rate cuts by the European Central Bank expected to begin in June have lifted the price-to-earnings ratio for the Europe STOXX 600 Index by 15%, from 11.8 to 13.6, since the start of November. Yet, European stocks remain attractively valued. International stocks still sell at a discount to their 10-year average valuation based on the forward price-to-earnings ratio, while U.S. stocks sell at a premium to their 10-year average. This indicates a potential for European stock market valuations to expand further as the recovery unfolds.

Price-to-earnings ratio still below average for Europe

Source: Charles Schwab, FactSet data as of 5/1/2024.

Past performance is no guarantee of future results.

Europe's stock market continues to outperform the S&P 500 since the current bull market began in October 2022. The gap did narrow during Europe's recession, but has since widened back out again, as you can see in the chart below. The total return of the MSCI EMU Index is outperforming the S&P 500 by about 20 percentage points, measured in U.S. dollars.

Europe's outperformance

Source: Charles Schwab, Macrobond data as of 4/30/2024.

. Performance begins on 10/12/2002, at the start of the current bull market. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

The shallow recession in the eurozone appears to be shifting to a modest recovery, with one positive GDP quarter now in the rear view. The gap in relative earnings growth between Europe and the U.S. may shift in favor of European stocks. Despite the climb in valuations already seen, valuations for eurozone stocks remain below the longer-term average and remain attractively valued, offering the potential for further price appreciation.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab