Sour sentiment toward emerging-market stocks is obscuring uncommon opportunities for equity investors.

Emerging-market (EM) equities are still struggling. But weak investor sentiment may be creating a favorable backdrop for stock pickers. With the right mindset, investors can discover promising EM businesses that aren’t tethered to the fortunes of developing-world economies or markets.

There’s no shortage of unsettling EM news these days. China is coping with lackluster economic growth. Recent elections in India, South Africa, Mexico and Argentina could lead to policy changes. Geopolitical risk is elevated as war rages from Ukraine to the Middle East. It’s a lot of uncertainty to stomach.

But it’s a very different story for many EM companies. While their stocks might get tarred by the same EM brush, plenty of developing-world businesses have bright prospects, have solid earnings growth and don’t rely on the Chinese economy. Some familiar storylines can help lead investors to opportunities in stocks with pent-up return potential.

Extreme Makeovers: Companies That Are Reinventing Themselves

Everybody loves a good turnaround story. Yet sometimes, the long shadow of a controversy or crisis can obscure positive change.

Consider Tencent Music Entertainment. The Chinese music-streaming service has faced a litany of challenges since its initial public offering in 2019. At the time, its main business was social entertainment services. Tighter regulation and tougher competition led to a decline of paying users—and a sharp drop in its shares through most of 2022.

Instead of buckling, Tencent Music reinvented itself as a music powerhouse. The company now dominates music streaming in China, and offers innovative services such as social karaoke, personal song recordings and singing competitions with friends. Today, this music business generates most of the company’s revenue in a growing industry that really isn’t vulnerable to China’s macroeconomic troubles.

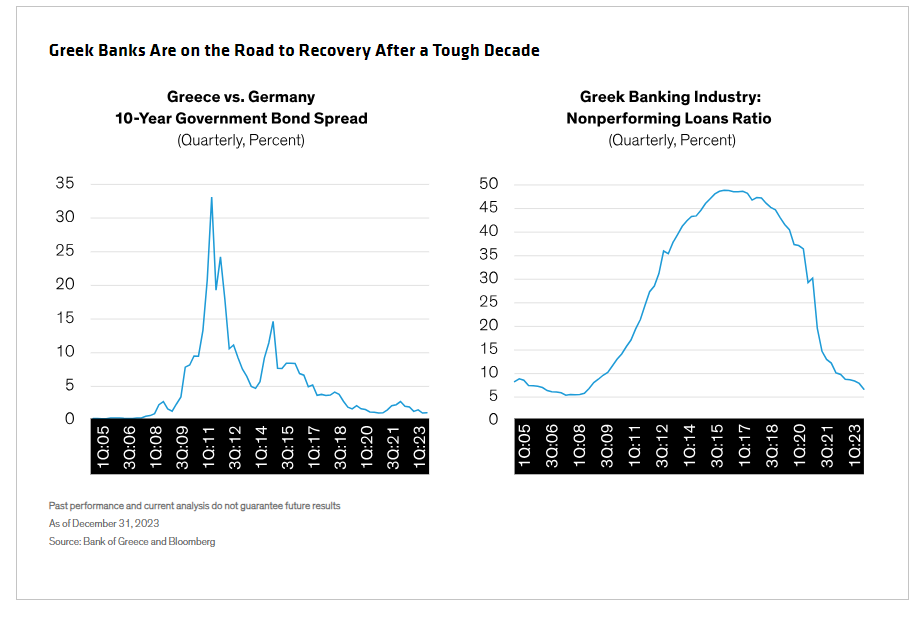

In a very different makeover story, Greece’s banking sector is rebuilding its reputation, long tainted by the country’s sovereign-debt crisis over a decade ago. Since MSCI downgraded Greece from a developed market to an emerging market in 2013, the country’s 0.5% weight in the MSCI Emerging Markets Index kept it off many investors’ radars. A tepid economy hasn’t helped.

Now, the International Monetary Fund projects that Greek GDP will grow by about 2.0% in 2024 and 2025. Greece’s current account deficit and unemployment rate are getting healthier. Narrowing credit spreads reflect improvements (Display). Meanwhile, nonperforming loan ratios of Greek lenders have dropped from nearly 50% in 2015 to under 10% in 2023. As the environment stabilizes, select Greek banks with strong capital ratios and business models look poised to recover.

Never Heard of These Companies?

Many of the MSCI EM’s 1,330 constituents aren’t household names for international investors. Dig a bit deeper—or look beyond the benchmark names—and you can find solid businesses that get little fanfare.

Kazakhstan is off the beaten track for EM equity investors. The country is home to Kaspi.kz, a local leader in payments, fintech and e-commerce, with a firm position for future growth. Kaspi.kz effectively runs about two-thirds of the country’s payment infrastructure, processing 74% of total payment transactions, which is four times the level of Visa and Mastercard transactions in Kazakhstan combined, according to company reports and data from the country’s central bank.

China is more familiar territory, yet some companies are relatively unknown. Nongfu Spring, a soft-drink manufacturer, has been in business for nearly three decades but only went public in late 2020, so it’s a newcomer to equity investors. In a country where tap water isn’t potable, the company’s clever marketing campaigns have helped it grab more than 20% of the bottled water market despite being a late entrant. Nongfu is now an early mover in the bottled unsweetened tea market, commanding more than half the market share of a segment that has grown by 30% a year from 2017 to 2023, according to a report by Iyiou Research.

Beneficiaries and Enablers of Structural Change

Big change means big business for EM companies, whether driven by government reforms or global disruption.

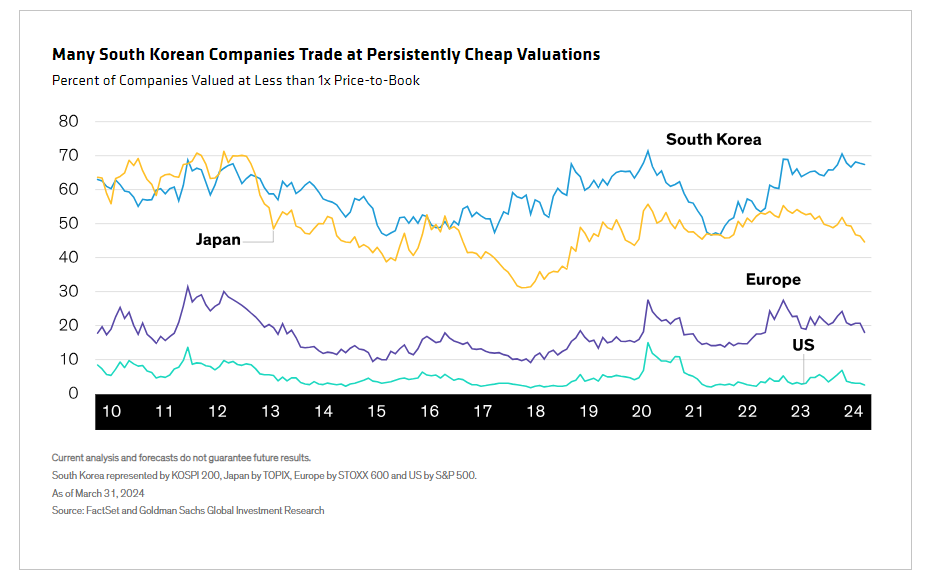

In South Korea, the government’s “Corporate Value-up” program aims to emulate Japan’s success at improving capital management by listed companies. The program includes guidelines aimed at enhancing shareholder disclosure, increasing shareholder returns through dividends, encouraging share buybacks and improving operating valuations.

The goal is to boost valuations in a market dominated by family-owned conglomerates (chaebols), including Samsung, Hyundai and LG. Chaebols control 62% of companies in the MSCI South Korea Index, and help explain why Korean companies rank low on MSCI’s governance scores—and trade at persistently cheap valuations (Display). The reforms will take time, but we see real potential for active investors to identify early reformers en route to unlocking shareholder value.

In Latin America, a transition to e-commerce and financial inclusion is in full swing. MercadoLibre, a regional e-commerce company, is at the heart of these changes. The company’s e-commerce platform runs on a third-party merchant model, so it carries no inventory, and offers a broad logistics network to facilitate deliveries, which can be unreliable in the region. MercadoLibre has also developed its own payment solutions and fintech services—adding a competitive advantage on a continent that still has a huge unbanked population.

Global enthusiasm for artificial intelligence (AI) has not passed over EM countries. In fact, many EM companies manufacture vital components for AI and should benefit as the technology spreads. Since they are less visible than the US technology titans, investors can often capture AI growth potential in EM companies at much better valuations.

Tying the Threads Together

These disparate stories share common threads. First, many EM companies don’t depend on macroeconomic growth to succeed because their business models are either global or driven by local structural changes. Second, shares of these companies often trade at relatively attractive valuations versus non-EM peers. Third, EM companies with high-quality business models have the fortitude to overcome regional or market pressures.

Investors who can tie these threads together with a disciplined stock-picking process will find uncommon opportunities in diverse EM industries and countries. It will take patience, but we think positioning in select companies today should pay off over time when business fundamentals are rewarded, with an added potential bonus for investors when EM stocks find their footing again.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

References to specific securities discussed are not to be considered recommendations by AllianceBernstein L.P.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© AllianceBernstein

Read more commentaries by AllianceBernstein