It seems that France's stock market has been hit by the uncertainty generated by President Macron's unexpected call for an election, with the second round occurring next weekend. Meanwhile U.S. stocks have continued to climb. But is this the whole story? What best explains the relative performance of the U.S. versus other stock markets over time? Politics? Economic growth? Inflation? Currency? All of these can matter, but history shows the main factor influencing performance is sector exposure.

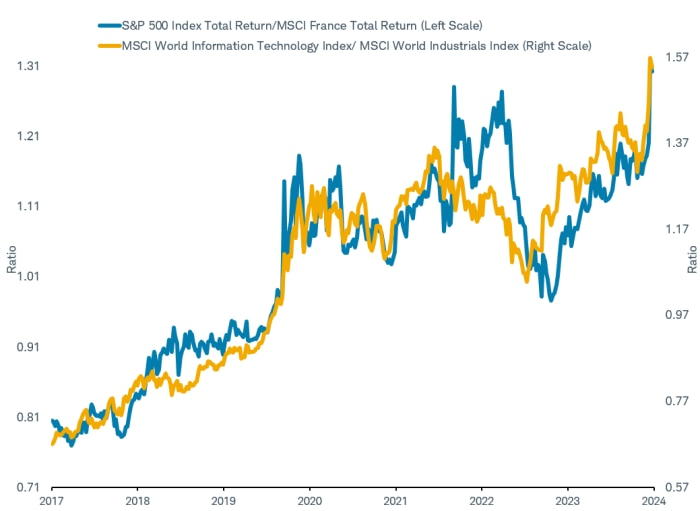

The relative performance of the U.S. stock market versus France's can largely be explained by the difference between the performance of the global Information Technology (Tech) sector and the global Industrial sector. The chart below shows the performance of the U.S. stock market versus the French stock market in blue over the past decade (the S&P 500 index divided by the MSCI France index), and the performance of the Tech sector versus the Industrials sector in orange (the MSCI World Technology index divided by the MSCI World Industrials index). The French stock market is dominated by Industrials, composing 26% of the MSCI France index, compared with 8% exposure for the United States. The U.S.'s S&P 500 has 33% exposure in the Tech sector while France has just 4%. To clarify, French stocks do not dominate the MSCI World Industrials index. In fact, U.S. stocks have the highest weighting in both of these indexes—which is unsurprising since U.S. stocks make up greater than 50% of the parent MSCI World Index.

U.S. vs. France = Tech vs. Industrials

Source: Charles Schwab, Bloomberg data as of 6/22/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

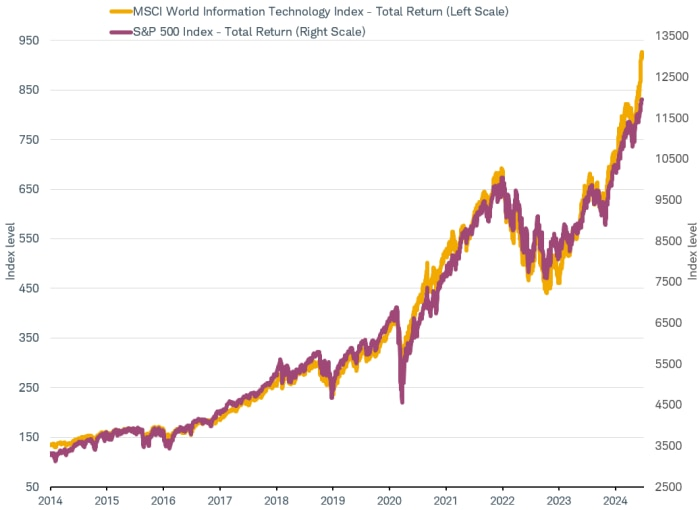

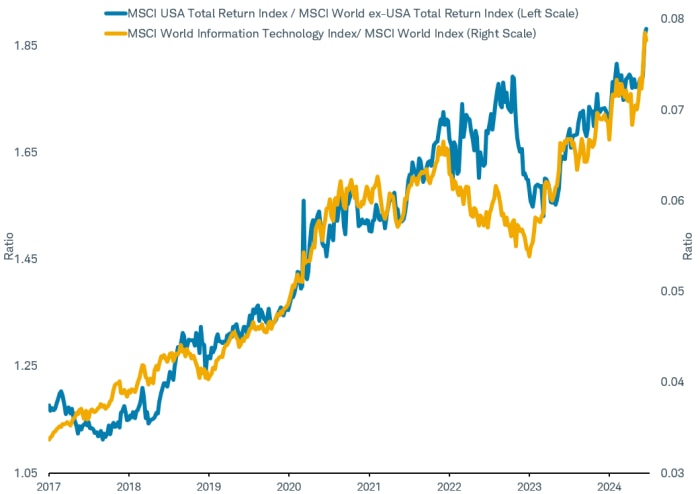

The point is that despite politics and other macro factors, it is sector performance that is likely the primary driver of markets' relative performance. The U.S. stock market (S&P 500) has tended to perform in line with the Tech sector (MSCI World Technology Index), as you can see in the chart below. Measured statistically, the correlation between their performance is a very high 0.92 on both a monthly and weekly basis over the past 10 years and on a daily basis over the past two years. That isn't a perfect relationship, but a very strong one.

S&P 500 and World Tech sector

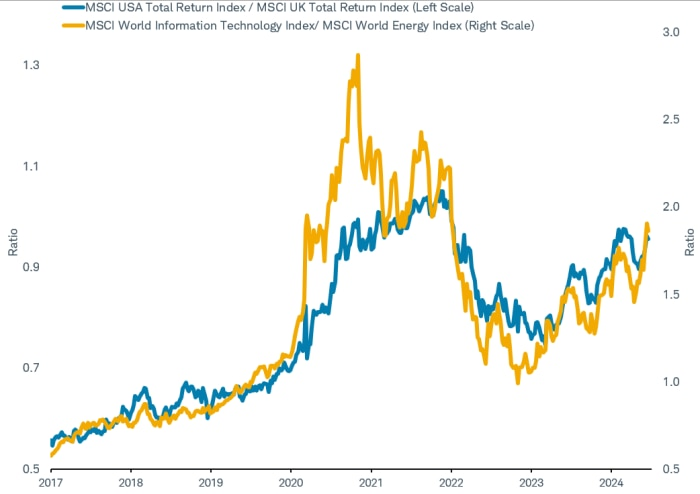

If the U.S. behaves like the world's Tech sector and France like the Industrials sector, what sectors align with the performance of other countries' stock markets? Australia tends to behave like Materials, Canada like Financials, and the United Kingdom like the Energy Sector.

United Kingdom

The U.K. is a big producer of Brent crude oil, the global energy benchmark grade produced in the North Sea. The U.K. stock market is highly exposed to the Energy sector with just two oil companies, BP and Shell, accounting for nearly 50% of the earnings of the MSCI United Kingdom Index as of the first quarter of this year. The Energy sector currently makes up 13% of the U.K. stock market compared to just 4% in the U.S.'s S&P 500. Therefore, it may be no surprise that the total return of the U.S. relative to the U.K.'s stock market closely tracks the relative performance of the world's Tech and Energy sectors.

Source: Charles Schwab, Bloomberg data as of 6/22/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

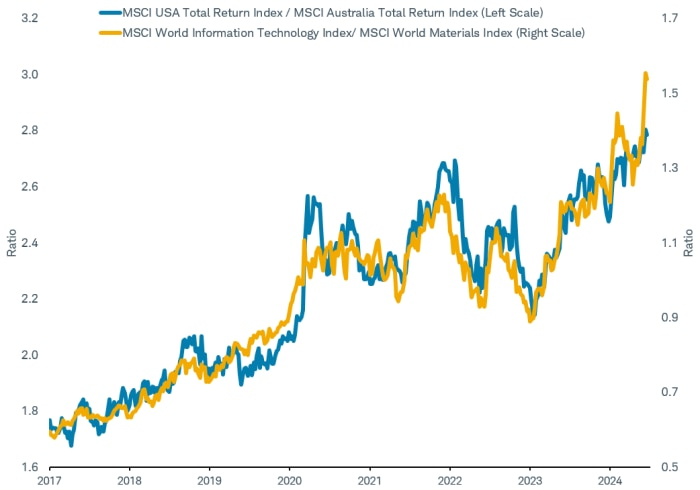

Australia

Iron ore is Australia's top export; BHP, the world's largest metal producer, is headquartered there. Materials stocks make up 21% of the MSCI Australia Index compared to only 2% in the U.S.'s S&P 500. It logically follows that the relative performance of the U.S. and Australian stock markets tracks the relative performance of the world's Tech and Materials sectors, as you can see in the chart below.

U.S. vs. Australia = Tech vs. Materials

Source: Charles Schwab, Bloomberg data as of 6/22/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Canada

Canada's biggest stock market sector is Financials at 35% of the index, including big names like TD Bank and Royal Bank of Canada. This compares to 12% exposure in the U.S. stock market. The relative performance of the U.S. and Canadian stock markets tracks the relative performance of the world's Tech and Financial sectors, as you can see in the chart below.

U.S. vs. Canada = Tech vs. Financials

Source: Charles Schwab, Bloomberg data as of 6/20/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

U.S.

It may be worth reviewing how much Tech-like exposure investors may have in their portfolios if they are concentrated in the U.S., rather than being more globally diversified.

At Charles Schwab, the sectors we favor in the second half of this year are: Financials, Energy, and Materials, as you can find in our monthly Sector Views publication. This suggests we see the potential for outperformance by the U.K., Australia, and Canada in the months ahead.

But rather than concentrate in a few other countries that also behave just like one sector, broad diversification may be preferable. As you can see in the chart below, the performance of the U.S. relative to the rest of the world is similar to the performance of the Tech sector versus all other sectors. While there was some deviation in the relationship during 2022's bear market, when the U.S. performed relatively well, even as the Tech sector lagged, the divergence was temporary.

U.S. vs. Rest of World = Tech vs. Everything Else

Source: Charles Schwab, Bloomberg data as of 6/22/2024.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Over the past 10 years, the U.S. has had different political parties in office, different rates of economic growth and inflation, Federal Reserve rate cuts and hikes, yet the relative outperformance by U.S. stocks appears to have been primarily the result of Tech exposure. The U.S. will likely remain connected with Tech in the future as it has historically, but Tech stocks don't always lead the stock market. For example, Tech was the best-performing sector in the 1990s, then it was the worst for the 2000s. Investors may want to consider some diversification away from a heavy concentration in Tech should the outperformance over the past decade not persist.

Michelle Gibley, CFA,® Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Currency trading is speculative, volatile and not suitable for all investors.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated.

The MSCI World Energy Index is designed to capture the large and mid cap segments across 23 Developed Market countries. All securities in the index are classified in the Energy sector as per the Global Industry Classification Standard (GICS®).

The MSCI World Financials Index is designed to capture the large and mid cap segments across 23 Developed Market countries. All securities in the index are classified in the Financials sector as per the Global Industry Classification Standard (GICS®).

The MSCI World Information Technology Index is designed to capture the large and mid cap segments across 23 Developed Market countries. All securities in the index are classified in the Information Technology sector as per the Global Industry Classification Standard (GICS®).

The MSCI World Industrials Index is designed to capture the large and mid cap segments across 23 Developed Market countries. All securities in the index are classified in the Industrials sector as per the Global Industry Classification Standard (GICS®).

The MSCI World Materials Index is designed to capture the large and mid cap segments across 23 Developed Market countries. All securities in the index are classified in the Materials sector as per the Global Industry Classification Standard (GICS®).

The MSCI Australia Index captures the performance of the large and mid-cap segments of the Australia market and represents approximately 85% of the free float-adjusted market capitalization in Australia.

The MSCI Canada Index captures the performance of the large and mid-cap segments of the Canada market and represents approximately 85% of the free float-adjusted market capitalization in Canada.

The MSCI France Index captures the performance of the large and mid-cap segments of the France market and represents approximately 85% of the free float-adjusted market capitalization in France.

The MSCI United Kingdom Index captures the performance of the large and mid-cap segments of the UK market and represents approximately 85% of the free float-adjusted market capitalization in the UK.

The MSCI USA Index is designed to capture the large and mid cap segments of the US market.

The MSCI World Index is designed to capture the large and mid cap segments across 23 Developed Market countries.

The MSCI World ex-U.S. Index is designed to capture the large and mid cap segments across 23 Developed Market countries, excluding the U.S.

0724-ATPC

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab