Volatility has recently ticked higher as central bank policies start to diverge and as market participants try to divine the timing and magnitude of central bank rate cuts. An unusually large number of investors remain sidelined, not yet ready to return to the market. But big-picture economic trends remain encouraging, and yields remain high—for now. We see these as favorable conditions for bond investors—especially for those who can beat the eventual rush back into bonds.

Central Banks Step Out of Sync

So far in 2024, among developed markets, the Swiss National Bank, the Bank of Canada and the European Central Bank have cut rates. The Bank of England has signaled it will begin cutting in August. And the Fed has delayed its initial rate cut until late this year. Meanwhile, the Bank of Japan (BOJ) is heading in the opposite direction. It abolished its eight-year-old negative interest-rate policy in March, hiking rates for the first time in 17 years, and has begun to shrink its balance sheet through passive quantitative tightening.

Recent divergence in central bank policy has brought volatility back into the market, as has geopolitical uncertainty, with election results in Mexico, India and Europe driving a significant repricing of assets in those regions. We believe volatility could remain elevated over the next few months. Economic data will likely become increasingly important in determining the Fed’s timing of cuts, and even small deviations from expectations could cause swings in valuations. Geopolitical uncertainties could also drive further fluctuations.

In our view, investors should get comfortable with evolving policy expectations and data surprises and avoid getting swept up in short-term turbulence. Broader trends, such as moderate global economic growth and high yields, matter more. Government bond yields remain very compelling, with AAA-rated 10-year German Bunds currently yielding 2.5% and the US 10-year Treasury yielding 4.3%.

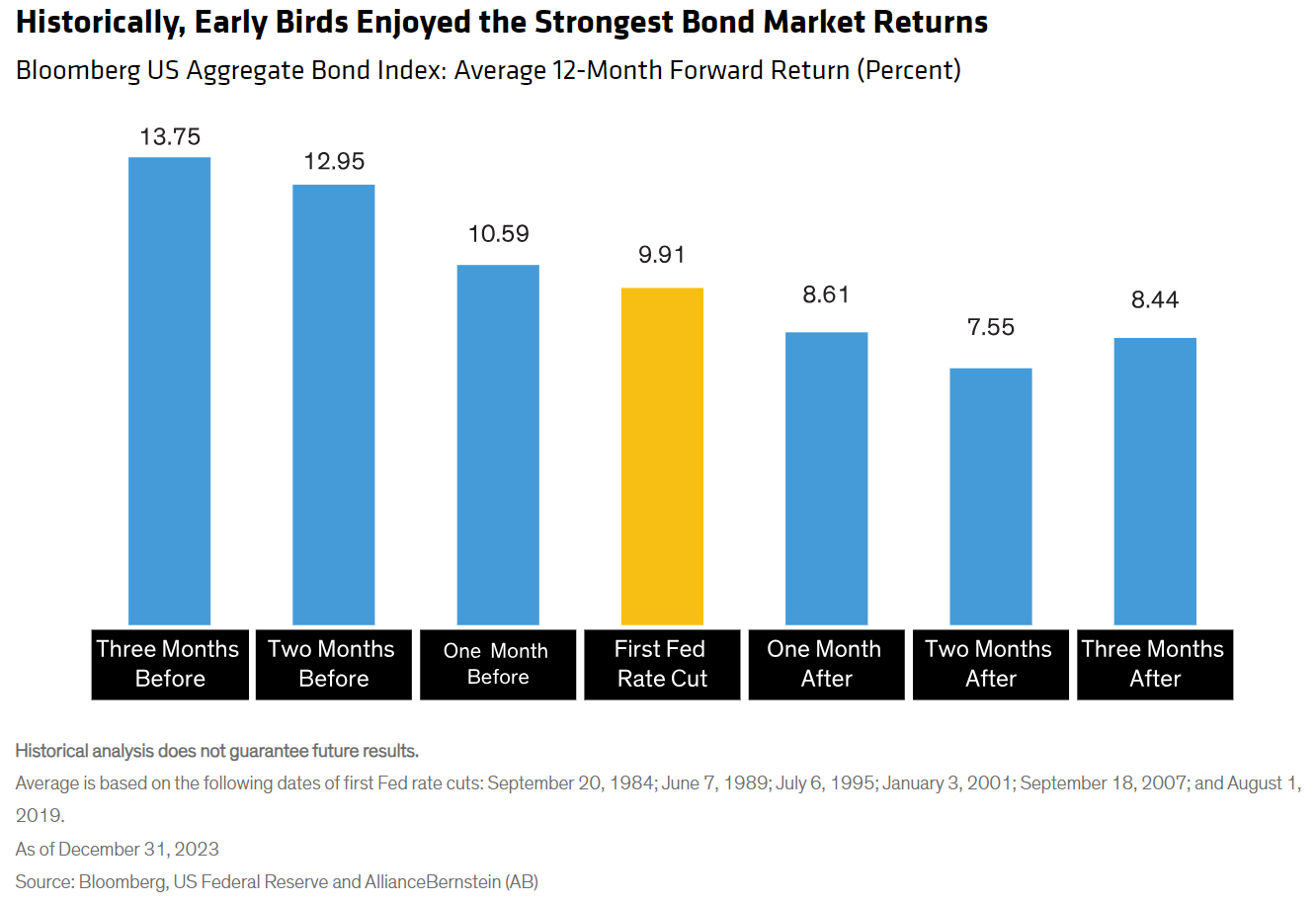

Anticipate the Action

For bond investors, these conditions are nearly ideal. After all, most of a bond’s return over time comes from its yield. And falling yields—which we expect across most of the developed world in the second half of 2024—boost bond prices. That boost could be especially big given how much money remains on the sidelines, looking for an entry point. A record $6.5 trillion is sitting in US money-market funds, a relic of the “T-bill and chill” strategy made popular in 2023, when central banks were aggressively hiking interest rates.

Historically, as central banks ease, cash floods out of money markets and back into longer-term debt. The resulting surge in demand for bonds from such flows helps reinforce the drop in yields that accompanies central bank rate cuts. Because the amount of cash sitting on the sidelines today is unprecedented, the potential surge in demand for bonds is exceptionally high. We anticipate roughly $2.5 to $3 trillion will return to the bond market over the next couple of years.

To avoid missing out on the potential returns this represents, we think investors should aim to get ahead of the shift from cash to bonds. That means making the switch before the US Federal Reserve starts to cut, because government bond yields often fall—and prices rise—before the central bank takes action. Historically, in the three months prior to the first Fed rate cut, the yield on the 10-year US Treasury fell an average of 90 basis points. Indeed, past investors captured the biggest returns when they invested several months prior to the start of the easing cycle (Display).

Position for Today’s Environment

In our view, bond investors can thrive in today’s favorable environment by applying these strategies:

Get invested. If you’re still parked in cash, you’re losing out on the daily income accrual provided by higher-yielding bonds, as well as the potential price gains as yields decline. While cash rates are currently higher than much of the yield curve, that’s typical ahead of easing cycles—and in the runup to large capital-gain opportunities. That’s why it’s so important that bond investors get off the sidelines and get invested now. In fact, in today’s environment, investors should probably allocate more to fixed income than they have historically.

Extend duration. If your portfolio’s duration, or sensitivity to interest rates, has veered toward the short end, consider lengthening it. As the economy slows and interest rates decline, duration benefits portfolios. Government bonds, the purest source of duration, also provide ample liquidity and help to offset equity market volatility.

Think global. Not only do idiosyncratic opportunities increase globally as central banks forge their own paths, but the advantage provided by diversification across different interest-rate and business cycles is also more powerful when central banks are out of sync.

Hold credit. We don’t think this is the time to avoid or underweight credit. Though spreads are on the tighter side, yields across credit-sensitive assets such as corporate bonds and securitized debt are higher than they’ve been in years, and over time a bond derives most of its return from yield. In fact, corporate fundamentals are still in relatively good shape, having started from a position of historic strength. And falling rates later in the year should help relieve refinancing pressure on corporate issuers. Further, as money moves out of cash, we anticipate robust demand for credit, especially investment-grade debt; this positive technical should help support credit spreads. That said, investors should be selective and pay attention to liquidity. CCC-rated corporates and lower-rated securitized debt are most vulnerable in an economic slowdown.

Adopt a balanced stance. We believe that both government bonds and credit sectors have a role to play in portfolios today. Among the most effective strategies are those that pair government bonds and other interest-rate-sensitive assets with growth-oriented credit assets in a single, dynamically managed portfolio. This pairing also helps mitigate risks outside our base-case scenario of weaker growth—such as the return of extreme inflation, or an economic collapse.

Protect against inflation. Given the heightened risk of future surges in inflation, the corrosive effect of inflation, and the affordability of explicit inflation protection, we think investors should consider increasing their allocations to inflation strategies now.

Consider a systematic approach. Today’s environment also increases potential alpha from security selection. Active systematic fixed-income approaches can help investors harvest these opportunities. Systematic approaches rely on a range of predictive factors, such as momentum, that are not efficiently captured through traditional investing. Because systematic approaches depend on different performance drivers, their returns may complement traditional active strategies.

The Tide Has Turned in Investors’ Favor

Active investors should prepare to take advantage of opportunities created by heightened volatility and market tailwinds in the second half of the year. In our view, the most critical step is simply to get back into the bond markets so as not to miss out on today’s high yields and exceptional potential return.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein