Economic indicators are released every week to provide insight into the overall health and performance of an economy. They serve as essential tools for policymakers, advisors, investors, and businesses because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending on June 3, the SPDR S&P 500 ETF Trust (SPY) rose 1.09% while the Invesco S&P 500® Equal Weight ETF (RSP) was down 0.13%.

Some of the most closely watched economic indicators are those surrounding the labor market. They provide insight into the health of the economy. But they also impact individuals’ lives and play a central role in government policy decisions. Last week featured a handful of employment updates that provided insights into different aspects of the U.S. labor market. This article will discuss the key data points from each report and explore their potential implications.

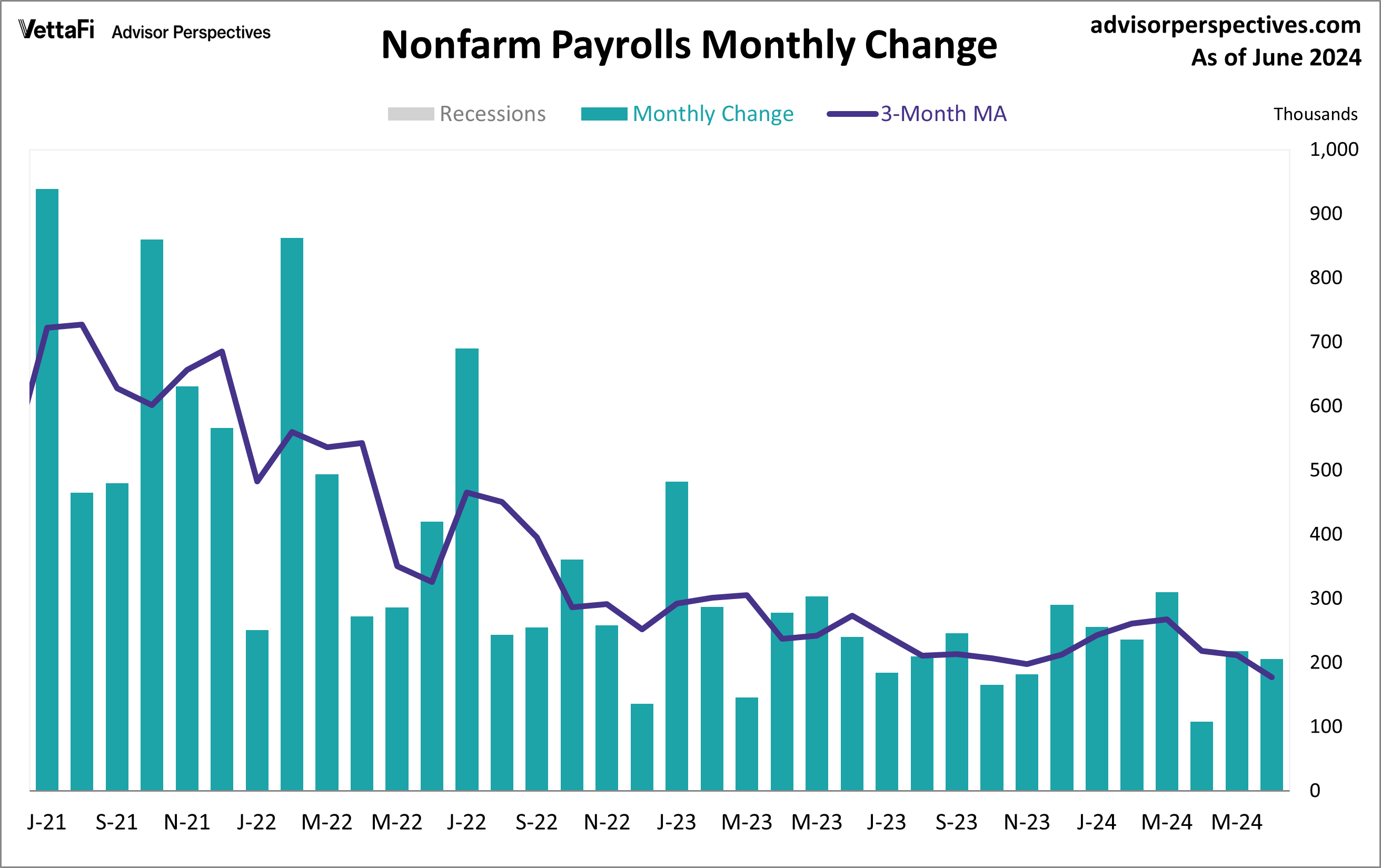

Employment Report

The U.S. labor market added more jobs than expected last month, but still showed signs of cooling down. The June employment report revealed 206,000 jobs were added last month, exceeding the expected 191,000 addition. With that said, June’s jobs numbers were a slowdown from May’s downwardly revised 218,000 addition.

The report also revealed another increase in the unemployment rate to 4.1%, its highest level since November 2021. Additionally, hourly earnings increased 0.3% from the previous month and 3.9% from one year ago. Both readings marked a slowdown from May and were consistent with their respective forecasts.

Overall, the latest jobs report strengthens views that the Fed will begin to cut rates later this year. Despite last month’s Fed forecast of only one rate cut this year, the CME FedWatch Tool is currently projecting two; the first one at the September meeting and the second one at the December meeting.

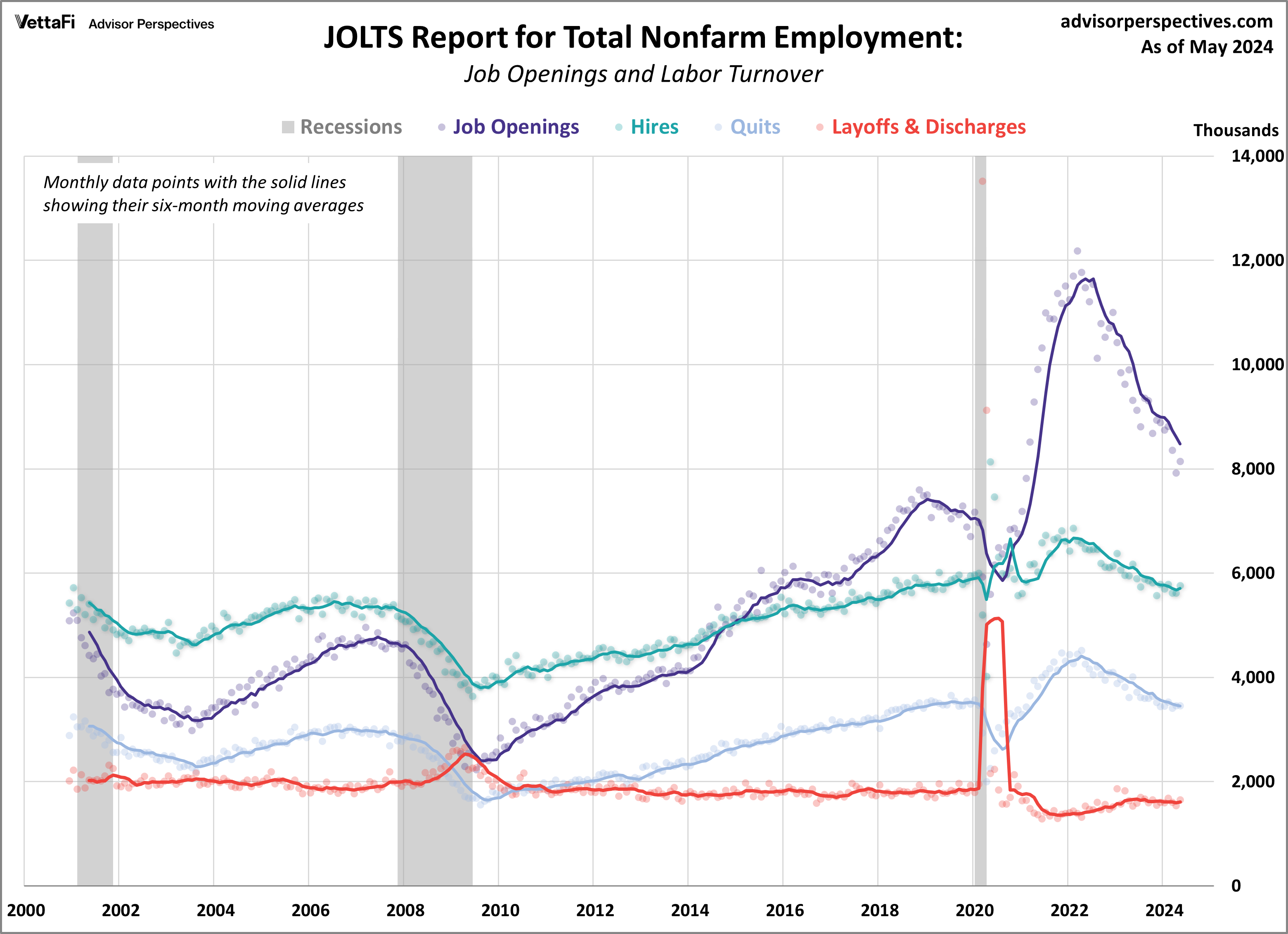

Job Openings and Labor Turnover (JOLTS)

Unlike the BLS’s June jobs report, the May JOLTS report highlighted a stronger than expected labor market as the number of jobs available increase for the first time in three months. The number of job openings increased by 221,000 to 8.140 million and came in above the expected 7.960 million vacancies. Despite the latest uptick, the overall trend in job openings continues to decline like it has over the past two years, slowly inching its way back to pre-pandemic levels. Other key data points from the report showed that the number of hires, quits, and layoffs increased from the previous month.

The JOLTS data serves as a barometer for assessing labor demand, and any disparity between workforce demand and supply could potentially exert upward pressure on inflation. Since the beginning of 2023, the gap between the two has consistently narrowed as job openings have steadily declined since their March 2022 peak. May, the number of job openings per employed worker remained at 1.22, the lowest level since June 2021.

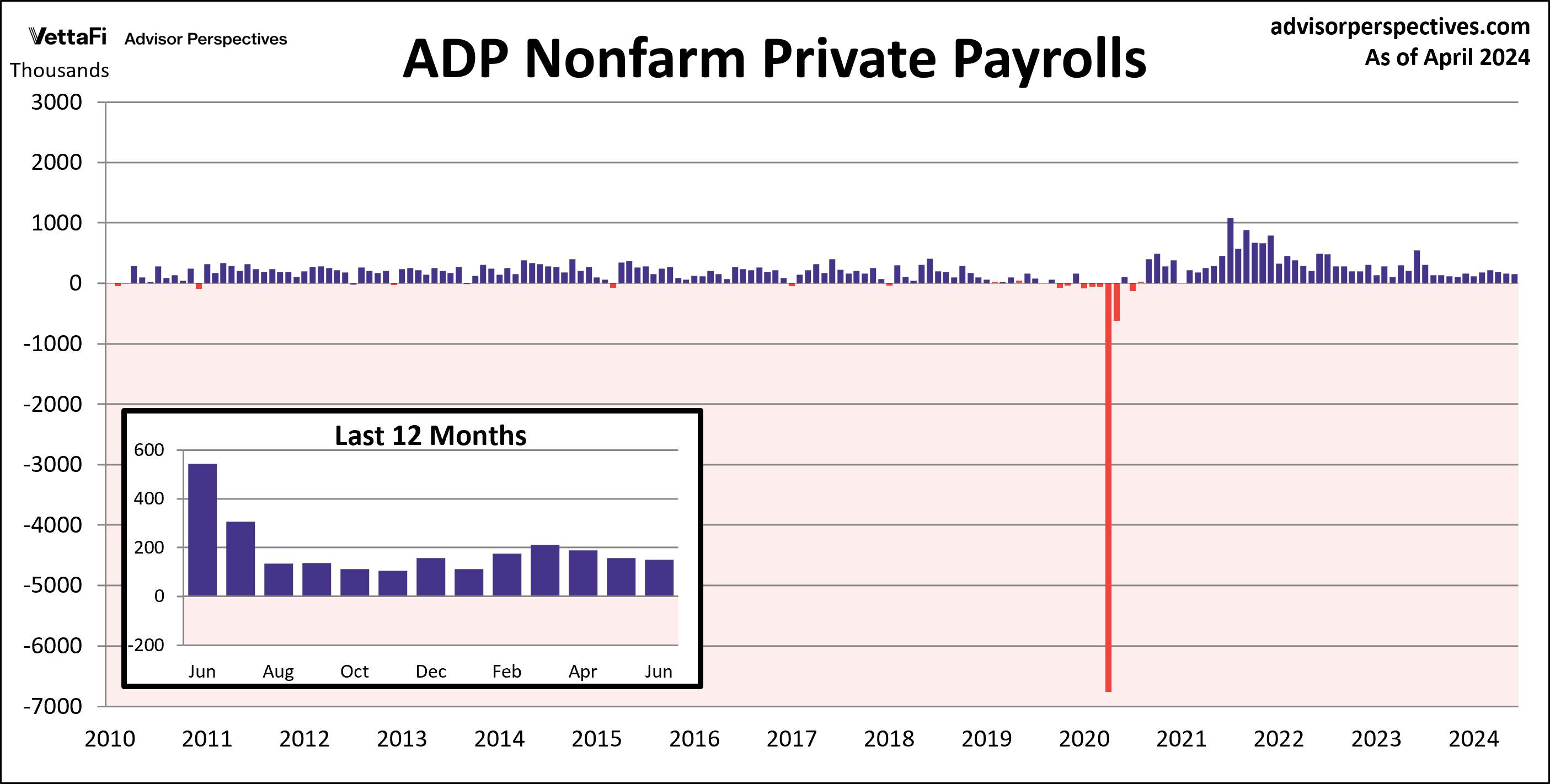

ADP Employment Report

In yet another sign of a cooling labor market, private sector hiring slowed for a third straight month in June by adding the fewest number of jobs in the past five months. According to the ADP employment report, 150,000 private jobs were added in June, less than the projected 163,000 addition. The pickup in May was most notable in the leisure and hospitality industry. It added 63,000 jobs last month, accounting for over 40% of June’s private job growth. Additionally, midsize companies (50-249) employees hired 65,000 jobs last month. Smaller companies (20-49) decreased hiring for a fifth straight month.

The report also revealed a slowdown in pay growth for both job-stayers and job-changers. Pay gains for job-stayers were up 4.9% year-over-year, the slowest pace in almost three years. Meanwhile, pay gains for job-changes slowed for a third straight month to 7.7% year-over-year. But they remain higher than at the start of the year.

Economic Indicators and the Week Ahead

This week’s economic calendar will feature the latest inflation and consumer sentiment data. On Thursday, the Bureau of Labor Statistics will release June’s Consumer Price Index (CPI). That will be followed by the Producer Price Index (PPI) on Friday. Consumer prices are expected to increase 0.1% and 0.2% from June for the headline and core indexes, respectively. Producer prices are expected to increase 0.1% and 0.2% for the headline and core indexes, respectively. Also on Friday, the preliminary report for the Michigan Consumer Sentiment Index, which could impact interest in the Consumer Discretionary Select Sector SPDR ETF (XLY), will reveal if consumer attitudes continue to worsen or if they have picked back up this month.

For more news, information, and analysis, visit VettaFi | ETF Trends.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more commentaries by VettaFi