Multi-Asset Mid-Year Outlook Global Growth Picture Supports Risk Assets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGlobal economic conditions continue to normalize, led by strength in the US and more stability in the euro area and UK. Consumer and business sentiment are also improving, as household incomes start to grow and borrowing rates have likely peaked. With inflation now cooling in more markets, rate-cut expectations have been pulled forward, especially in the US.

In this environment, we think multi-asset investors should consider adding to high-quality equity exposure as well as select opportunities in bonds.

More of the World’s Economies Sputter to Life

With pandemic excesses fading, the economic outlook is likely to improve across a wider swath of markets. US growth has continued to outpace that of other developed markets (DM), but we expect the gap to narrow.

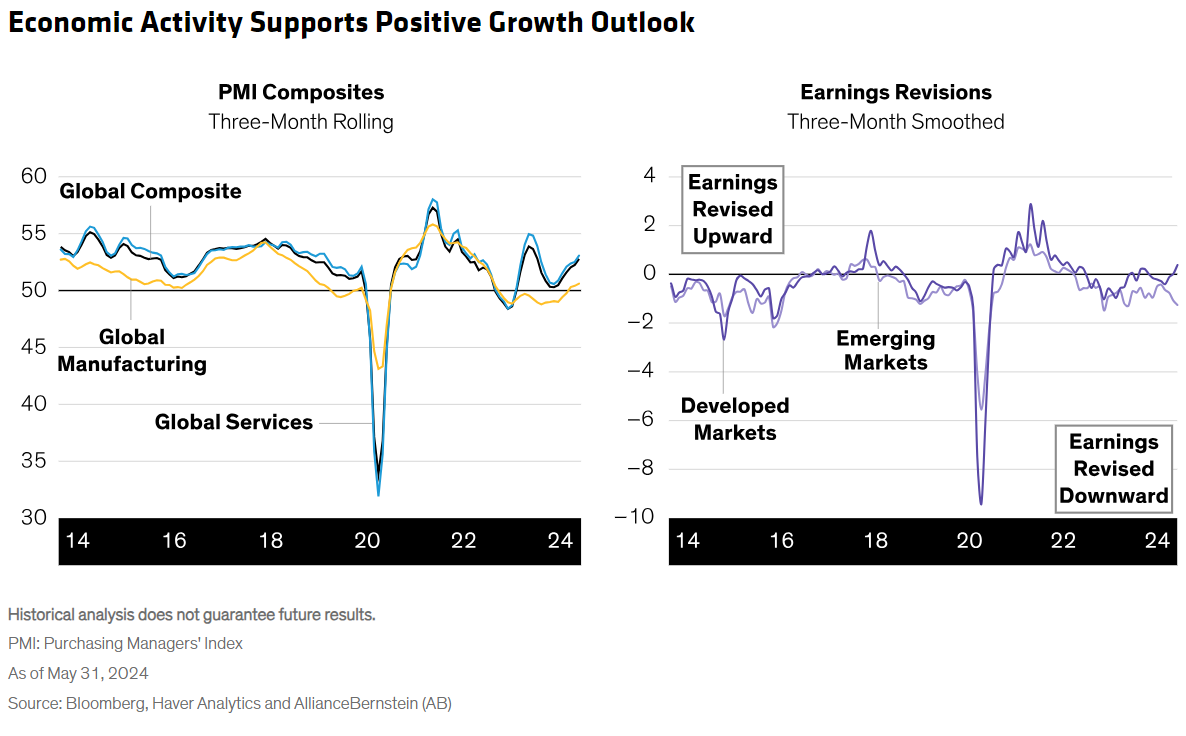

Global manufacturing is also on the mend after several years of drag from excess inventories, and services output is broadly in line with prior mid-cycle highs (Display, left). Strong nominal growth and fading headwinds for corporate margins have boosted earnings growth across developed markets, and expectations have been revised upward (Display, right). The earnings outlook for emerging markets has been more subdued, hampered by China’s lackluster growth and pricing power.

Households Continue to Spend, Business Investment Slowdown Is Shallow

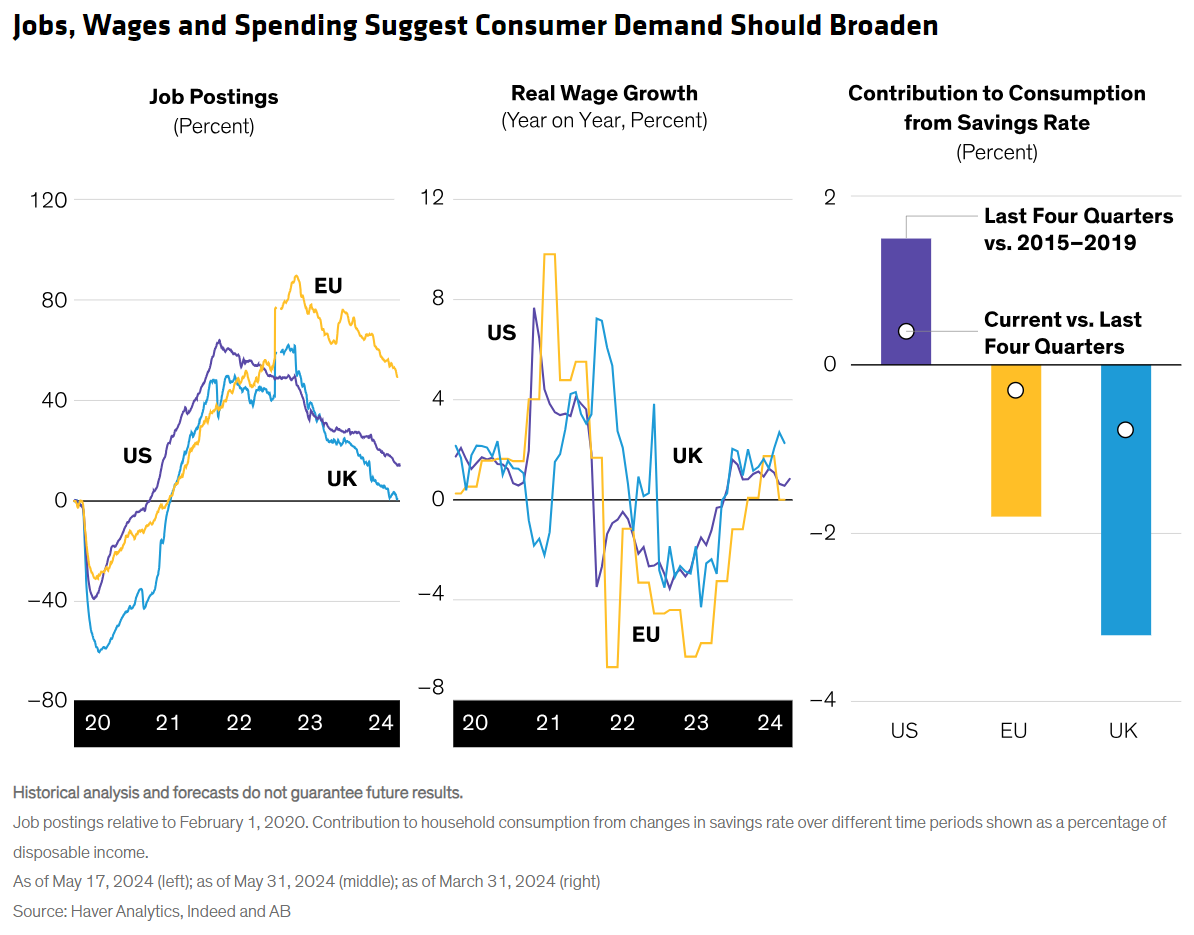

US household spending has been a key growth engine, but we expect ex-US growth to improve as well. Labor markets are one reason: they’ve been just as robust in the European Union (EU) and UK as in the US (Display, left), and real wage growth has accelerated as inflation pressures waned (Display, middle). However, households increased their savings rate in the euro area and UK, which weighed on spending power; the opposite was true in the US (Display, right). As confidence improves, we expect EU and UK household saving rates to at least stabilize or decline toward historical levels, which should bolster consumption.

With interest rates higher for longer, investors have been concerned about a potential drought in business investment. But spending has been resilient, cushioned by AI-aided growth in technology investment. So far in 2024, expectations for business investment have been revised up, now calling for only a modest deceleration in growth from very strong 2023 levels.

Inflation Rates Approaching Central Bank Targets

Inflation is now in the 2% to 3% range across many developed economies, and central banks have started to ease their exceptionally tight monetary policies.

While goods inflation is generally back to pre-pandemic dynamics, services inflation remains elevated, though we think relief is coming. For instance, housing inflation is high, but it reflects transaction data, which has a substantial lag, suggesting that housing inflation should continue to cool in the coming months. Meanwhile, consumer-staples companies and restaurants are noting an increasingly value-oriented consumer: with the cost of inputs relatively steady over the past year, we expect firms to revert to a more normal pace of price increases compared to immediately after the pandemic.

Wage inflation has similarly peaked, as labor markets have started to rebalance and the impact of inflation “pass through” has faded. Add rising labor-participation rates and migration, and labor markets are now less tight—even with strong job creation. These improvements should help ease central banks’ concerns about wage-price spirals.

China Growth Likely to Remain Subdued

Growth in China remains lackluster, dragged down by the continued contraction in the sizeable property sector. Rebalancing the sector’s excesses has been a key policy priority that could take years, weighing on growth in China and driving disinflation to the rest of the world.

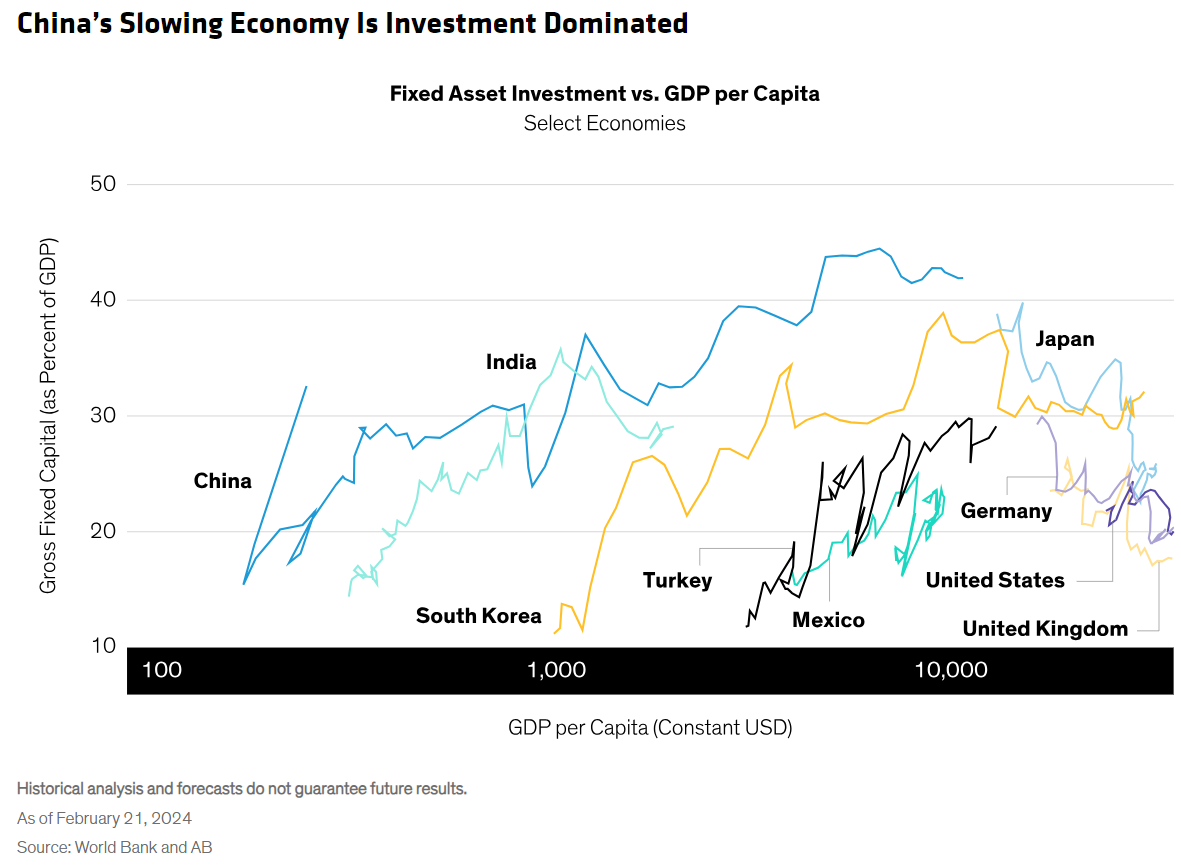

A key challenge for policymakers is maintaining growth around the official 5% target while rebalancing the economy. Fixed asset investment (which includes property, manufacturing and infrastructure) accounts for about 40% of the economy, an exceptionally high level compared to China’s peers (Display).

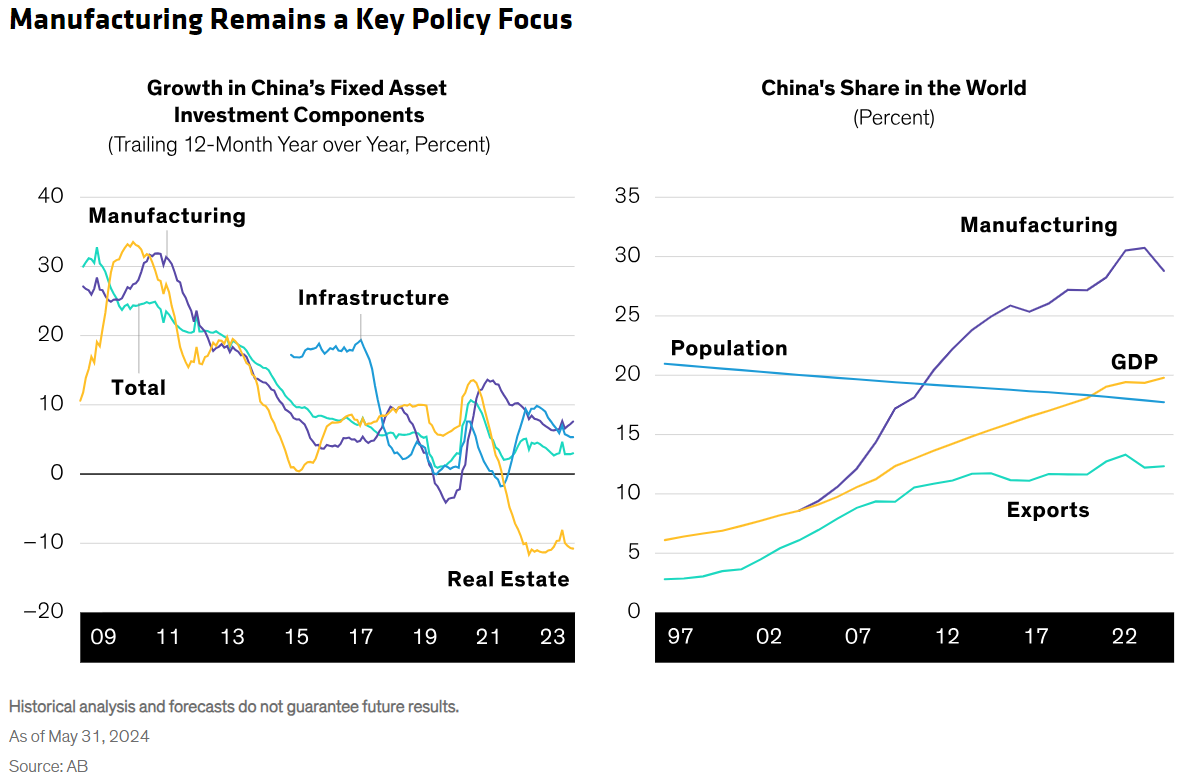

China surprised markets by cutting short- and long-term interest rates immediately after the Communist Party’s third plenary session in July. This may send a positive signal, but we don’t believe these actions will have a meaningful impact on broader issues in the property sector. So far, policymakers have offset the contraction in property investment by ramping up manufacturing investment. Manufacturing is growing the fastest among fixed-asset-investment components—with infrastructure a close second (Display, left). The manufacturing emphasis has helped China gain share in global production capacity and exports (Display, right). Renewables are a case in point: China quickly dominated the solar energy market and has become a global powerhouse in electric vehicles. Today’s excess capacity has helped drive down global prices in both sectors.

Over the long term, the more sustainable policy path would be a gradual move toward a consumer-driven economy, given that high household saving rates and net worth suggest consumption potential. However, with much of household wealth tied up in housing and with limited social support, consumers probably won’t have the impulse needed to keep growth at target levels.

Instead, policymakers appear likely to continue leaning on manufacturing investment, which will add to global capacity. Resolving the property glut while creating another glut in manufacturing will likely put downward pressure on global inflation. The reason: the property sector slowdown will shrink demand for construction materials, creating excess capacity in manufacturing and forcing down prices, particularly among renewables.

What the Current Landscape Means for Multi-Asset Positioning

With economic growth broadening, we see the investment backdrop as favorable for risk assets such as equities. Global stocks made strong gains through midyear, but opportunities remain in high-quality stocks that haven’t yet been rewarded. In developed markets, we see the greatest potential in the US, Europe ex UK and Japan. Emerging market equities also gained in the first half of 2024 but lagged developed markets, given China’s challenges. We see select opportunities in emerging equities, investors should be extra vigilant.

In light of high yields and falling inflation, we see an improving backdrop for bond exposure, particularly among select sovereign bonds. High-yield credit offers strong fundamentals but spreads are near historical lows, so in our view they may not offer the risk/reward potential of equities.

With inflation easing in more countries, monetary-policy headwinds should continue to fade. Equity valuations are elevated, but earnings growth may still power positive excess returns, and bond market conditions are gradually becoming more attractive. As always, it’s important for multi-asset investors to stay flexible and selective to effectively navigate a dynamic environment.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All