As expected, the Federal Reserve kept the target range for the federal funds rate at 5.25% to 5.5% at its July meeting, but it opened the door to cutting rates at an upcoming meeting. The decision to leave the policy rate unchanged was unanimous. This meeting was not accompanied by an updated Summary of Economic Projections, but the accompanying statement and comments from Fed Chair Jerome Powell at the press conference support our expectation that a rate cut is likely coming in September.

The time to cut is getting close

There were important changes in the statement that suggest a rate cut is coming soon. The Fed noted that it is "attentive to the risks to both sides of its dual mandate" referring to the requirement to target both low inflation and full employment. For the past two years, since the rate-hiking cycle began, the Fed has focused almost entirely on its inflation mandate. To us, this appears to be a signal that the Fed is preparing to ease policy due to growing concerns that high interest rates are having a negative impact on the economy.

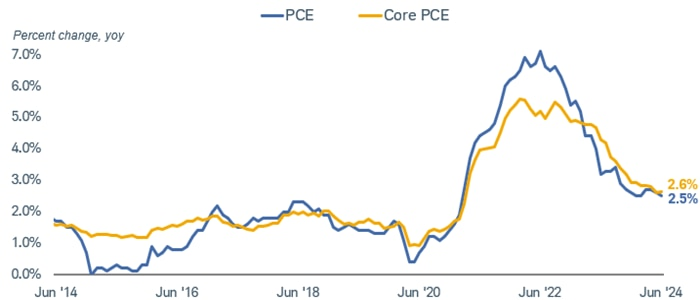

The wording around achieving its inflation mandate indicated more confidence, with the Fed noting that "there has been some further progress toward the committee's 2% inflation objective," changing the previous statement that inflation "remains elevated" to "is somewhat elevated." In addition, the Fed noted that job gains had moderated, and the unemployment rate has moved up, although Powell still described the job market as solid.

The Fed is still hesitating

As much as we would like to see the Fed get started with a rate-cutting cycle, there is still some hesitance. One key part of the statement remained unchanged, suggesting that the Fed is not yet ready to reduce interest rates: "The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%." In his press conference, Powell said that the committee was growing more confident, but it wants even more confidence. Presumably, that means that Fed officials want to see a few more months of economic data before shifting policy.

Policy makers have been concerned about allowing inflation to rebound. While inflation has fallen sharply from the pandemic highs and is headed toward the Fed's 2% target, allowing more time to make sure that the trend is intact reduces the risk of a policy mistake that could allow inflation or inflation expectations to rebound.

Inflation has eased

Source: Bloomberg, monthly data as of 6/30/2024.

PCE: Personal Consumption Expenditures Price Index (PCE DEFY Index), Core PCE: Personal Consumption Expenditures: All Items Less Food & Energy (PCE CYOY Index), percent change, year over year.

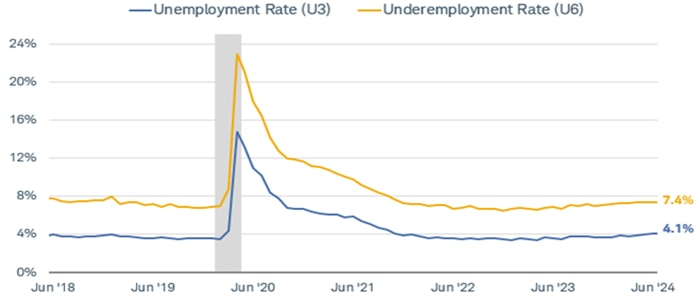

However, waiting too long to cut rates could mean a policy error that slows the economy too much, raising the unemployment rate and risking recession. Powell has indicated that the committee believes its policy stance is restrictive, with real interest rates high enough to have a negative impact on economic activity. The key metrics to watch are the unemployment rate, along with the pace of job and wage growth. The unemployment rate has already moved up from a low of 3.4% in April 2023 to 4.1% last month. Given the long lags between changes in monetary policy and the effects on the economy, the risks now seem skewed toward a weaker economy.

The unemployment rate has increased

Source: Bloomberg, monthly data as of 6/30/2024.

U-3 US Unemployment Rate Total in Labor Force Seasonally Adjusted (USURTOT Index) and US U-6 Unemployed & Part Time & Margin % Labor Force & Margin SA (USUDMAER Index).

In summary

We continue to expect the Fed to cut the federal funds rate by 0.25% to a target range of 5.0% to 5.25%, most likely in September, with one or two more likely by the end of the year if the current trends with inflation and the labor market hold. For bond investors, reinvestment risk has already arrived, as Treasury bills with maturities of six or 12 months have already fallen below the current fed funds rate. We expect that trend to continue.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0724-H4MA

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Charles Schwab

Read more commentaries by Charles Schwab