The Next Episode for Jobs, Inflation, and the Fed

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIf there was ever a doubt that big-picture, macro issues were not back in vogue, last week helped settle the debate. Between mega-cap earnings results (which were largely met with a lack of investor enthusiasm), the Federal Reserve's decision to leave rates unchanged (which didn't reveal much more than what we already know about officials' views), and the July jobs report (which caused recession fears to spike), there was no shortage of news that drove an incredibly volatile week for stocks. In the span of three days, the S&P 500 had its best day since this past February and the second-worst decline of the year. Liz Ann certainly picked an interesting time to be on vacation!

Dual mandates no longer dueling

There was no major inflation news last week, given the Fed's preferred inflation gauge—the personal consumption expenditures (PCE) Price Index—was updated back on July 26th. Revisiting the results from that June data helps paint the picture for this report.

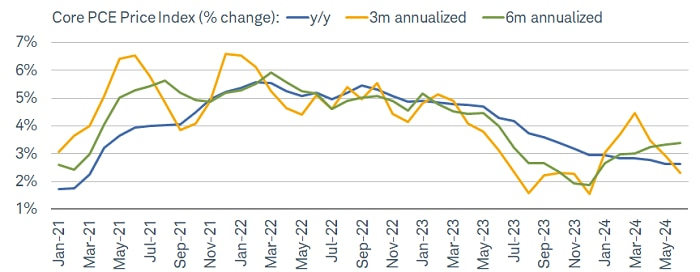

As shown in the chart below, it's clear that the disinflation trend has resumed. The three-month annualized change in core PCE (yellow line) has downshifted sharply after that brief, scary bump in the first quarter of the year. That should start to weigh on the six-month annualized change (green line) soon and keep the year-over-year change (blue line) in a downtrend. We're not back to the Fed's 2% target, but officials (and notably, Chair Powell) have mentioned several times that they'd like to cut rates before getting there.

Know your PCEs

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

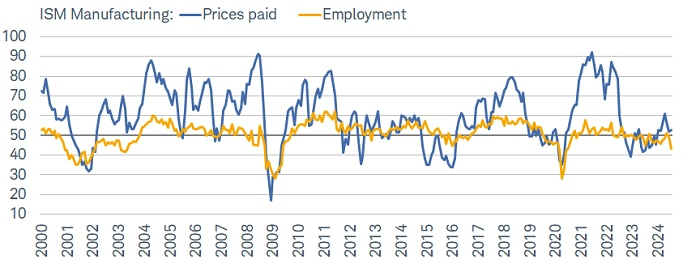

Bringing the Fed's other mandate—employment—into the picture, it's clear that the labor market is starting to have an increasingly negative reaction to higher rates. As shown in the chart below, the employment component in the ISM Manufacturing Index (another disappointing economic data release last week) slipped in July to its lowest since June 2020. Fortunately, that was accompanied by only a slight uptick in the prices paid component.

Employment sentiment sours

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 7/31/2024.

Key to keep in mind is that in this unique cycle, survey-based data like the ISM indexes have been harder to rely on when it comes to the direction of the economy. Case in point: Even though the above chart shows a marked decline in manufacturing employment for July, the Bureau of Labor Statistics' (BLS) July jobs report showed a gain of 1,000 manufacturing jobs, as well as a gain of 25,000 construction jobs.

One flag, two flags, yellow flags, red flags

That said, though, it's getting harder to deny some of the more traditional recession warnings in the labor data. At first glance, July's jobs report was not bad: 114,000 jobs added, an unemployment rate at 4.3%, and the highest prime-age labor force participation rate since March 2001–not to mention Hurricane Beryl's potential impact on payroll growth (there was a huge spike in individuals not at work due to weather). However, the true weather effect is hard to measure, and trend is much more important at this stage of the cycle.

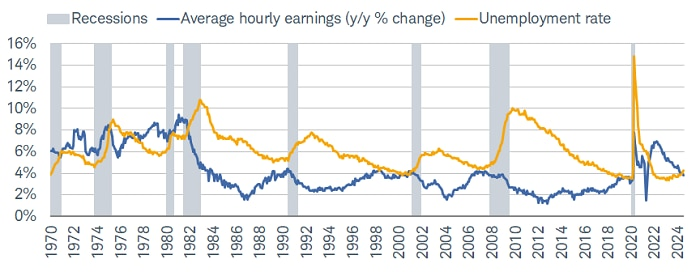

As shown in the chart below, the unemployment rate has been creeping higher over the past year as year-over-year growth in average hourly earnings has been slowing. Both trends tend to be consistent with a recession already (or shortly) underway.

Labor market whispers "recession"

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 7/31/2024.

Average hourly earnings for production and nonsupervisory workers.

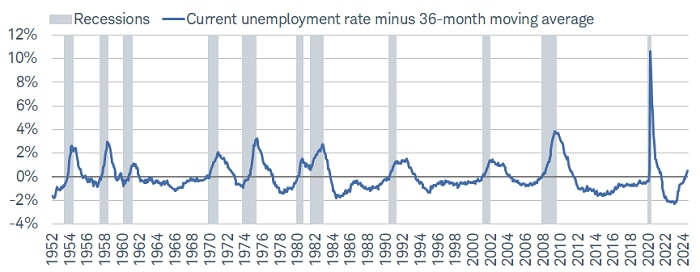

The rise in the unemployment rate in July got the most attention; and rightfully so, given its larger-than-expected increase from 4.1% to 4.3%. Even more notable is how far above its longer-term average it now is. As shown in the chart below, the spread between the current rate and its rolling three-year average is now 0.5 percentage points. Going back to the mid-1950s, we have never seen a spread that wide without the economy already being in a recession. As we've mentioned several times, this is a unique cycle, so we shouldn't be too dogmatic when it comes to one single indicator, but we do think this is a worrisome trend worth monitoring.

Unemployment rate red flag

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 7/31/2024.

Average hourly earnings for production and nonsupervisory workers.

The downside is that the cracks under the labor market's surface we have been monitoring are widening. From an inflation perspective, the upside is that it's getting harder to see where upward pressure on prices is going to come from. An increasingly soft labor market is consistent with slower wage growth, slower spending, and disinflation.

Labor-driven inflation pressures fading

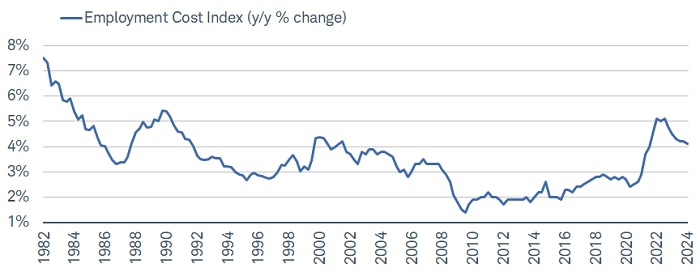

We're continuing to see that via metrics like the Employment Cost Index (ECI). As shown in the chart below, the year-over-year change in the ECI has rolled over and slowed to just slightly above 4% through the second quarter of this year. That's elevated relative to the pre-pandemic expansion, but it's getting closer to the long-term average.

Compensation pressure fading

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

The Employment Cost Index (ECI) is a quarterly economic series published by the Bureau of Labor Statistics that details the growth of total employee compensation.

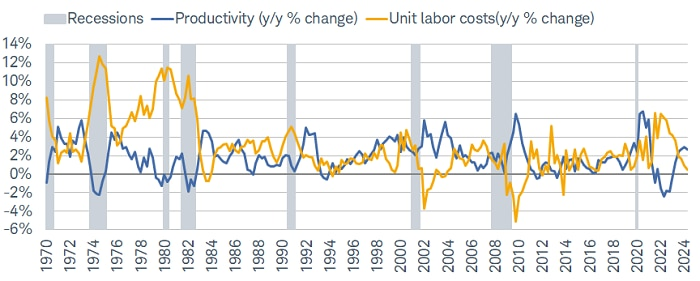

The easing in compensation costs is consistent with a marked slowdown in unit labor cost growth, which was the standout data release last week. As shown in the chart below, the year-over-year trends in productivity and unit labor costs continued to move in the right direction through the second quarter. For the latter, annual growth was the slowest since the third quarter of 2019. This is perhaps the clearest way to see that the economy is not facing a wage-price inflation spiral like it did in the 1970s and 1980s.

Great quarter, guys

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 6/30/2024.

All else equal, the fact that the rate of inflation is outpacing unit labor cost growth is good news for companies and their profit margins. However, as the current earnings season has revealed, there are more than enough cases of companies losing their pricing power; and for those that have been able to maintain it, the ability to do so might not last much longer if the labor market continues to deteriorate.

Ready or not: here cuts come?

The July jobs report was met with a sharp decline in risk assets and bond yields, as well as a chorus of Fed watchers saying the central bank was wrong to hold at the July meeting. As such, the market has started pricing in larger rate cuts (50 basis points) for upcoming meetings. That might raise suspicion that the economy is deteriorating quickly, but there is a difference between the Fed dialing back its restrictiveness at an aggressive pace and slashing rates to try and save a faltering economy. It's entirely possible that the former scenario plays out; what might be difficult is officials having to communicate that in a reassuring way.

As such, we expect volatility to remain elevated in both the market and economy over the next several months. Expectations for Fed rate cuts will jump around swiftly given the slew of crucial data until the September meeting; as well as the Kansas City Fed's upcoming annual Jackson Hole summit. Assuming the current inflation and labor trends continue to hold, though, the economy's message to the Fed is clear: It's time to start getting much less restrictive.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

0824-HSL2

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All