In the first half of 2024, economic growth was solid and inflation rates remained sticky, leading capital markets to dial back expectations for policy rate cuts this year. Stock and bond markets, which had tracked closely in 2022 and 2023, began to diverge in 2024, with stocks rallying even with bond yields rising for a good portion of the first half.

Being too defensive in a multi-asset income strategy during 2024 might have cost investors some equity upside, even accounting for a particularly rough early August for markets. Some of the recent weakness may be technical, driven by elevated positioning. To the extent that this is true, it may point to a good entry point for investors—providing that the economy achieves a soft landing.

On the economic side, we’ve raised our gross domestic product forecast for this year, with the US forecast at 2.4%, just below last year’s growth and near the long-term trend. Europe is likely to accelerate modestly as recession fears recede. We expect inflation to continue cooling: US progress ebbed earlier in the year, but the last two releases have been softer than expected. Across several major economies, inflation is now running in the 2% to 3% range.

Lower inflation has opened the door for the Federal Reserve to start cutting rates, joining other central banks including the Bank of Canada and the European Central Bank. A soft-landing, lower-inflation scenario seems favorable for risk assets, including equities. And with bond yields still relatively high, fixed-income offers strong income and return potential. It’s a landscape that’s compelling for multi-asset income strategies—particularly those with the flexibility to shift across and within asset classes.

Equity Returns Could Be Ready to Broaden…and Rotate

Many of the first half’s equity trends continued from 2023, though signs of market returns broadening beyond a few highfliers had emerged early in the second half. Last year, the Magnificent Seven powered 60% of the S&P 500’s returns. We saw a similar share earlier this year, but investors may be becoming more discerning on fundamentals and expected earnings growth.

Signs of potential rotation are also visible. Returns for emerging market equities have lagged those of developed markets for a while but have outperformed them over the last three months. July featured the largest rotation from large-caps to small-caps in over 20 years: the Russell 2000 Index recently recorded its largest two-week rally against the Nasdaq 100 since 2002.

Given our base-case forecast for a soft landing, we think maintaining some exposure to equities makes sense in a multi-asset income strategy. But investors should also be watching for opportunities to rotate. Since early 2023, we’ve made the case for a tilt toward large-cap, quality growth stocks. We still see a core role for this segment, but richer valuations and a lofty earnings bar tilt the balance of risks toward other segments—even after some rerating in early August.

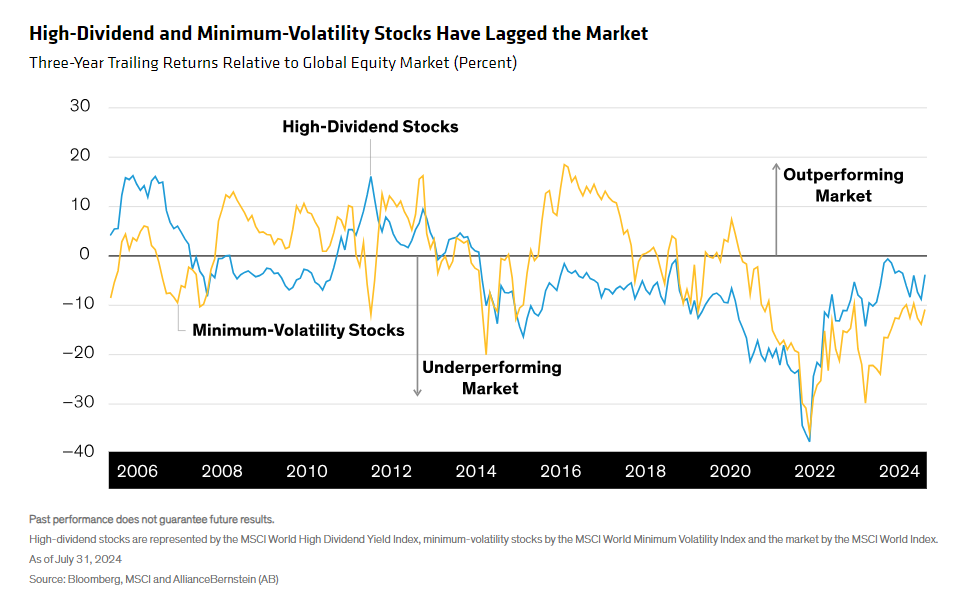

We see scope for earnings growth to broaden as growth moderates and the rate-cut cycle picks up steam. In fact, we had seen some signs of this before the early August downturn. Defensively oriented equity segments have lagged during a dominant period for mega-cap tech (Display), but they have a chance to catch up. They also offer potential downside mitigation in case the economic picture unexpectedly deteriorates.

Small-caps have rallied after trailing large-caps for a long stretch, and we see more upside possible from rate cuts and potential political tailwinds if a US leadership change increases a focus on domestic matters. But prudent position sizing and a selective approach are key. That’s because small-cap indices include many unprofitable, low-quality companies highly levered to economic conditions.

Geopolitical and Election Risks Moving Closer on the Horizon

Risk, particularly in equity markets, has been well below average over the past couple of years. However, as recent events have highlighted, we think that will change in the second half. Disruption could come from macro surprises to growth and inflation, markets wrestling with earnings surprises or election risks. These risks are the same as earlier in 2024, but they’re now closer on the horizon—and in some cases, already on the scene.

The US general election in November is a likely focal point for market uncertainty. Election years haven’t historically altered market returns relative to nonelection years, but they have rattled markets. With more political polarization and clear policy differences, and with equity risk having been at a low level, investors should expect choppier waters than usual in the second half.

Bonds Highlight the Value of Diversification—and Income Potential

Possible market turmoil makes diversification a point of emphasis. One avenue is a more balanced approach in equity allocations. Bonds also play a big role. High starting yields bolster income potential and, in our view, could cushion against potential volatility. They played this role well in the recent equity sell-off, with substantial yield declines boosting prices. With inflation cooling and rates likely to follow, we think prospects for bond returns are sound.

High-yield credit is an attractive income source, and our expectation for a moderate macro backdrop bodes well for this asset class. A “not too hot, not too cold” growth scenario has typically been the sweet spot for high yield, and a soft landing in the US is still our base-case forecast. Credit spreads have seemed tight historically, though they widened with the market turmoil. Previous cycles suggest that—absent a recession—spreads could stay at these relatively tight levels for some time.

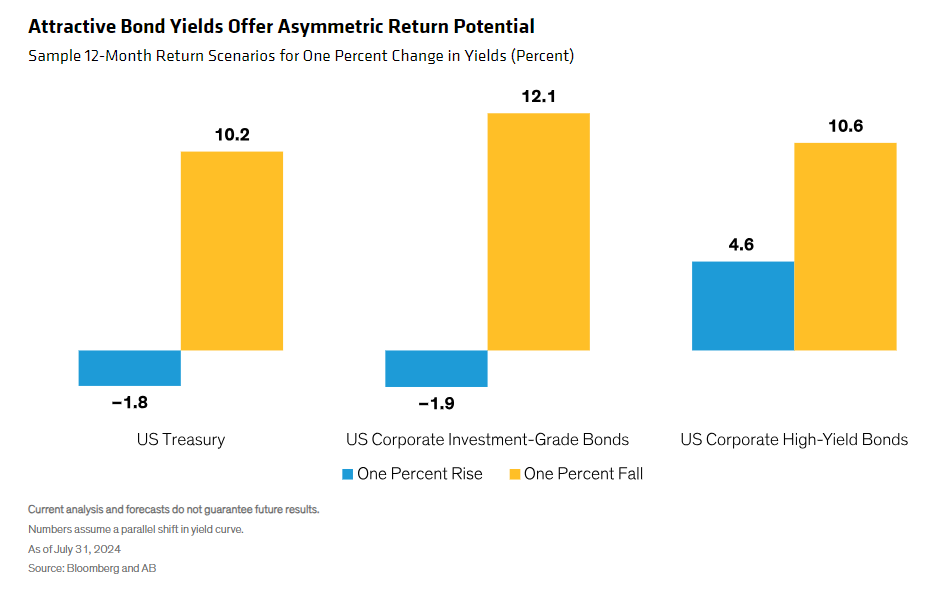

The quality of the high-yield universe has improved in recent years, with the share of BB-rated issuers climbing and CCC issuers falling, so we think credit spreads are more constructive than they appear at first glance. What’s more, high starting yields provide a degree of convexity in fixed-income exposure (Display), with high coupons boosting upside potential while helping compensate for any potential downside.

Combining equity and credit exposure may also produce complementary exposures to industries—and, by extension, business types. Global stock indices tend to be more tech heavy, and global credit indices more cyclical—often with greater exposure to industries such as energy. This mix may produce a diverse mix of firms that traditionally outperform in different economic and market environments.

The Big Picture: Positive Income Backdrop, but a Dynamic One

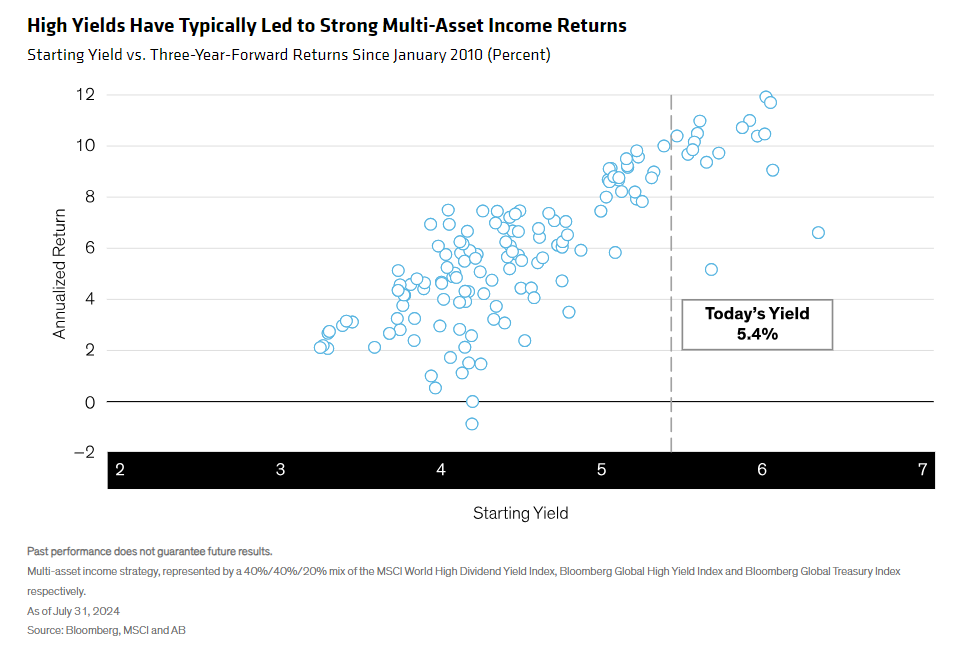

Multi-asset income strategies tap a range of asset classes, and we see promise on several fronts. After years of underperformance, income-oriented assets should be poised to revert. Today’s higher yields are a strong starting point for income, total return and diversification. Also, a relatively benign economic environment has historically been favorable for both equity and credit—and, by extension, multi-asset income strategies (Display).

But simply assembling building blocks isn’t enough, in our view. It’s critical to adapt the mix and design of those building blocks as conditions evolve. We think executing this effectively can help investors balance the mix of upside and downside risks as the second half of 2024 plays out—an important point punctuated in August.

As we survey capital markets, we see several paths to diversify equity allocations. Bonds offer more yield than they have in years—and should benefit when rates start falling. For investors seeking income and growth, we believe that a multi-asset strategy harnessing the income power of bonds and the growth potential of stocks can be a potent combination—if it’s managed dynamically.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© AllianceBernstein

Read more commentaries by AllianceBernstein