Economic indicators are released every week to provide insight into the overall health and performance of an economy. They serve as essential tools for policymakers, advisors, investors, and businesses. That's because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending August 8, the SPDR S&P 500 ETF Trust (SPY) fell 2.28%. The Invesco S&P 500 Equal Weight ETF (RSP) was down 2.00%.

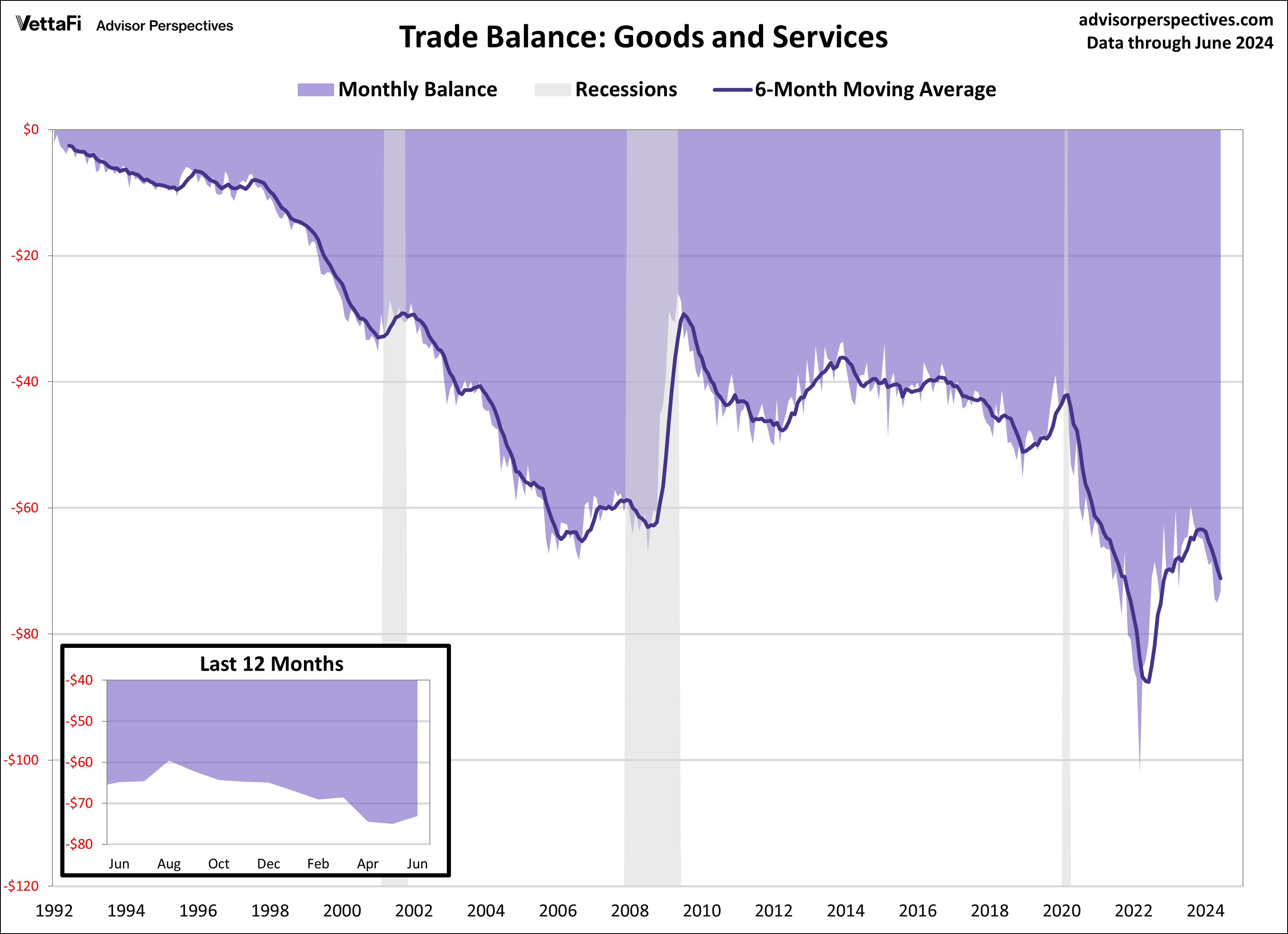

Despite the economic calendar’s light load last week, there were a few macroeconomic reports that warrant attention. Those are the quarterly household debt and credit report, the services sector PMI, and the trade balance. These data points can collectively provide insights into various aspects of the economy. These aspects include consumer behavior and service sector health. In this article, we will summarize the latest data on each of these indicators.

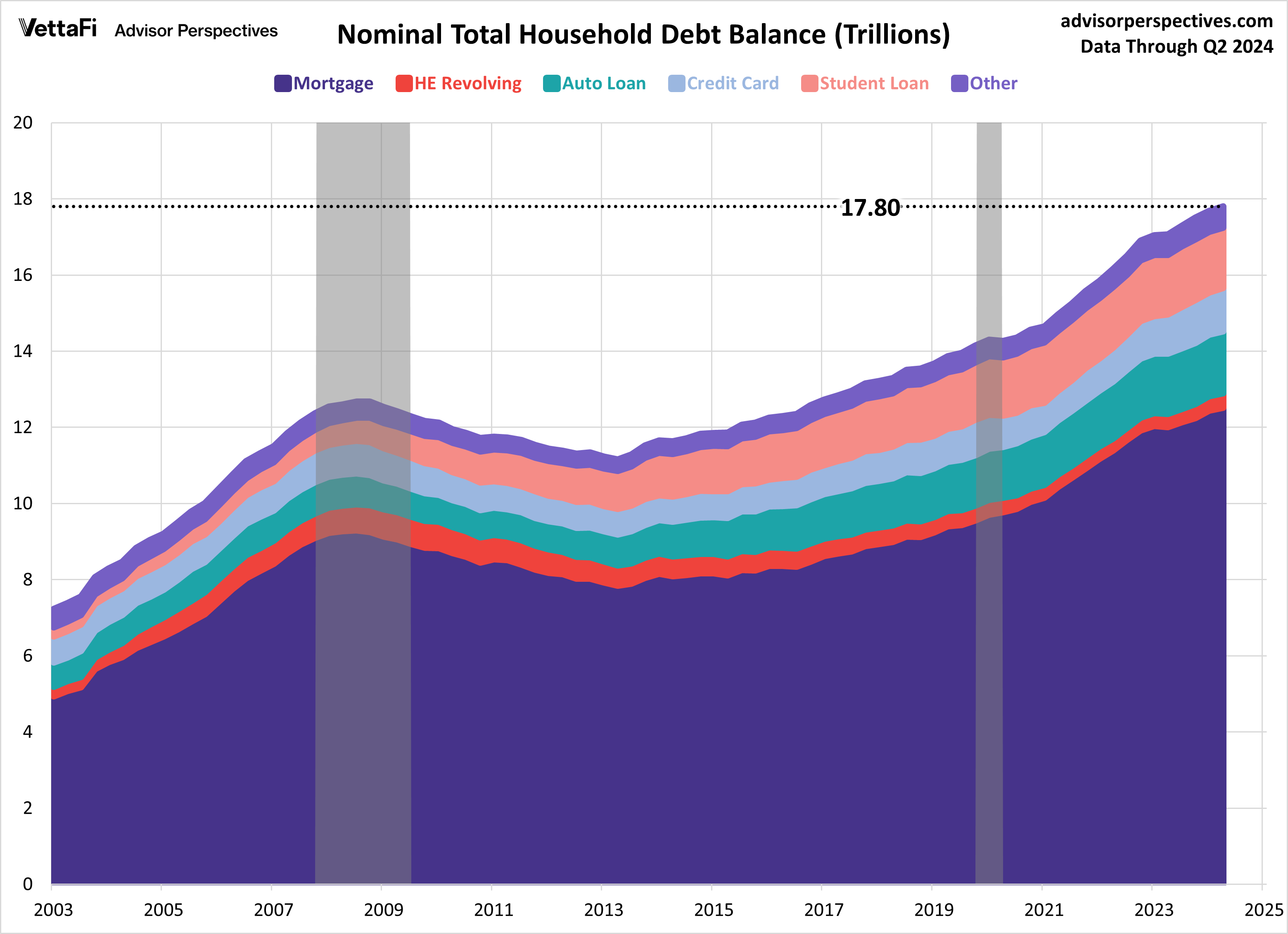

Economic Indicators: Household Debt and Credit

According to the latest household debt and credit report released by the New York Fed, household debt increased $109 billion in Q2 of this year to reach a record $17.80 trillion. The latest data represents a 0.62% increase from Q1’s debt level of $17.69 trillion. Most debt categories grew in the second quarter. The latest growth was primarily fueled by increased mortgage and credit card balances. Specifically, mortgage balances hit an all-time high of $12.52 trillion, a 0.6% increase from the previous quarter. Credit card balances reached a record high of $1.14 trillion, a 2.4% increase from the previous quarter. Student loan balances were the sole category that declined last quarter. They fell 0.6% to $1.59 trillion, its lowest level in a year. This comprehensive report serves as a gauge for the financial conditions of U.S. households, offering insights into their economic well-being.

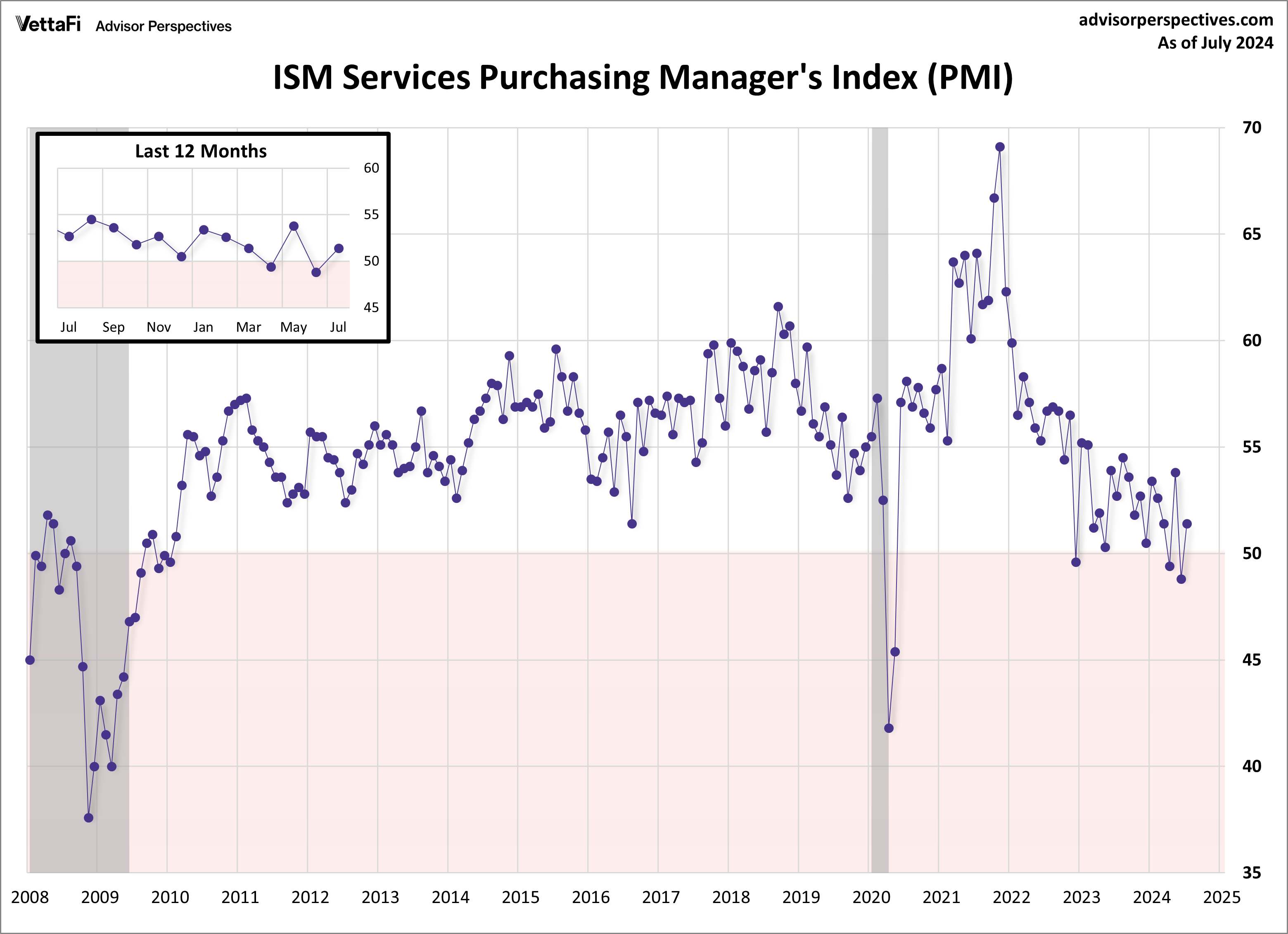

Economic Indicators: ISM Services PMI

Economic activity expanded in the services sector in July, marking the 47th month of expansion in the past 50. Notably, however, two of the three contraction periods have occurred in the past four months. The ISM Services PMI rose to 51.4 last month, as expected. The majority of the index’s subcomponents improved in July, apart from supplier deliveries and inventories. Additionally, ten service industries reported growth, while eight industries reported a decline. Overall, the business conditions in the services sector continue to steadily grow as many respondents commented on business activity being “stable,” “steady,” and “strong,”