Schwab Market Perspective: Spinning

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsListen to the latest audio Schwab Market Perspective.

Markets were rattled in recent weeks by fears that the Federal Reserve may have waited too long to begin cutting short-term interest rates, raising the likelihood of a potential recession. But whether those fears are justified is open to debate, and U.S. stock indexes quickly rebounded.

Meanwhile, investors in the popular "yen carry" trade were shaken when the value of the Japanese yen rose against the U.S. dollar, leading to the reversal of many of these trades—an unwinding that contributed to the market turmoil. Is it over now? Read on for our take on the situation.

U.S. stocks and economy: Are recession fears justified?

Recessionary concerns have continued to crop up given some worrisome developments in the labor market—emphasized by the worse-than-expected July jobs report. In addition to the unemployment rate's unexpected jump to 4.3%, payroll growth continued to slow. We still caution against looking at any single indicator to gauge the overall health of the labor market, however.

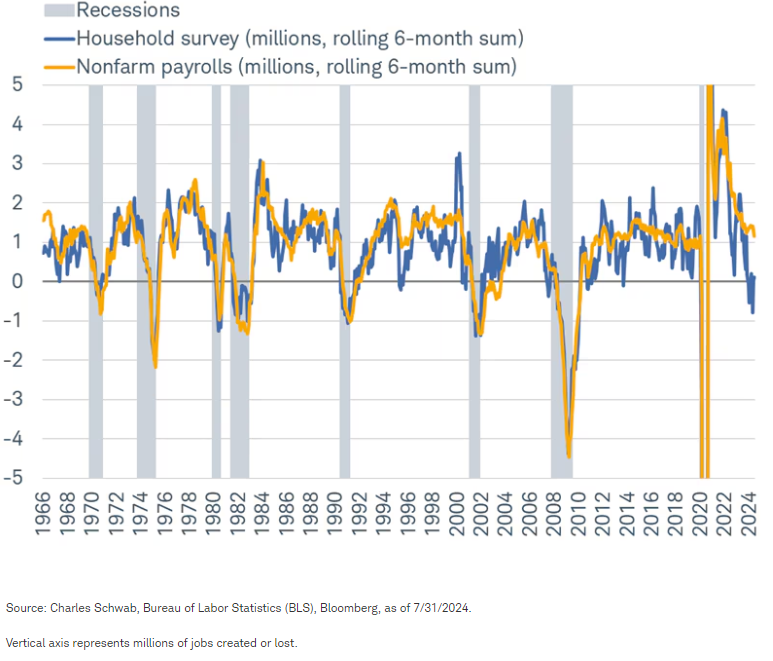

Case in point is the fact that there is still a huge gap between growth in payrolls (from the establishment survey) and household employment (from the household survey). As shown in the chart below, the former shows more than one million jobs created over the past six months, while the latter shows just 114,000 jobs created.

Two surveys, two tales

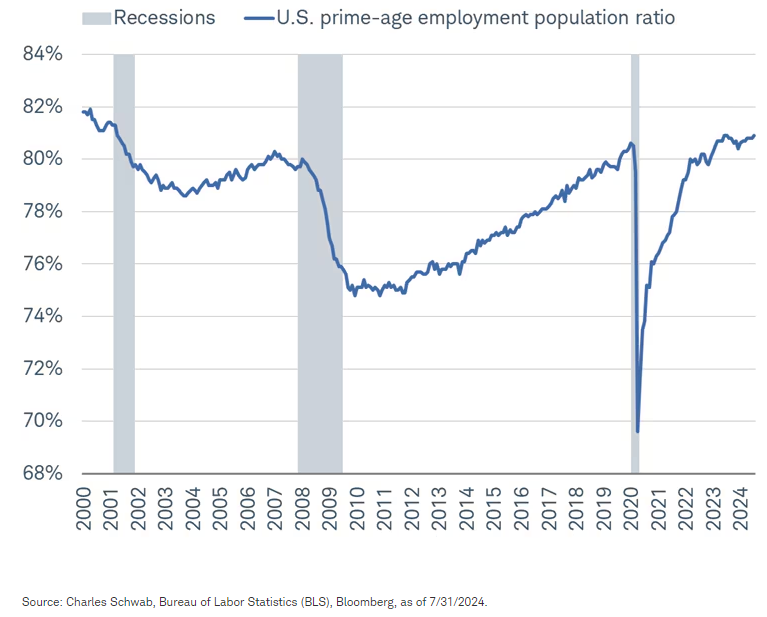

While it might be tempting to look at the rise in the unemployment rate and deterioration in household employment as surefire recession signals, there are other labor data that don't yet support the fact that the economy has already slipped into a recession. As shown in the chart below, the prime-age employment population ratio—which measures the proportion of individuals, ages 25 to 54, who are employed—is still rising and at a cycle high. A high and rising percentage is not consistent with the economy being in a recession.

Employment still strong

Market action signaling recession?

Elevated market volatility has exacerbated some of the recent economic fears, not least because of U.S. stocks' sharp selloff immediately after the release of the July jobs report—which culminated in a week that saw the S&P 500's worst and best daily gains of the year thus far. While some of the elevated recession fear is justified, we don't think the market is sending a recessionary signal.

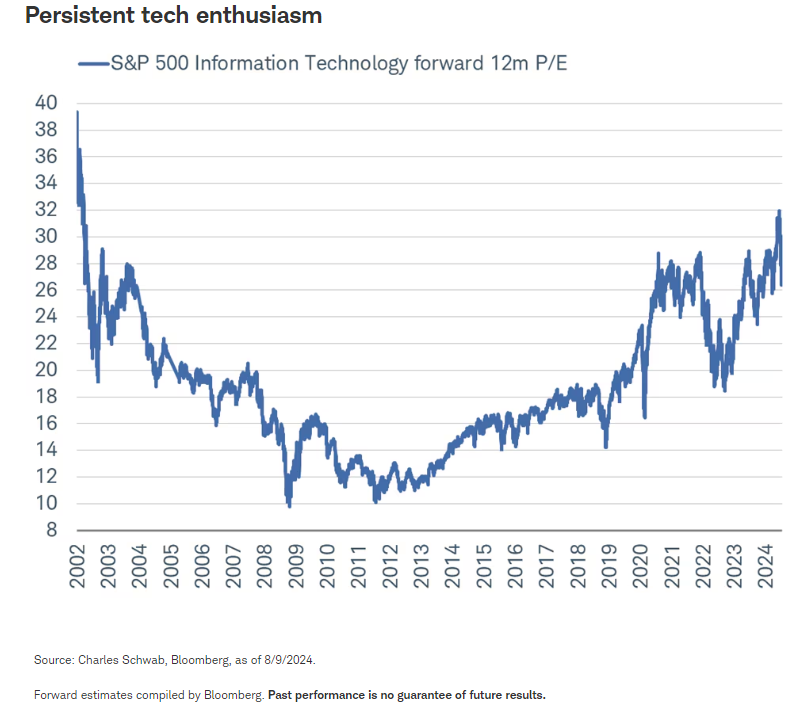

Since the S&P 500's most recent all-time high in mid-July, there are only two sectors underperforming relative to the index: Consumer Discretionary and Information Technology (tech). The latter had been the top-performing sector this year and (perhaps unsurprisingly) saw the strongest inflows on a rolling one-year basis. That coincided with a remarkable rise in its forward 12-month price-to-earnings (P/E) ratio. As shown in the chart below, tech's forward P/E—before the recent selloff—rose to its highest in more than 20 years.

The tech sector houses many of the market's heavyweight names and was the worst performer in the recent drawdown. Given that, as well as the fact that traditional cyclical sectors like Financials have fared much better, the market's message is that a popular theme has unwound in a rather dramatic and quick fashion. For now, investors' profit-taking in tech shouldn't be conflated with the market sending a recession signal. Of course, that can change if the labor market weakens at an aggressive pace, but for now, market signs of a downturn aren't yet abundant.

Fixed income: Volatility picks up

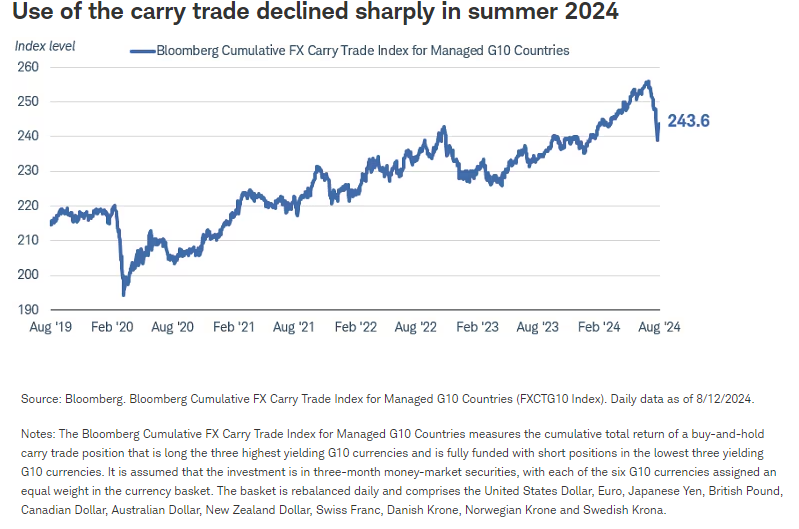

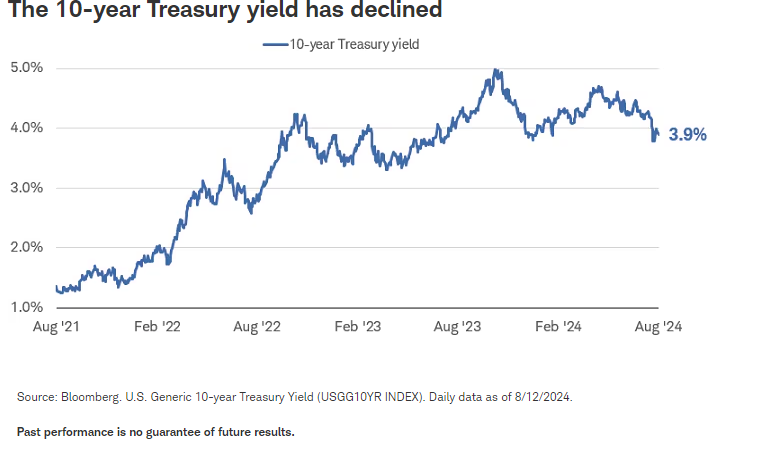

Bond yields dropped sharply in the past month, reaching the lowest levels in over a year amid high volatility. A weaker-than-expected August unemployment report pulled yields lower and raised concerns about a potential recession on the horizon. Market expectations for the timing and depth of Federal Reserve rate cuts accelerated. That news collided with a surprise interest rate hike by the Bank of Japan (BoJ). Investors in a popular strategy, the "yen carry trade" were shaken out by the rapid turnaround.

A "carry trade" describes when investors borrow in low-yielding currency to invest in one where expected returns are higher. Over the past several years, it has been profitable to borrow in Japanese yen with rates near zero and invest in U.S. stocks and other assets that have been rising. With the change in outlook, many of these trades were liquidated as the value plummeted.

The good news for U.S. bond investors is that Treasuries assumed their traditional role of a perceived safe haven asset during the market turmoil. Treasury bond prices soared, helping to offset declines in other parts of balanced portfolios.

Now that the dust has begun to settle, we look for yields to stabilize in a lower range than earlier in the year. In the Treasury market, intermediate- to long-term yields have already fallen to levels consistent with weaker growth, low inflation, and several rate cuts by the Federal Reserve. Ten-year yields reached our year-end target of 3.8% and fell even further before bouncing back. We expect the Fed to lower the target range for the federal funds rate by 75 basis points, or 0.75%, in incremental steps from the current range of 5.25% to 5.5%. More rate cuts are likely in 2025, with the potential for the federal funds rate target to fall to 3% to 3.5% in this cycle.

Although yields have fallen sharply, we still see opportunities in the fixed income markets for investors. In the Treasury market, yields for two- to five-year notes will likely fall further, lifting prices and producing positive returns. For investors with a longer time horizon, investment-grade corporate bond yields are in the 4.5% to 5% region. Although there is somewhat more credit risk there than in Treasuries, the risk/reward may be reasonable for investors wanting to capture those yields for a longer time period.

In the months ahead, there are likely to be more bouts of volatility, given the uncertainty about the economic outlook and the potential for more unwinding of leveraged trades. Fixed income can play its traditional role in a portfolio—providing income, capital preservation, and diversification from riskier asset classes.

Global stocks and economy: Is the great unwind over?

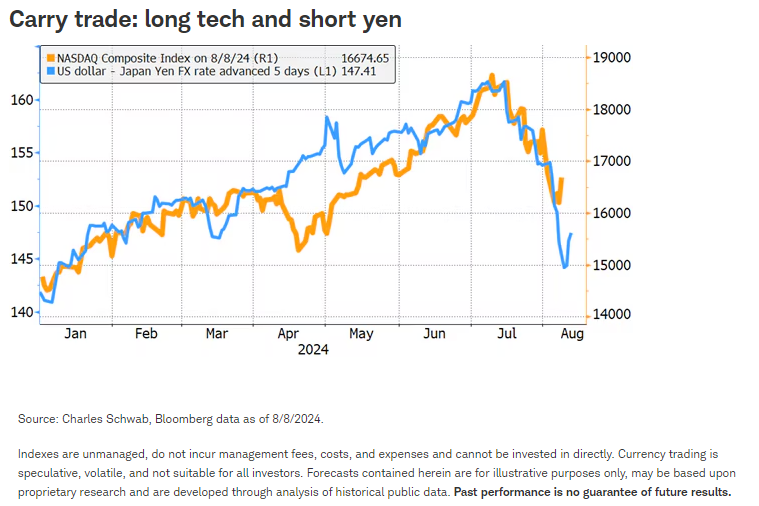

Going long on tech and short on the yen have been two very popular trades in recent years. With the yen the cheapest major funding currency—meaning it has been possible to borrow at the cheapest rate in yen—and since tech has tended to be consistently profitable, it's not hard to imagine a good portion of the short yen trade flow has gone into U.S. tech. The chart below of the similar movement in the dollar-yen exchange rate and the tech-heavy Nasdaq highlights the likelihood of carry trades funding investments in tech, but the trade likely funded buying in other markets as well.

After last week's dramatic moves, is the unwind of the carry trade now over? While it is impossible to say exactly how big the carry trade is, there are some indicators we can look at to see how far the unwind could still go on a short-, medium-, and long-term basis.

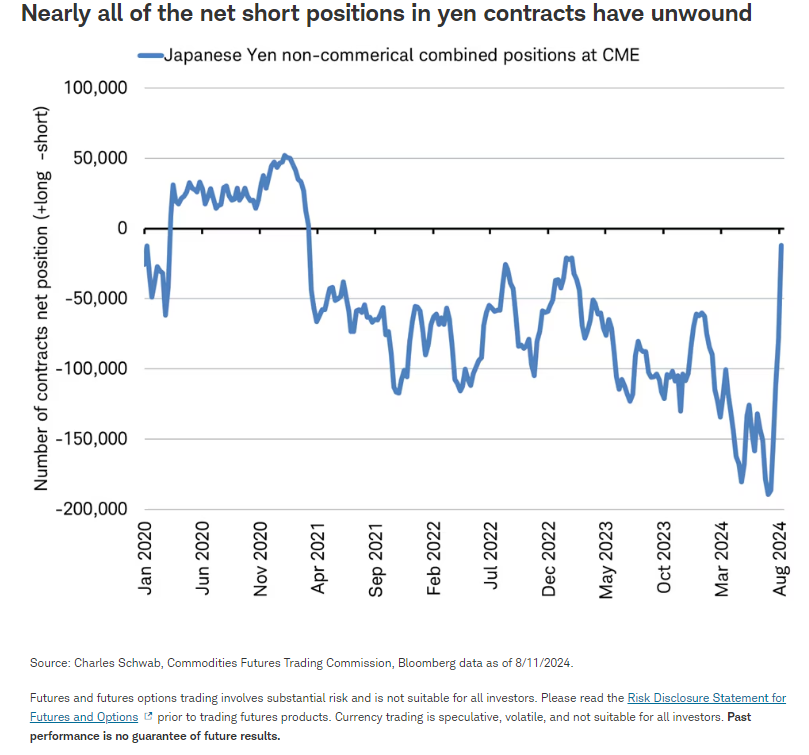

- Short-term: To look at the size of a potential for a short-term reversal, we can examine yen contracts tracked by the Commodity Futures Trading Commission. On July 2, speculative investors, like hedge funds, were holding a net 190,000 contracts betting on a weaker yen (worth about $15.6 billion). By July 31, the day of the BoJ meeting, those positions were halved and were nearly back to the flat line by Tuesday, August 6th. While positioning could further unwind and perhaps even turn long, we feel that most of the extreme short position is unwound.

- Medium-term: A proxy for the medium-term carry trade magnitude is to look at Japanese banks' foreign lending in yen. This type of lending is often to non-banks, like asset managers, and has been on the rise since 2010 and accelerated in the last couple of years as rates rose outside Japan while remained very low in Japan. According to the data released by the Bank of International Settlements, the loans totaled $1 trillion (145 trillion yen) as of March 2024. Unlike investors in futures that are subject to margin calls that can force urgent selling, asset managers may look to reduce any carry trades and pay back yen loans over the medium-term, dependent upon their outlook for currency and rate moves. This means an unwind of this exposure could unfold over the coming months.

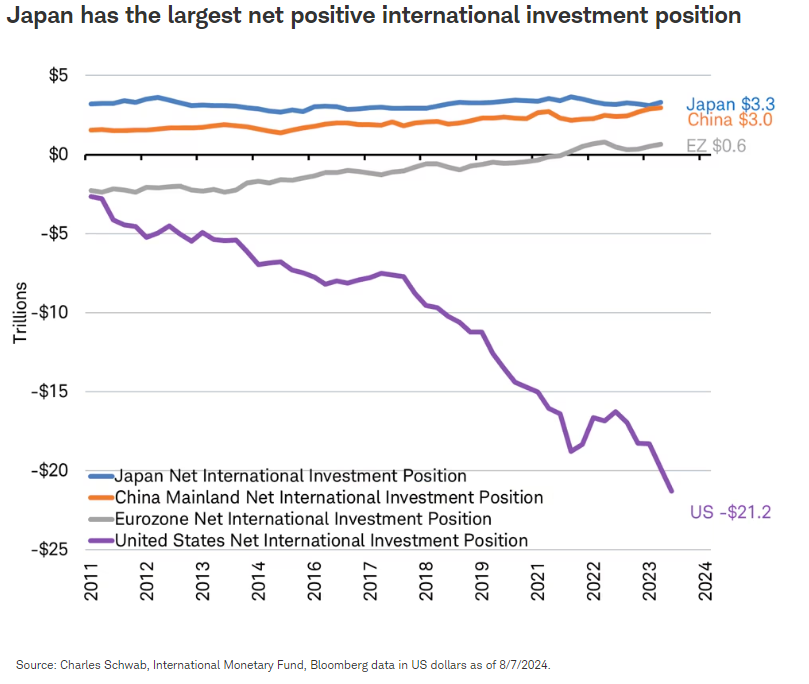

- Long-term: For the longer-term carry trade size, we look to Japan's long-term net investment position. Japanese investors are the biggest non-U.S. investors in U.S. Treasuries and among the top five in ownership of non-Japanese stocks. According to the International Monetary Fund, decades of current account surpluses have accumulated, giving Japan the world's largest net international investment position with $3.3 trillion of investments held abroad as of March 31, 2024. The potential for a reversal of more than a decade of outward flow of capital may be felt by investors worldwide. It is unlikely all of the outbound investment from Japan will reverse given the scope of investment opportunities outside of Japan, yet the size of the position suggests the potential for a trillion or more in capital might be repatriated to Japan over the coming quarters.

The global stock market sell-off of August 5th saw a turnaround the next day with when markets rebounded, but the recovery doesn't guarantee the risk has been eliminated. We believe that the most dramatic moves tied to the unwinding of the short-term yen trade may have passed, yet the unwind could remain a market drag and prompt more volatility over the medium and longer-term. The markets' panicky moves offer a reminder about how portfolio diversification and a review of risk-exposures is prudent.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. All expressions of opinion are subject to changes without notice in reaction to shifting market, economic, and geopolitical conditions.

Data herein is obtained from what are considered reliable sources; however, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Currency trading is speculative, volatile and not suitable for all investors.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0824-KWVY

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All