Are we in a recession? That's a question only the National Bureau of Economic Research (NBER), the official arbiter of recessions, can answer. However, investor concern has risen.

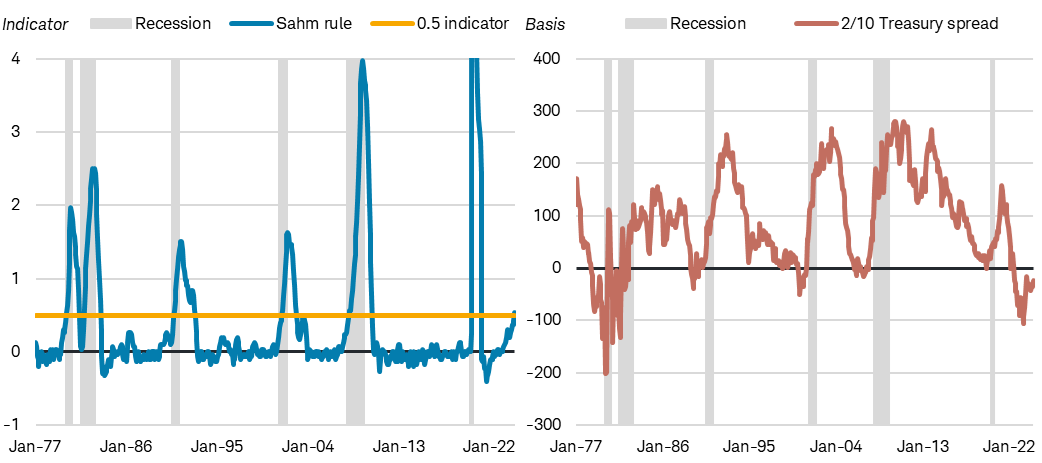

There have been two notable signals that the economy may be on the cusp of a recession:

- the re-steepening of the yield curve, which historically steepens prior to the onset of a recession, led by falling short-term rates as the Federal Reserve cuts rates in an attempt to spur the economy.

- and the triggering of the "Sahm rule," created by economist Claudia Sahm, which states that when the three-month average of the U.S. unemployment rate rises by at least a half-percentage point above its low during the previous 12 months, the economy is likely in recession. The Sahm rule was triggered by the July U.S. jobs report.

Both the Sahm rule and steepening of the yield curve are signaling a recession

Source: Bloomberg. Monthly data as of 7/31/2024.

Past performance is no guarantee of future results. United States Sahm Rule Recession Indicator Current (SAHMRLCR Index) and Market Matrix US Sell 2-Year & Buy 10-Year Bond Yield Spread (USYC2Y10 Index).

Although there are signs that are flashing recession, we think it's too early to declare that the economy is in a recession. However, the risk is elevated and for investors who are concerned about a recession, municipal bonds may provide some shelter.

Municipal bonds are bonds that are issued by cities, states, and local governments and often pay interest payments that are exempt from federal and potentially state income taxes. They usually have lower yields than bonds like Treasuries or corporate bonds, all else being equal, to account for the tax benefits. As a result of the tax benefits that munis offer, they can be an attractive conservative investment option for investors in higher tax brackets.

Here are five reasons why we believe that munis may provide some shelter if a recession hits.

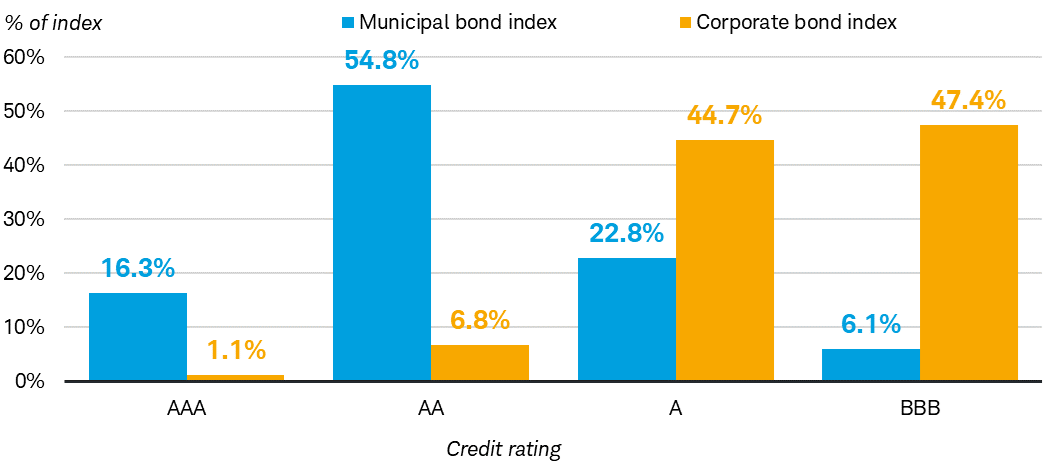

1. Most are very high credit quality to begin with, which can buffer the impact of a recession. On average, most states and local governments have strong finances and stable revenues. This is reflected in a high credit rating. Roughly seven out of 10 bonds in the Bloomberg Municipal Bond Index, a broad index of munis, are rated either AAA/Aaa or AA/Aa, which are the top two rungs of credit quality.1 Higher-rated issuers, on average are less likely to miss a scheduled interest or principal payment. This differs from other fixed income markets like the corporate bond market where most corporate bonds in the index are either A/A or BBB/Baa rated.

Most municipal bonds are either AAA or AA rated

Source: Composition of the Bloomberg Municipal Bond Index and the Bloomberg U.S. Corporate Bond Index as of 8/16/2024.

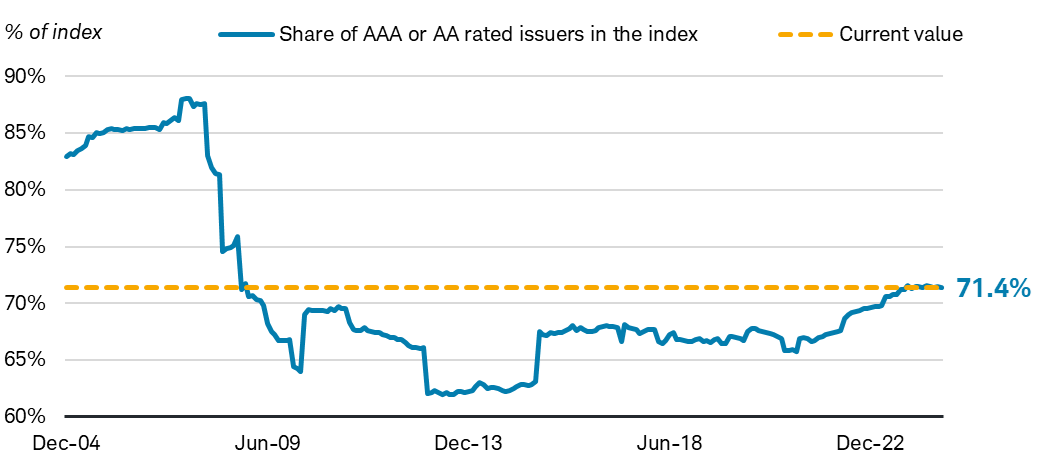

Municipal bonds historically have been very highly rated but recently the average credit quality of the market has improved. The proportion of AAA/Aaa or AA/Aa munis in the index was roughly 62% in 2013 but has since climbed to 71.4%—which is the highest proportion since the 2007-2008 credit crisis. The high average credit quality historically has led to very few defaults in the muni market. In fact, on average, only nine out of 10,000 investment-grade munis defaulted per year over a 10-year period.2

The share of highly rated munis in the index is the highest since 2009

Source: Composition of the Bloomberg Municipal Bond Index. Monthly data as of 7/31/2024.

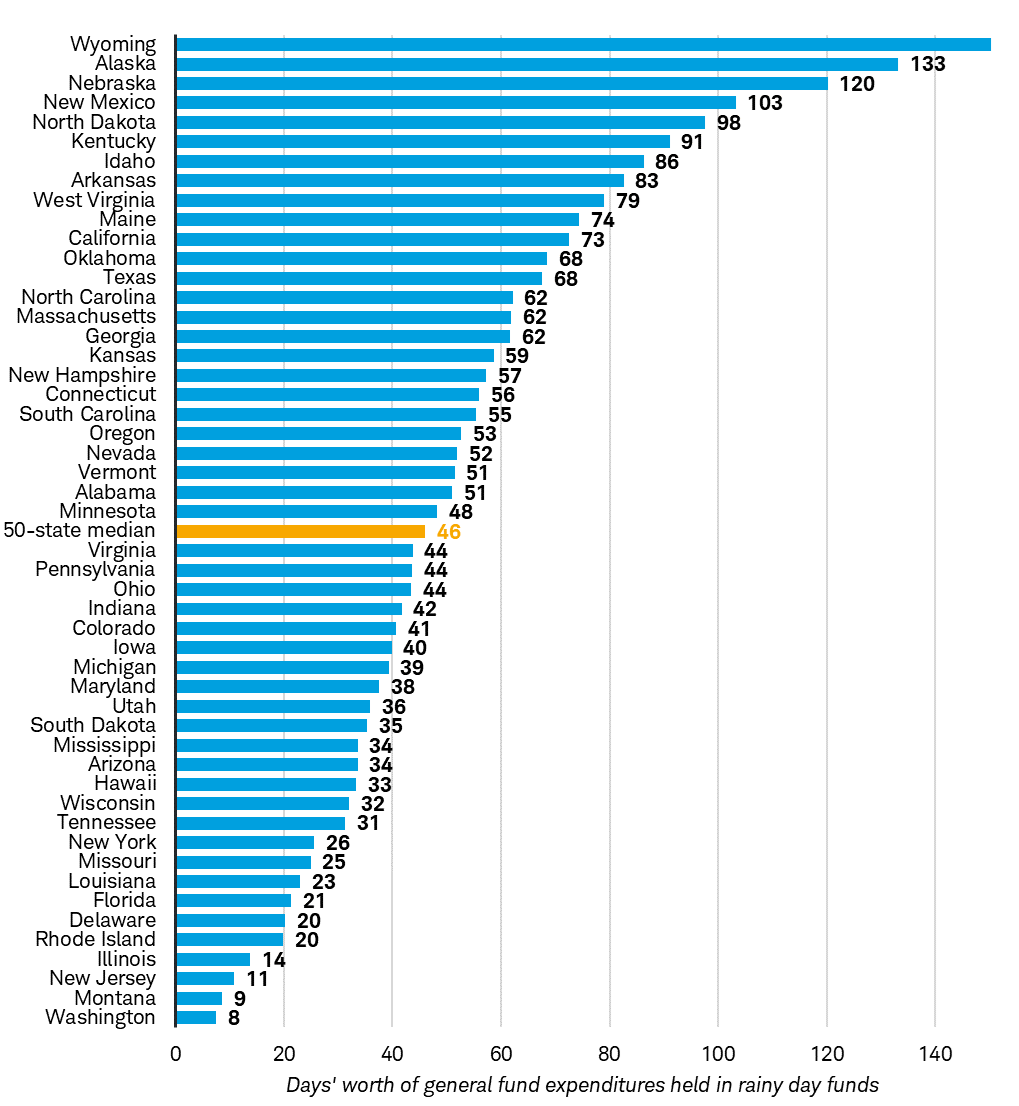

2. States have been building up their savings, which they can tap into if there's a slowdown in revenues. Most states have a rainy-day fund, which is akin to a savings account, that they can tap into if necessary. Almost all states operate with a balanced-budget requirement, which means that annually, they have to ensure that revenues meet expenses. This is unlike the federal government, which can run a deficit. If revenues aren't enough to meet expenses, states either have to cut expenses, raise revenues like taxes, tap into their rainy-day funds, or take other budgetary measures.

Over the past few years, most states have built up their rainy day funds. Rainy-day funds reached a record high in 38 states at the end of fiscal year 2023, according to The Pew Charitable Trusts. In fact, Pew estimates that the average state could operate for roughly a month and a half on savings alone. Pew also estimates that 19 states reached a record of the number of days they could operate on savings alone largely due to tightening spending.

Most states have strong rainy-day fund balances, in our view

Source: The Pew Charitable Trusts, FY 2023 Estimated.

Report published on 12/7/2023. X-axis truncated at 150 days for visual purposes. Wyoming is 306.6 days.

3. Revenues historically have declined later after a recession starts. Many municipalities have revenue sources that lag or are mostly isolated from economic activity. For example, the bedrock of local governments' finances are typically property revenues. Taxes are usually based on the assessed value of the property which typically lags the market value. Additionally, most states rely on income taxes as their primary source of revenue, which are often based on the prior year's incomes. Finally, some issuers, like water utility districts, have revenues that are essential services. Even if a recession hits, it's likely that most property owners will prioritize paying their water bill over other expenses.

Because of the way most state and local governments' revenues are constructed, it has resulted in tax revenues declining usually long after the recession has already started. For example, tax revenues held up during the first few years of the 2007-2008 recession. Revenues didn't start substantially declining until 2010. This long lead time gives state and local governments ample planning time to adjust expenses.

Revenues have generally fallen long after a recession has started

Source: US Census State Tax Collections, Quarterly data as of 3/31/2024.

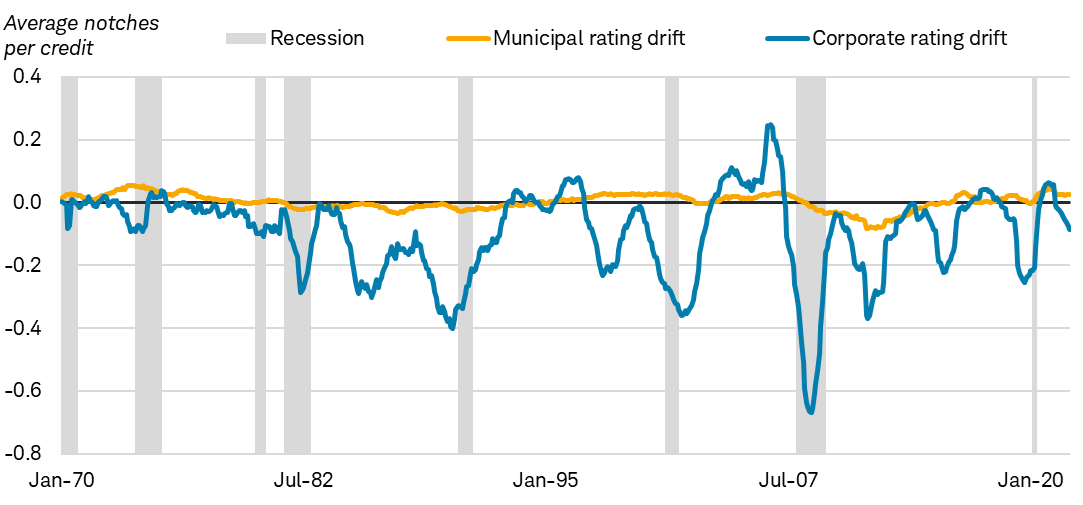

4. Ratings have been stable in past recessions. As a result of generally stable revenue sources and other factors, munis tend to be downgraded less frequently than corporate bonds, which tend to have more volatile revenue streams. This is especially true when a recession occurs.

As illustrated in the chart below, ratings drift is much more volatile for corporate bonds compared to munis. Ratings drift is the average change in credit-rating "notches" for every 100 bonds over the observed one-year period. One "notch," for example, is the incremental difference between AA+ and AA. In other words, in September 2008, the average corporate bond was downgraded 0.7 notches while the average municipal bond's rating was essentially unchanged. This is important because when a bond is downgraded or the market anticipates it may be downgraded, it usually falls in price.

Historically, muni ratings haven't been as volatile as corporate ratings

Source: Moody's Investor Services, as of July 19, 2023, which is the most recent date the data is available.

Past performance is no guarantee of future results. For illustrative purposes only.

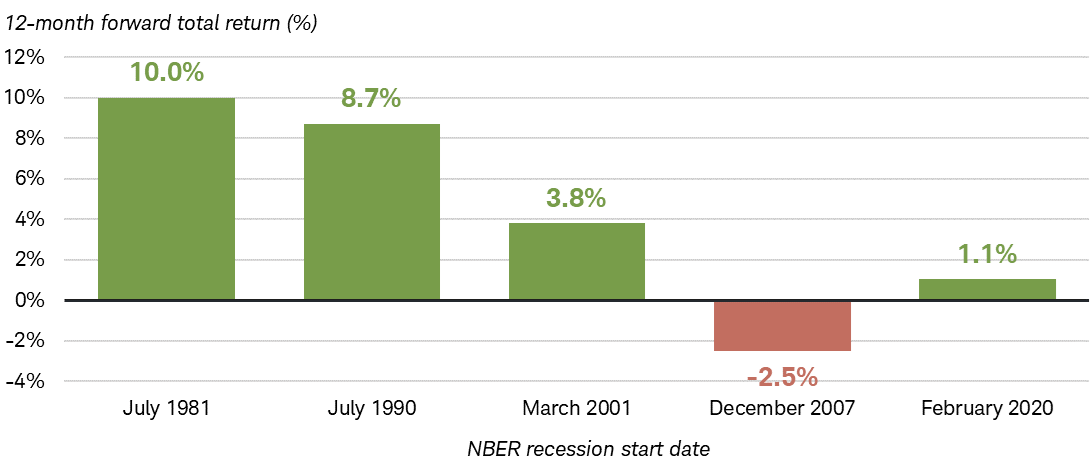

5. Performance is generally positive following the onset of a recession. Longer-term bonds tend to track the direction of inflation and the economy. A recession, by definition, is a sustained period of economic decline, which historically has translated to yields for longer-term bonds falling. In four of the past five recessions, municipal bonds have posted positive total returns over the 12 months following the start of the recession. Only in the 2007-2009 recession did munis post a negative return in the 12 months after the start of the recession.

In four of the past five recessions, munis have posted positive total returns over the subsequent 12 months

Source: Bloomberg, as of 8/16/2024.

12-month forward total return of the Bloomberg Municipal Bond Index. Past performance is no guarantee of future results. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly.

Munis posted positive total returns during the 1990 and 2001 recessions because yields were already moving lower and continued to move lower as investors sought less-volatile investments, like bonds. The 1981 and 2020 recessions were relatively unique. The 1981 recession was characterized by the Federal Reserve aggressively hiking interest rates to squash record-high inflation. The 1981 recession officially started in July of that year when the yield on a broad index of munis was 11.4%. The very high starting yield translated to a very strong performance in that period. The 2020 recession was unique in the sense that at no other time in modern history has a global pandemic caused the entire U.S. economy to come to a screeching halt. It's worth noting that each economic slowdown is unique, and history may not repeat itself when the next recession occurs.

What to consider now

Historically, municipal bonds have been a respite from an economic slowdown. The long lead time between the start of a recession and revenues slowing gives issuers ample opportunity to prepare. This has resulted in fewer ratings changes and defaults relative to corporate bonds. For help selecting the right investment options given your situation, reach out to your Schwab representative.

1 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

2 Source: Moody's Investor Services, as of July 19, 2023, which is the most recent date the data is available. 10-year cumulative default rate for munis rated in the investment-grade category by Moody's. Past performance is no guarantee of future results.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Supporting documentation for any claims or statistical information is available upon request.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and the Schwab Center for Financial Research does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

All issuer names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or 'Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0824-LW9H

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab