Chinese companies are being encouraged to return cash to shareholders—and are finding good reasons to do so. This marks a big shift for the market and could unlock attractive return potential for equity investors who become familiar with the forces that are driving increased dividend payouts.

The evolution of China’s equity market is in full swing. Regulators are encouraging companies to focus on shareholder returns. And changing macroeconomic conditions are making it easier for Chinese companies to pay dividends. Taken together, we believe these two trends are paving the way for a new phase in which Chinese dividend payers will be rewarded by the market, creating a virtuous cycle for investors.

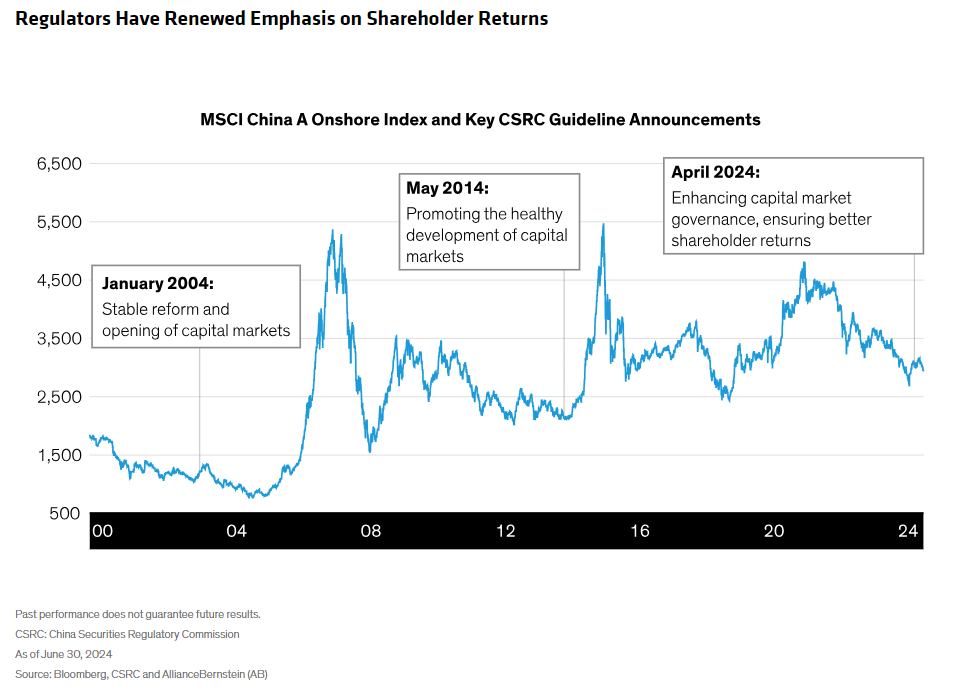

The Nine-Point Guideline: A Catalyst for Change

Dividends have been elevated on the public agenda by regulatory directives released in April. These policies, known as the nine-point guidelines, followed similar moves in 2004 and 2014, which shaped China’s modern A-share market. In 2014, the guidelines sparked a boom in initial public offerings (IPOs) for fast-growing companies and an increase in the number of listed companies that established the public equity market as a key source of capital for the economy (Display).

The new guidelines offer three main policy focuses: enhancing capital market oversight and governance; improving the quality of listed companies by setting higher IPO standards, implementing stricter de-listing processes and ensuring better shareholder returns; and boosting investor protection through more transparent disciplinary measures, improved disclosure and increased representation of long-term institutional capital in A-shares.

These guidelines are similar to those typically issued by regulators in other markets, such as Japan and South Korea. In our view, this indicates that the Chinese market is continuing to mature.

Of course, China’s market has its own unique features. Still, we think Chinese companies are likely to respond positively to the dividend directives. In part, that’s because the regulations aim to encourage state-owned enterprises (SOEs) to direct payouts to their government shareholders at a time when the macroeconomic slowdown is straining fiscal coffers.

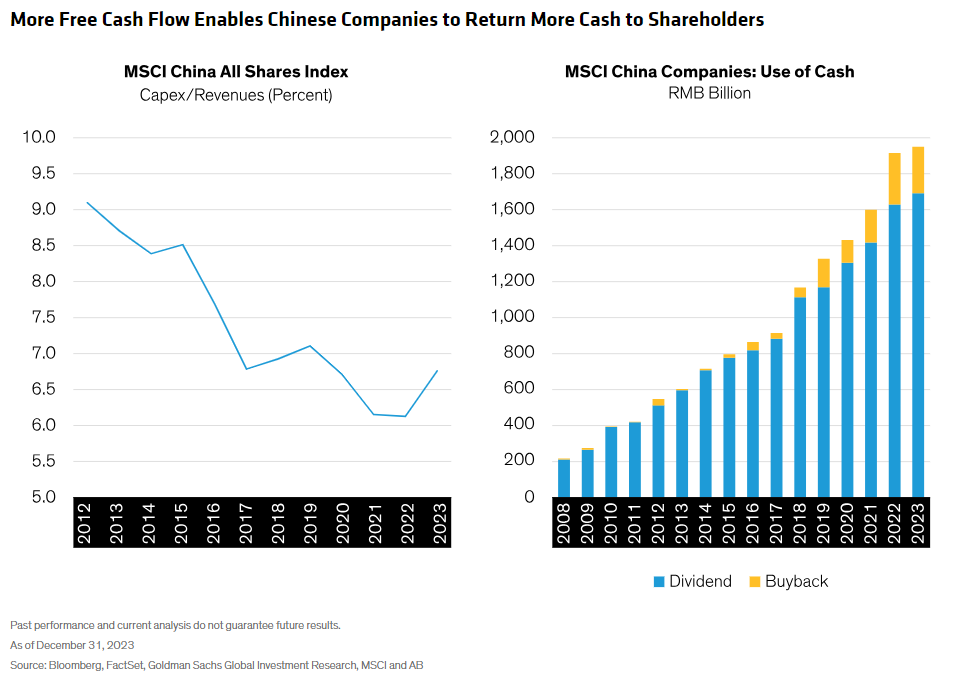

Companies Are Able to Pay More Dividends

Regulatory change comes at an opportune moment. Chinese companies, which have historically paid much lower dividends than Western peers, are much better placed to boost payouts to shareholders than in the past.

Rewind to 2000, when China joined the World Trade Organization. At the time, Chinese companies were growing rapidly, driven by an aggressive expansion model focused on increasing capacity as quickly as possible. As voracious consumers of capital, Chinese companies issued large amounts of stock and debt to fund extensive capital expenditure budgets for building more factories and facilities. In this high-octane growth environment, companies didn’t have much excess cash to reward shareholders.

Yet as the economy matures and growth slows, demand for capital expenditure has decreased. Well-managed companies are now able to return excess capital to shareholders because declining capital investment (Display) frees up cash for dividends and buybacks, which have risen steadily in recent years.

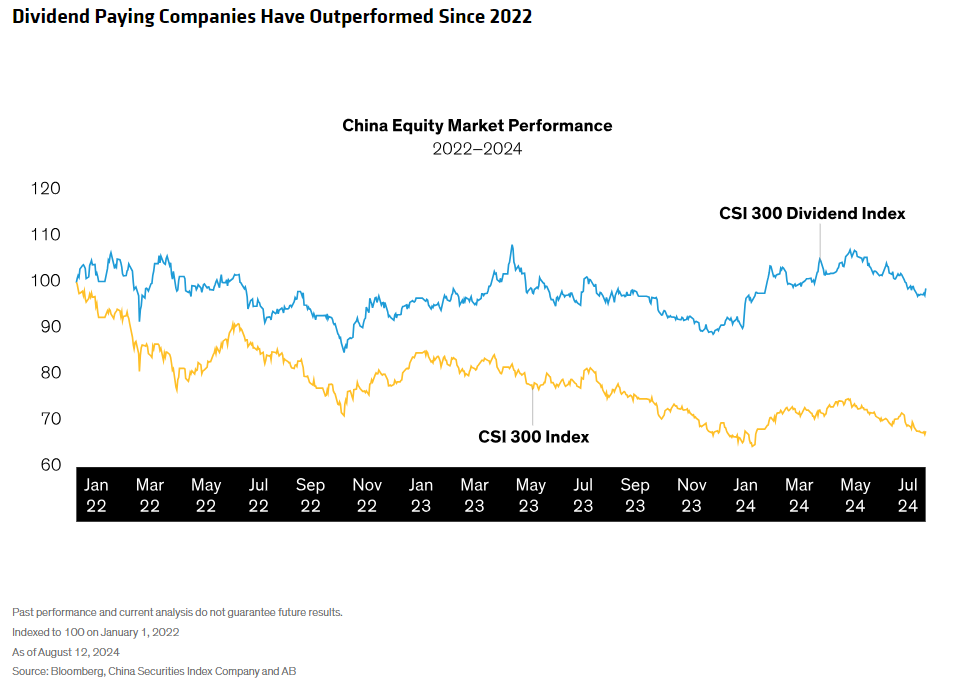

Will Markets Reward Dividend Payers?

Meanwhile, we’re seeing evidence that dividend-paying companies are being rewarded by the market. Over the past two years, the CSI 300 Dividend Index, comprised of high-dividend-paying Chinese companies, has outperformed the broad CSI 300 Index by a wide margin (Display).

This trend also helps explain why Chinese value stocks have outperformed growth stocks. Since early 2022, the MSCI China A-share Value Index, which has a higher cohort of dividend payers, has outperformed the MSCI China A-share Growth Index by 38%.

Potential Hurdles to Progress

To be sure, regulatory attitudes can change quickly in China. If the government’s objectives or focus were to shift elsewhere, the trend toward dividends could be affected.

The weakening economy is another potential hurdle. While most large-cap companies have managed to sustain revenues and margins despite the sluggish economic backdrop, dividends ultimately are derived from profits. If economic growth were to decelerate further, companies would face a squeeze on earnings and profit margins that could constrain dividends.

Identifying Opportunities in Dividend Stocks

Given the risks, we think an active investing approach is especially important when investing in high-dividend Chinese stocks. Investors should focus on the following types of companies.

First, look for SOEs that are responding positively to the guidelines. From our discussions with SOE management teams, we’ve learned that large companies directly controlled by the central government have been most responsive; many already have plans to boost their dividend payouts. In contrast, smaller, locally controlled SOEs have been less proactive; many are adopting a wait-and-see approach to managing their balance sheets before boosting payouts to shareholders.

Second, focus on companies with high-quality business attributes. Large-cap stocks like these are in the sweet spot for dividend stocks with potential upside thanks to ample free cash flows and the potential for increased payouts.

Third, focus on sectors that offer supportive features for payouts. We see opportunities in industrials, including operators of toll roads, ports and other infrastructure assets. The energy and commodities sectors also offer attractive dividend potential. In these areas, large, established national champions benefit from steady cash flows supported by their national oligopolistic positions.

These types of businesses are more prominent among value-oriented companies, which haven’t typically been favored by international investors in Chinese equity markets. As more companies discover dividends, value stocks of cash-generating businesses could help investors gain access to new return streams powered by the ongoing transition of China’s economy.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

© AllianceBernstein

Read more commentaries by AllianceBernstein