With high-yield credit spreads hovering near all-time lows, some investors may be tempted to sit on the sidelines until spreads have widened before investing. We think that could be a mistake. In fact, we see a compelling case for investing in the high-yield market today, despite narrow spreads. Here’s why.

1. Spreads Are Tight Because of Good News

The biggest reason that spreads are so narrow today is that economic news has been good. Sustained economic growth has made the possibility of recession seem more remote. Strong fundamentals also play a role, as companies have fortified their balance sheets and locked in lower interest expenses in the years since the COVID-19 pandemic. As a result, defaults have been modest, running below their historical averages—and below Street expectations.

Meanwhile, attractive yields have stoked demand in the global high-yield market as investors try to capitalize on higher potential returns and lower perceived risks. By contrast, on the supply front, companies have focused more on reducing debt than on using it for growth or acquisitions. As a result, demand has been outstripping supply, creating a favorable technical backdrop that supports prices and keeps spreads tight.

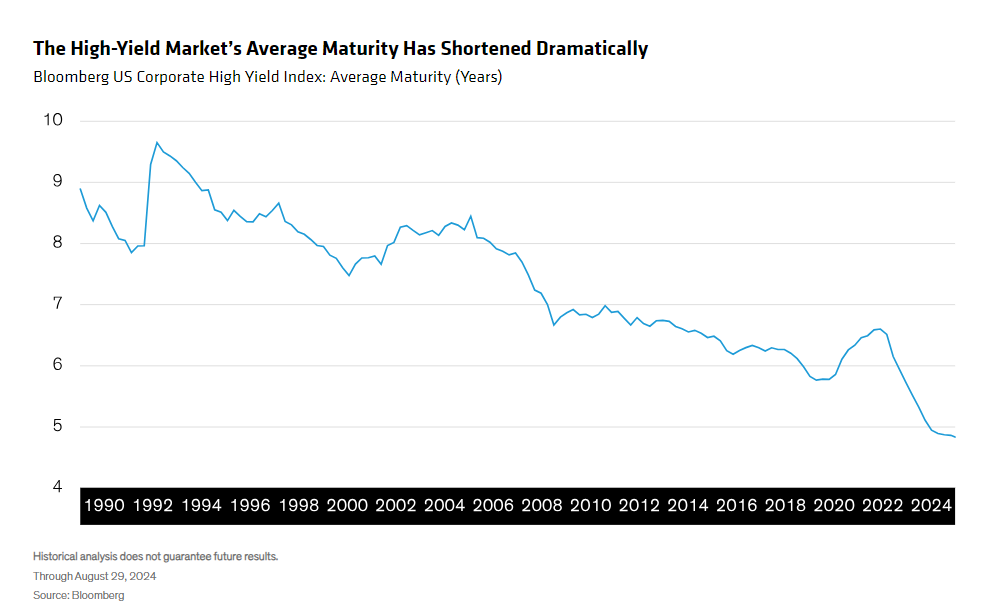

Debt reduction has also caused the average maturity of the Bloomberg US Corporate High Yield Index to shorten to record lows (Display). Consequently, both the index’s average duration and its “spread duration”—the sector’s price sensitivity to changes in spread levels—are below historical averages.

2. Tight Spreads Have Tended to Be “Sticky”

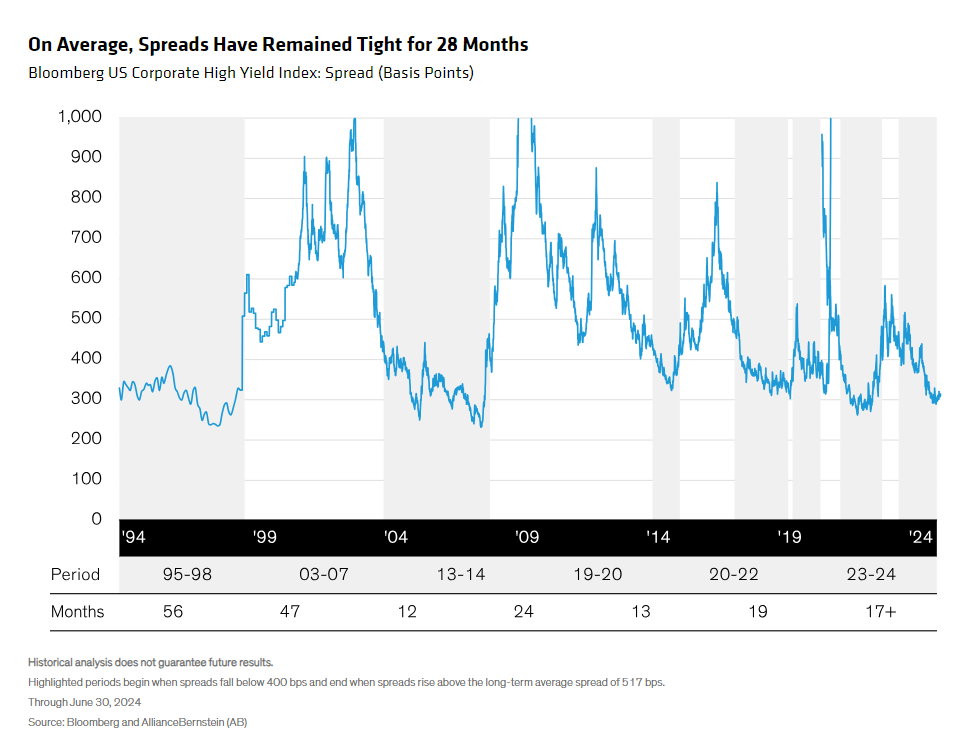

If history is a guide, high-yield spreads could stay in their current range for some time. Since the mid-90s, tight spreads have remained tight for more than two years, on average (Display).

That’s a long time for sidelined investors to pass up attractive income and return potential. Even a patient investor may find they’ve waited for nothing. (And on those occasions when spreads do blow out, not many investors feel comfortable adding risk when spreads are exceptionally wide, indicating a risk-off environment.)

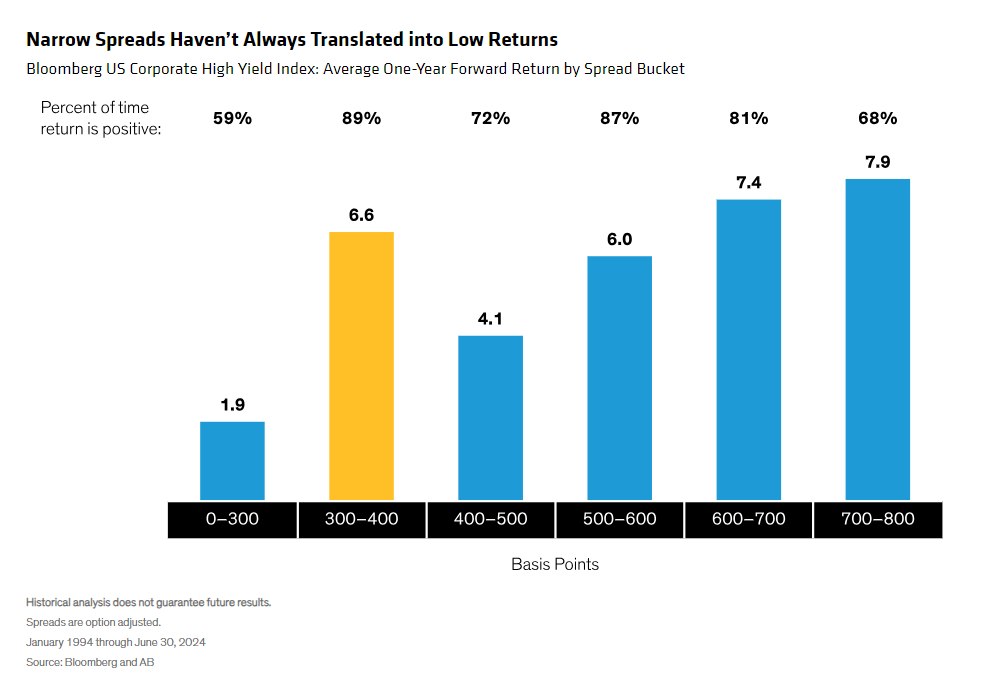

Further, since 1994, when spreads ranged between 300 and 400 basis points, ensuing returns were strong, averaging roughly 6.6% (Display). In our analysis, that’s because macro factors and overall yield levels hold more sway than spreads.

3. Yields Are Compellingly High

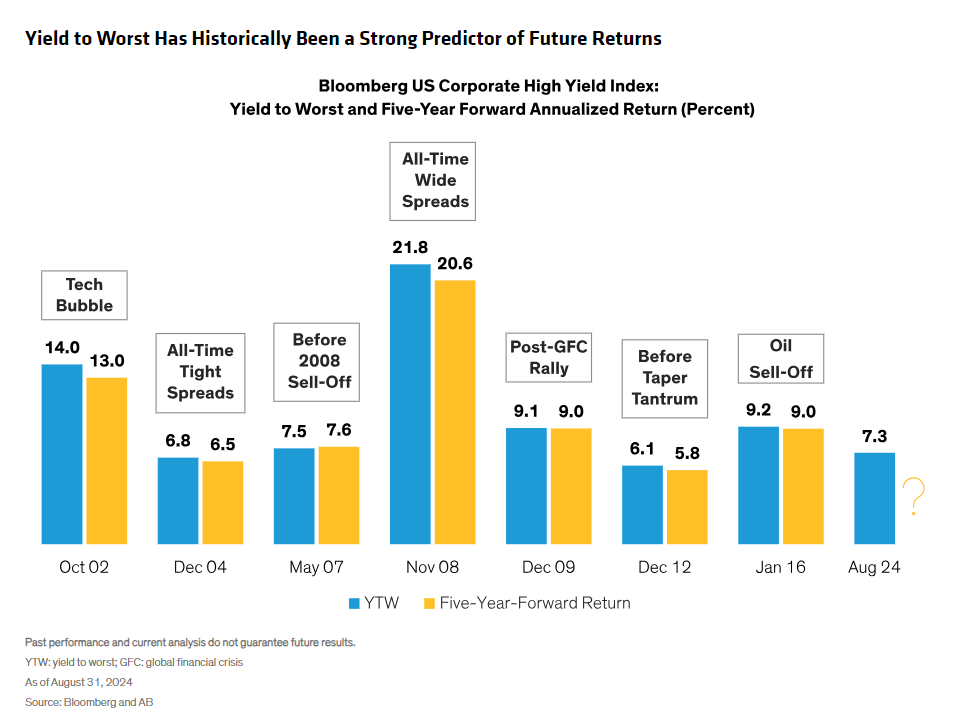

While spreads are relatively low, yields on high-yield bonds are higher than they’ve been in years. And historically, yield has been a much better predictor of return than spread has been. History shows that the sector’s yield to worst has been an excellent proxy for return over the next three to five years, in all kinds of markets (Display). With today’s yield to worst at 7.3%, the potential return appears sizable.

When It Comes to Risk, Context Matters

Some investors may nonetheless be leery of potential spread widening. Because spread widening typically occurs during market corrections and in risk-off environments, it’s important to consider risk-taking in the context of the larger portfolio. That’s especially the case for investors who are overweight equities but underweight credit.

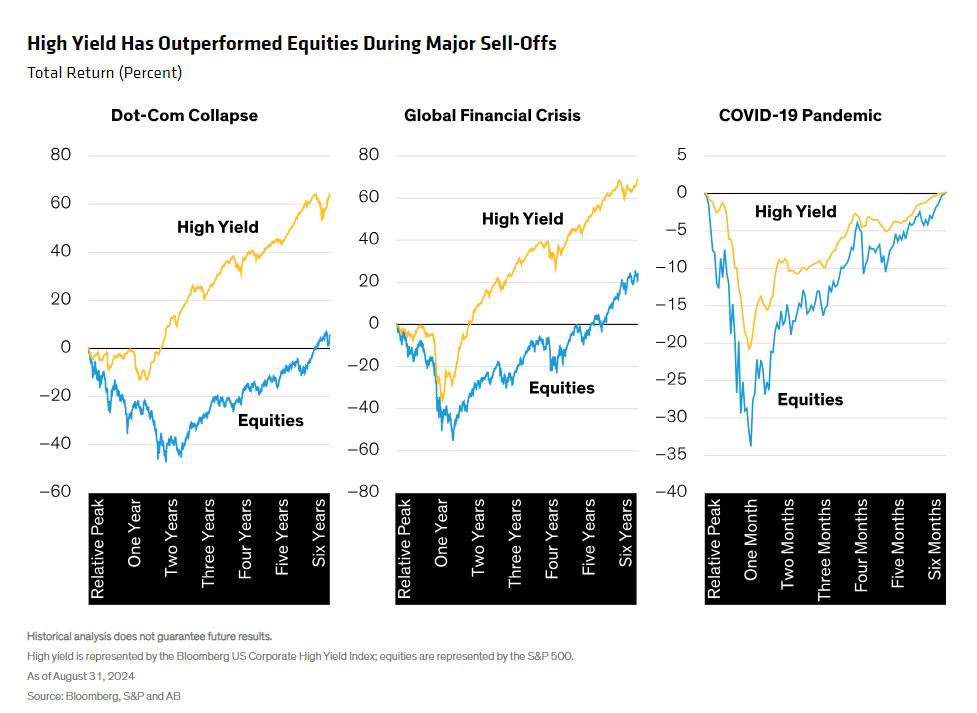

Historically, high yield has delivered equity-like returns with roughly half the volatility. During major sell-offs such as the dot-com crash, the global financial crisis and the COVID-19 pandemic, equity returns declined more sharply than high-yield returns, and high-yield recovered more quickly (Display). In our view, that makes high-yield bonds a prudent substitute for a portion of an equity allocation.

Of course, spreads may move in either direction, not just wider. Though GDP growth is slowing, we continue to view a recession as unlikely, given the economy’s underlying strength coming into the policy cycle. If the Federal Reserve successfully avoids a recession, it’s possible that spreads could tighten even further, giving a near-term boost to the high-yield market.

Regardless, positive economic news, strong fundamentals, sticky spread trends and compelling yield levels make it, in our view, worth giving a green light to investing in high yield today.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein