As the Federal Reserve joins the rate cut party, global growth may begin to see the boost investors have been waiting for.

Rate cuts point to better growth ahead

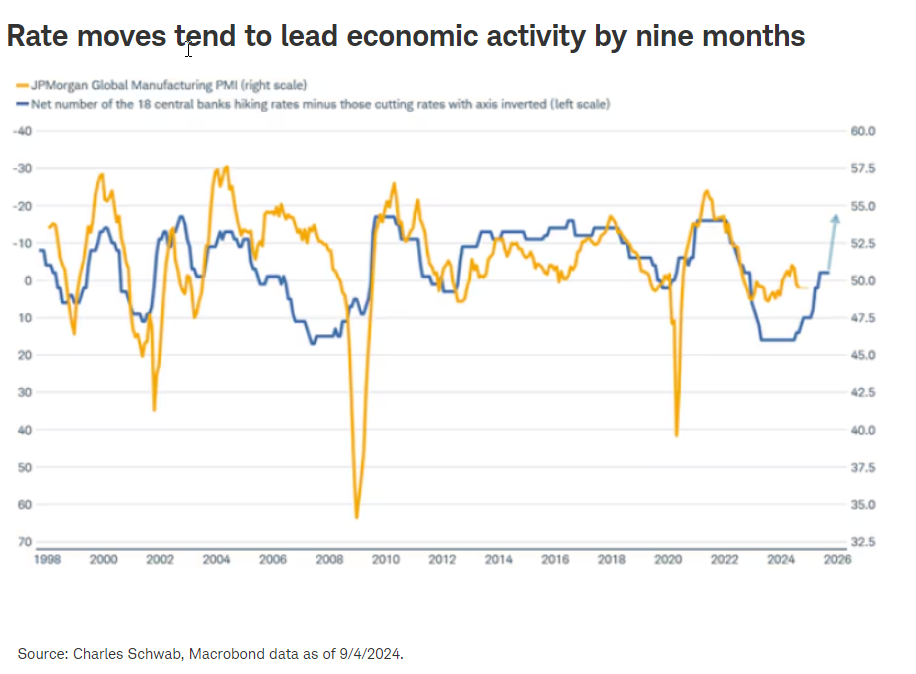

The Federal Reserve may be gearing up for its first interest-rate cut of the cycle, but the European Central Bank, the Bank of Canada, Bank of England, among other advanced economy central banks have already begun to reduce rates. In fact, just over half of the world's central banks in advanced economies as defined by the International Monetary Fund have already started to cut rates. An index of central-bank rate cuts that measures the net number of advanced central banks changing rates leads the global manufacturing Purchasing Managers' Index (PMI) by about nine months, as you can see in the chart below. The arrow points to the most likely shift to cuts by nearly all of the 18 advanced central banks over the coming months as the United States, Australia, Norway, South Korea and a few others are likely to join the 11 who have already cut rates.

18 advanced central banks include: Australia, Canada, Czech Republic, Denmark, Eurozone, Hong Kong, Hungary, Iceland, Israel, Japan, New Zealand, Norway, South Korea, Sweden, Switzerland, Taiwan, United Kingdom, and United States.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Historically, the manufacturing PMI has been a good proxy for global growth for both output and corporate earnings. Manufacturing tends to be more cyclical, and therefore leads changes in the overall economy. If history unfolds similarly, rate cuts could help to lift economic growth as represented by the global manufacturing PMI from around 50 to near 55 by mid-2025. Let's examine what it might mean for stocks and stock market leadership.

What might stocks do?

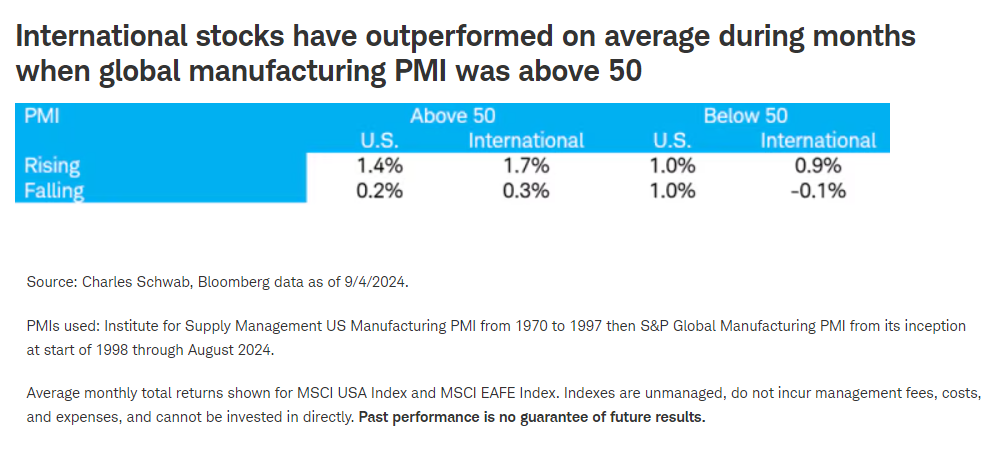

When the global manufacturing PMI is above 50 and rising, as the chart above suggests it may be in the coming months, stocks have posted the strongest average monthly returns. The average monthly total return of the MSCI World Index has been 1.4% (18% when annualized) during similar periods. When the PMI was below 50 and rising the monthly return averaged 0.8% (10% annualized) and the stock market was effectively flat on average when the PMI was falling.

When the global manufacturing PMI is above 50 and rising, international stocks have posted stronger average monthly returns than U.S. stocks. Unsurprisingly, when the PMI is above 50 international stocks have outperformed U.S. stocks whether the PMI was rising or falling and international stocks underperformed when the PMI was below 50, especially when it was falling, as you can see in the chart below. The makeup of the U.S. stock market has tended to be less economically sensitive than the market of non-U.S. stocks. The MSCI EAFE Index of developed international stocks has much higher weightings in economically sensitive sectors like Financials, Energy, and Materials. Should the PMI rise from around 50 over the coming months as suggested by the historical relationship with central bank rate cuts, international stocks may lead the market.

Currency boost?

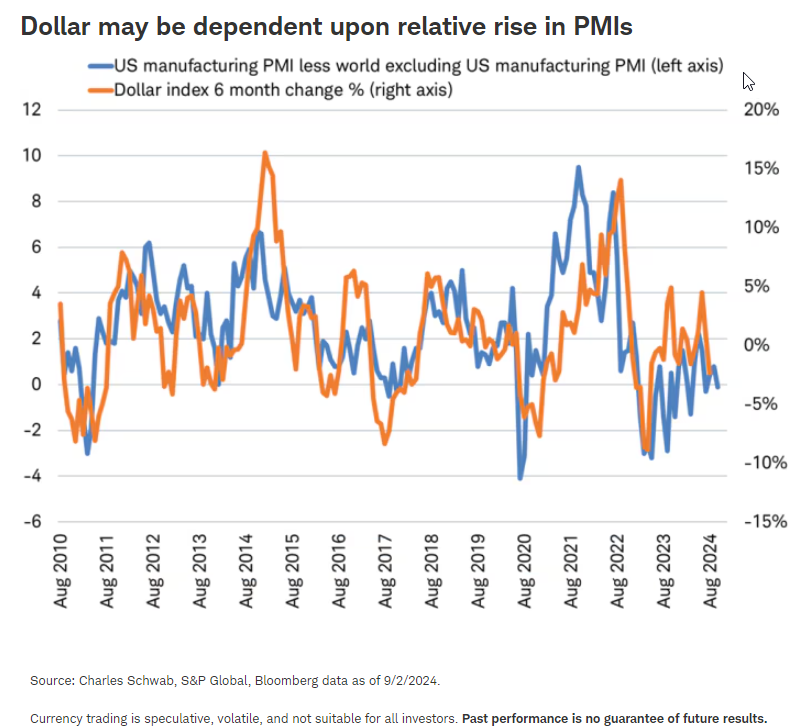

If the slower start to rate cuts by the Fed results in the U.S. manufacturing PMI rebounding from just below 50 more slowly than the non-U.S. PMI, then the dollar may slide relative to currencies like the euro and the pound. As the chart below shows, when the U.S. manufacturing PMI lags the rest of the world, the dollar tends to fall—as it has recently. This could act as another factor favoring non-U.S. stock market exposure in the months ahead.

International stocks have outperformed U.S. stocks so far during the third quarter. Should the global economy respond as it has in the past to global rate cuts, the historical lag between monetary policy stimulus and growth suggests a brighter outlook over the coming months and the potential for solid stock market returns and continued international stock market leadership.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

Currency trading is speculative, volatile, and not suitable for all investors.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0924-RLYB

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab