Many of the election campaigns around the world in 2024 featured a lot of bark but ending up taking little bite out of markets. Candidates often campaign on change, but there was little to follow the many elections of 2024. The major policy changes proposed by the winners during their campaigns saw little progress toward actual implementation, limiting their potential market impact. The lesson is that actual policy seems to be more often dictated by economic circumstances, rather than the proposals offered by policymakers.

Biggest election year in history

Voters in over 80 nations and territories representing more than half the world's population headed to the polls this year, making it the biggest election year in history. We observed a broad theme that emerged across these elections: Parties encouraging "my country first" nationalist policies that may restrict trade and touting fiscal deficit widening spending initiatives and tax cuts saw gains. While markets could respond negatively to trade frictions and wider deficits due to their potential negative impact on growth and inflation, in general, they haven't. To figure out why, we will examine the policies—rather than the proposals—of the new governments that followed elections this year in Taiwan, South Korea, the Netherlands, Mexico, India, European Union, United Kingdom, and France to see if there is a consistent message for investors to consider with the Japanese and U.S. elections just ahead.

Taiwan (January)

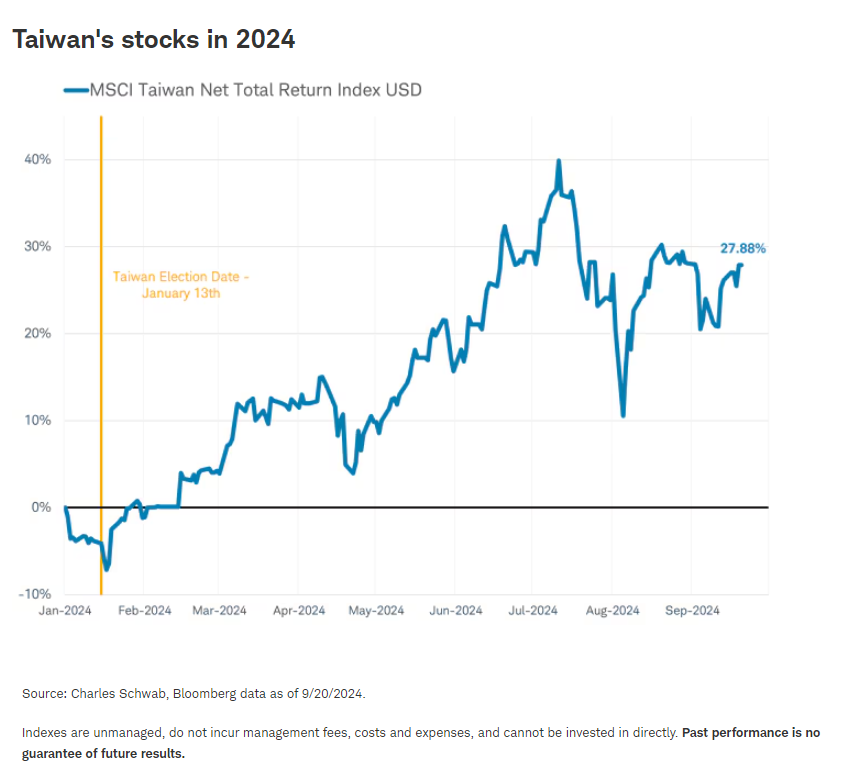

The first major election in 2024 was held in Taiwan, when voters didn't just choose their next president and legislature, they also helped set the course for U.S.-China relations over the next four years. Voters chose between a ruling party determined to maintain Taiwan's independence and an opposition that sees closer ties with China as Taiwan's only viable path.

Despite the win of the presidency by the pro-independence Democratic Progressive Party (DPP), the party did not see a decisive victory and lost its majority in the legislature. The outcome resulted in little change in policy with new President Lai Ching-te stressing he would support the cross-strait status quo with China. Shortly after Lai took office in May, Beijing halted tariff suspensions/discounts on 134 items listed under a trade deal with Taiwan. In September, the Chinese government announced it would scrap its additional tariff exemptions on 34 Taiwanese agricultural exports to China. Yet, these symbolic moves impacted only about 10% of the value of Taiwan's exports to China.

Taiwan's stocks delivered a nearly 30% total return so far this year, as measured by the MSCI Taiwan Index in U.S. dollars.

South Korea (April)

South Korea's opposition parties won 189 seats in the 300-seat National Assembly during the April 10 legislative elections. With the legislature now in the opposition's hands, President Yoon of the People Power Party will have little ability to enact policy changes. Sustainability of the pension system is one major policy issue due to South Korea's aging population. In August, the president proposed pension reforms that would raise wage earners' pension contribution, raise the qualifying age, and cut future benefits to delay the fund's depletion. The opposition-run legislature may propose a drastically different reform with more benefits, but neither proposal seems likely to pass.

The split control between the legislature and the presidency leads us to not expect significant changes on the issue of pension reform, or any other major policy initiatives that might impact markets. While South Korea's stock market has suffered losses this year, they can be attributed to the performance of Samsung and SK Hynix. These are the index's two biggest stocks, together accounting for over one-third of the MSCI Korea Index and have both plunged about 30% since July 11 on the early August global unwinding of the yen carry trade and declining global semiconductor sales for laptops and cell phones. The decline is not likely tied to any changes in domestic policy.

Mexico (June)

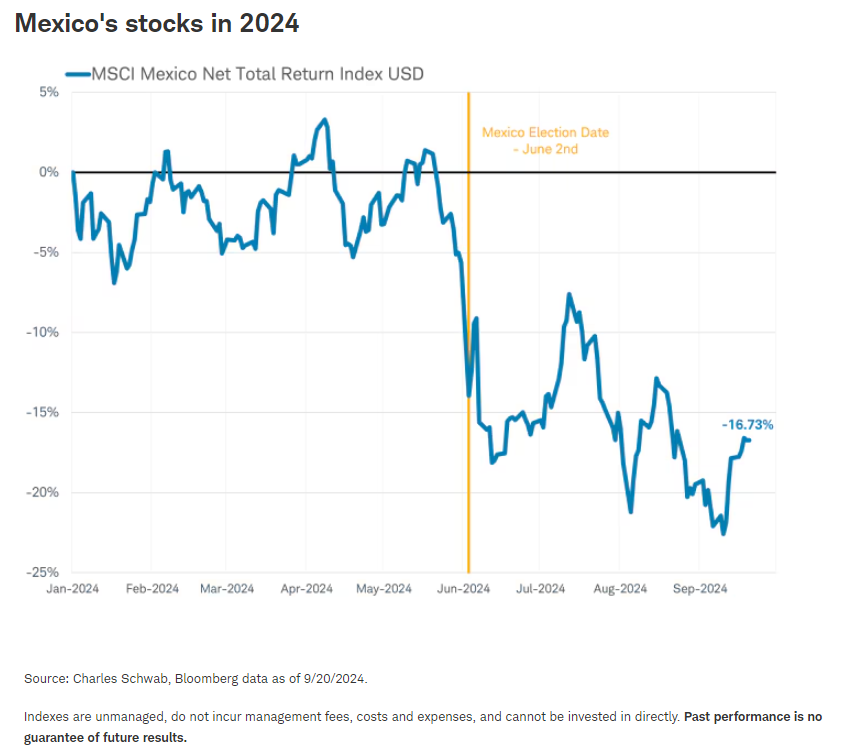

After her inauguration on October 1, President-elect Sheinbaum will have a stronger mandate than outgoing President Obrador received in 2018, having won more than 60% of the popular vote on June 2. Moreover, her party's alliance with the Labor and Green Parties has resulted in a large supermajority in the lower house amounting to 74% of the seats as well as securing 83 out of 128 seats in the Senate, just two votes shy of a two-thirds supermajority. Despite her power and populist bent, she has pledged fiscal austerity focused on bringing down the budget deficit to maximum of 3.5% in 2025. It has grown to 5.9% of GDP this year according to government sources, the highest rate since the 1980s, on her predecessor's social spending. In support of U.S.-Mexico trade, Sheinbaum met with U.S. Vice President Harris in mid-June 2024 to discuss shared priorities, including strengthening trade ties.

Sheinbaum's landslide win and populist policy proposals, including judicial reforms, seem to have originally spooked investors with the MSCI Mexico Index falling by -13% in the days following the election in U.S. dollars. But a month later, the index had recouped nearly all of those post-election losses. Since then, Mexican stocks have slumped again, with the timing aligned with the global yen carry trade unwinding rather than the domestic policy agenda.

Netherlands (June)

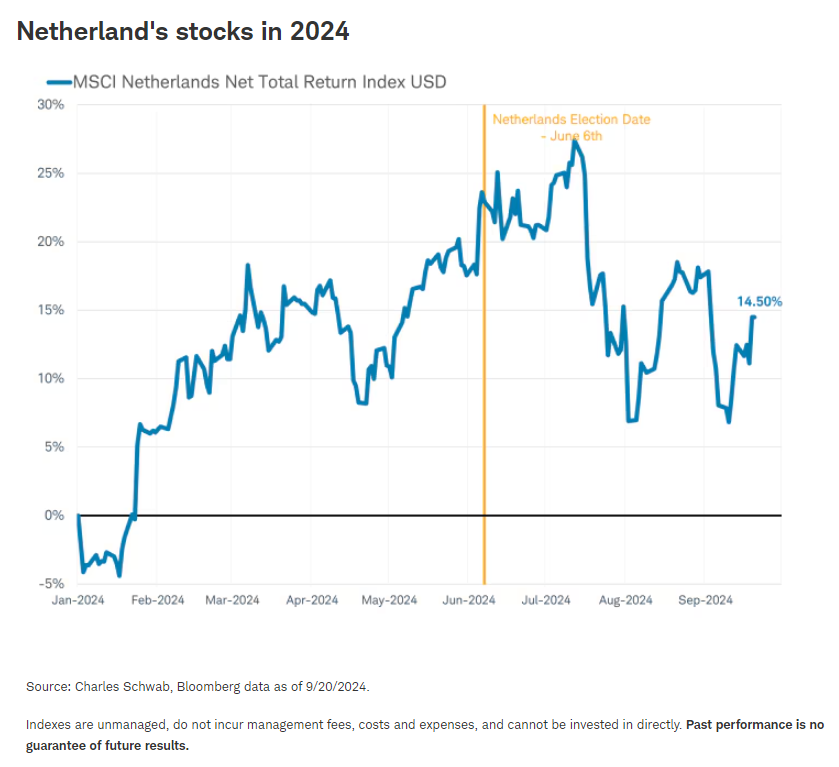

The new Dutch ruling coalition elected on June 6, which includes the far-right Freedom Party, the center-right People's Party for Freedom and Democracy, the center-right New Social Contract Party and the agrarian anti-establishment Farmer-Citizen Movement, has seemingly united around clamping down on immigration. Yet, the government consists of a diverse mix, with 18 political parties represented, making policy changes challenging. Beyond the challenges to domestical political alignment, any government plans to opt out from European Union migration rules would also require EU treaty changes approved by all 27 member nations.

Stocks in the Netherlands have produced a total return of 11% so far this year, as measured by the MSCI Netherlands Index in U.S. dollars. The index was dragged down recently by ASML Holdings, N.V., the maker of equipment used to produce Nvidia's artificial intelligence (A.I.) chips. This stock accounts for 40% of the MSCI Netherlands Index and has fallen since July 11th along with other global chip-related stocks.

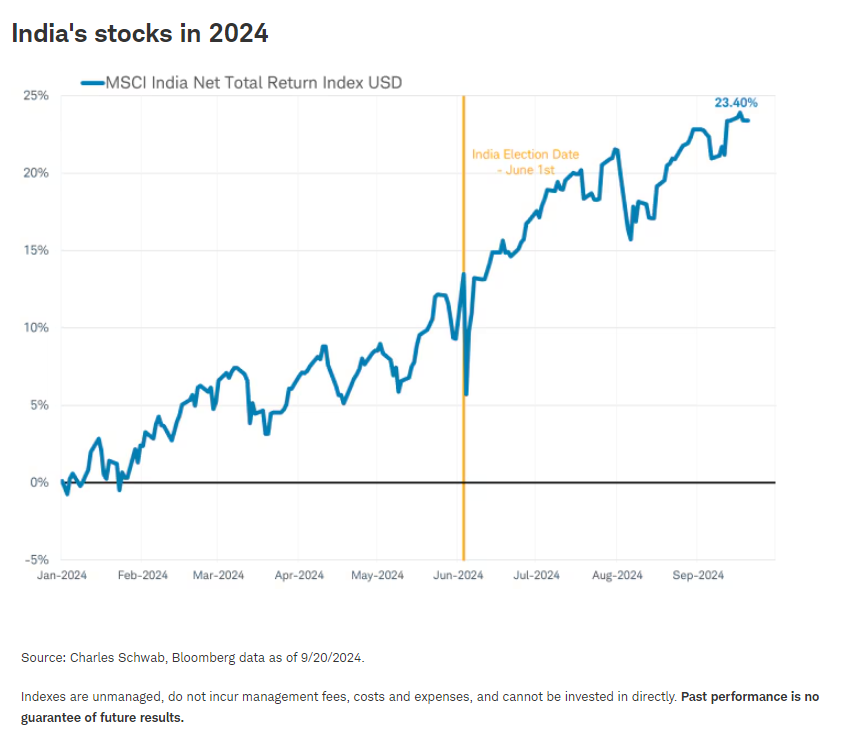

India (June)

In the world's biggest election, with more than 968 million people out of a population of 1.4 billion eligible to vote, the ruling Bharatiya Janata Party (BJP) unexpectedly failed to win an outright majority. After losing 60 seats, the party is reliant on its alliance partners to form a government. It was the party's worst electoral performance since it came to power in 2014 and seen as a big blow to Prime Minister Modi's leadership. The opposition parties campaigned on overtly populist policy platforms such as increasing social spending and implementing redistributive wealth taxes.

A tighter budget might imply a diversion of funds from investments in infrastructure, which have been critical to growing India's manufacturing base, toward more popular social handouts. But the first budget of the new coalition government revealed little change in policies; the budget featured a plan to reduce the deficit while maintaining healthy levels of infrastructure spending and added a component designed to boost job growth. With India's growth supporting policies intact despite the election outcome, the total return of the MSCI India Index is up 24% so far this year, as measured in U.S. dollars.

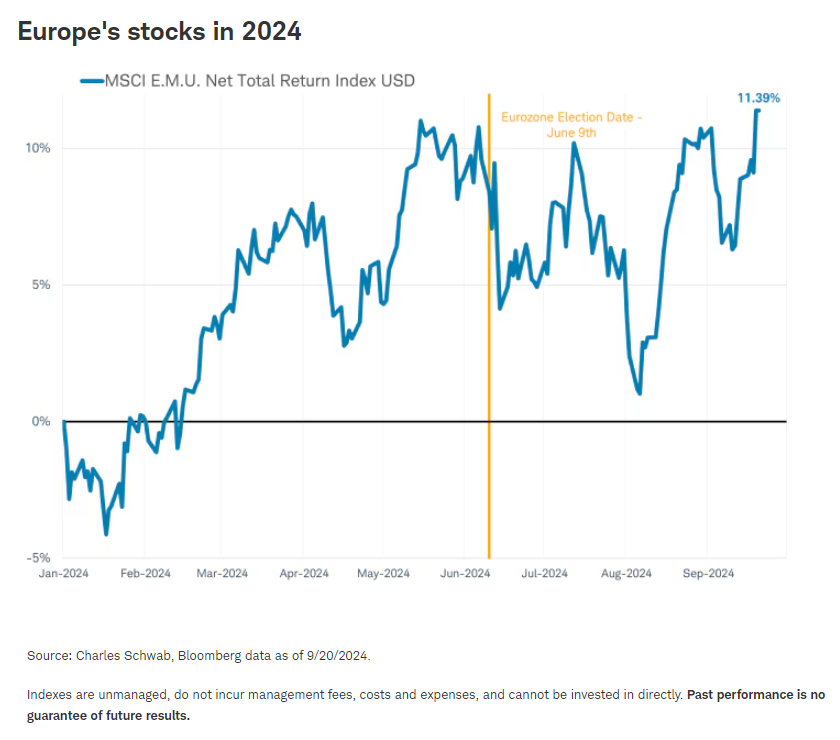

European Union (June)

The European Union (EU) elections on June 9 saw a rise by populist parties, with the coalition of the European People's Party and the Social Democrats losing their majority in Parliament for the first time. But rather than heralding sweeping changes, the election has resulted in a more fragmented legislature. This likely leads to a slower and more complex policymaking process.

The populists in the EU parliament are experiencing a challenge similar to what Italy's populist Prime Minister Meloni has encountered as she finishes her second year in office: How to fulfill generous campaign promises while shrinking bloated budgets. Figuring out how to pay for their pledges is especially complex in the EU; watchdogs in Brussels tend to keep a close eye on government spending, reining in any excessive deficits. In early September, the release of a long-awaited report by former European Central Bank President Draghi on the future of European competitiveness is expected to translate into proposals for industrial policy, regulatory reform, and spurring investment in technology, green energy infrastructure, and defense. But political and financial constraints are likely to limit how much the EU will be able to deliver on these targets.

On the one measure they seem to be united on, trade protections, the outcome still isn't assured. In July, the EU put in place provisional tariffs on Chinese-made electric vehicles as part of its ongoing investigation of alleged Chinese subsidies. A vote in November would be needed to make them permanent. Fearing Chinese retaliation, several EU countries (including Germany) oppose the tariffs with nearly a dozen abstaining from an advisory vote on the issue, which suggests many are undecided on the measure. They may be waiting to see China's reaction and the outcome of the U.S. election (and the potential prospect of increased U.S. tariffs on China's goods).

The MSCI EMU Index that tracks stocks in the European Monetary Union in U.S. dollars has seen a total return of 12% so far this year, showing little negative effect from the populist parties' increased presence in the legislature.

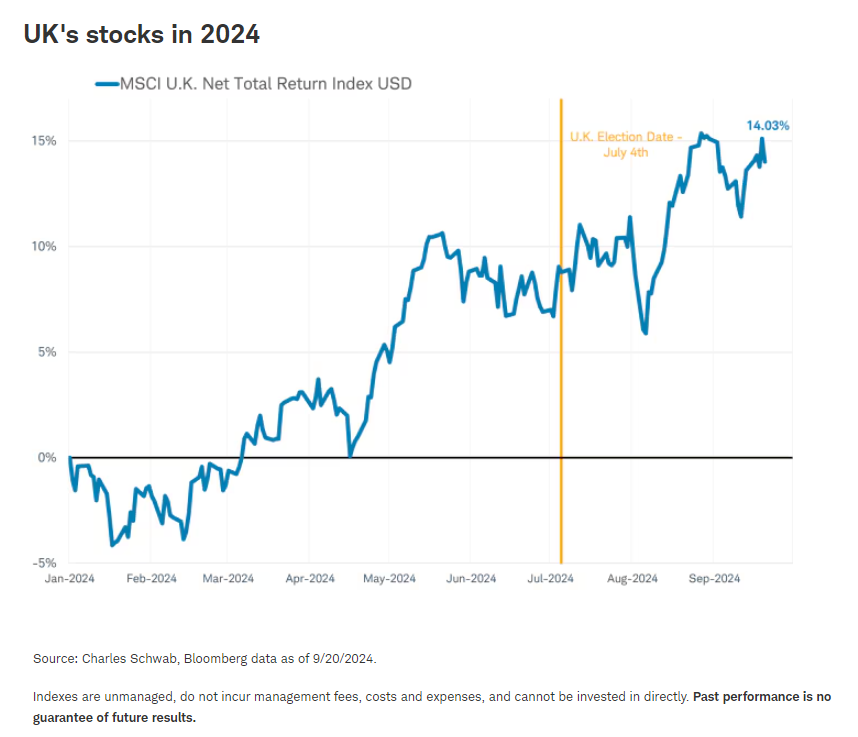

United Kingdom (July)

The July 4 election in the United Kingdom gave the Labour Party a large majority, coming very close to beating the party's best result seen in the 1997 general election. Yet, the potential for sweeping change is highly constrained by fiscal realities that likely mean little near-term impact on policy and markets.

New U.K. Prime Minister Starmer's main challenge will be working with already extended budget deficits that leave little room for new spending priorities coupled with an election pledge not to raise income, payroll, or VAT taxes, and a debt-to-GDP ratio over 100%, according to Office of National Statistics. The new chancellor said potential increases to capital gains and inheritance taxes will not be enough to cover the budget hole, adding there will be "more difficult decisions around spending, around welfare, and around tax."

The MSCI United Kingdom Index has produced a total return of 15% measured in U.S. dollars so far this year, seemingly unconcerned about the prospect of tighter fiscal U.K. policy.

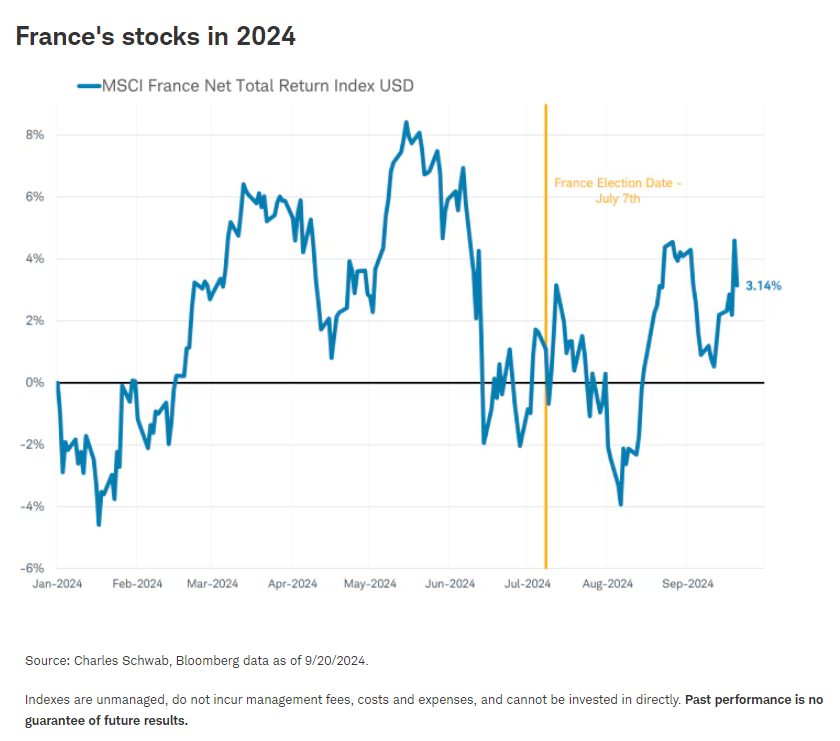

France (July)

Given the plans laid out by France's far-right and far-left parties, France's second-round election on July 7 had the potential to reshape the country's economic and fiscal policies and widen the budget deficit already in breach of European Union rules. In June, as the elections approached, French stocks fell and the risk premium on French debt widened. But the far-left New Popular Front (NFP) and centrist Ensemble coalitions coordinated in three-party run-off races to block the far-right from winning a majority. The NFP picked up the most seats, while President Macron's Ensemble came in second and the far-right National Rally third. Each fell far short of a 289-seat majority. The outcome implies little or no major legislative changes, as the leaders of all three groups have vowed not to work together on domestic policy, according to various media sources. President Macron remains in charge of France's international relations and trade policy.

Markets began to reverse June's losses after the first round of voting on June 30, with the margin of victory by the National Rally being insufficient to claim a majority in the second round. But even though the surprise outcome and hung parliament leaves some uncertainty, the main drag on France's stocks this year is more likely tied to the slump in Chinese consumer spending on French luxury brands such as LVMH, the largest stock in the MSCI France Index.

Looking ahead

With the Japan (Sep. 27) and U.S. (Nov. 5) elections just ahead, it's important to keep in mind the lessons of this year's elections: Proposals—particularly generous populist proposals—are unlikely to pass divided governments with tight budgets, limiting their impact on stock markets. Even widely supported trade restrictions may have more bark than bite. Actual policy may be more often dictated by economic circumstances rather than the proposals offered by policymakers.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI Taiwan Index is designed to measure the performance of the large and mid-cap segments of the Taiwan market covering approximately 85% of the free float-adjusted market capitalization in Taiwan.

The MSCI Korea Index is designed to measure the performance of the large and mid-cap segments of the South Korean market, covering about 85% of the Korean equity universe.

The MSCI Mexico Index is designed to measure the performance of the large and mid-cap segments of the Mexican market covering approximately 85% of the free float-adjusted market capitalization in Mexico.

The MSCI Netherlands Index is designed to measure the performance of the large and mid-cap segments of the Netherlands market covering approximately 85% of the free float-adjusted market capitalization in Netherlands.

The MSCI India Index is designed to measure the performance of the large and mid-cap segments of the Indian market covering 85% of the Indian equity universe.

The MSCI EMU Index (European Economic and Monetary Union) captures large and mid-cap representation across the 10 Developed Markets countries in the EMU covering 85% of the free float-adjusted market capitalization of the EMU.

The MSCI United Kingdom Index is designed to measure the performance of the large and mid-cap segments of the UK market covering approximately 85% of the free float-adjusted market capitalization in the UK.

The MSCI France Index is designed to measure the performance of the large and mid-cap segments of the French market covering about 85% of the equity universe in France.

0924-UJWH

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

Read more commentaries by Charles Schwab