Emerging-market (EM) equities have lagged developed-market (DM) stocks over much of the past decade. But some trends look more promising than the headlines would suggest. Earnings revisions for EM equities are finally beginning to look up, particularly in the technology and consumer-discretionary sectors. We believe an improved earnings picture could point to long-term opportunities for EM equity investors in five key areas.

1. China Should Never Be Underestimated

As the world’s second-largest economy and largest emerging market, China is a vital cog in the global economic engine. After a strong start to the year, China’s economy has stalled of late, weighed down by weakness in the country’s real estate sector and sluggish consumer spending. But relief could be coming in the form of accommodative monetary policy and long-term structural reforms.

In late September, China’s central bank announced plans to lower its reserve requirement ratio by 50 basis points (bp) and its key interest rate by 20 bp, with more cuts to come later in the year. We view this as evidence that policymakers are serious about China’s 5% growth target for 2024. Still, we believe market excitement about these actions will be short-lived unless they’re backed by fundamental improvements.

China is also moving ahead with regulatory reforms aimed at attracting more capital and boosting share prices. China’s nine-point guidelines are encouraging firms to return cash to shareholders, while a changing macroeconomic backdrop is making it easier for Chinese companies to pay dividends. Earlier in China’s growth trajectory, many companies followed a model of aggressive expansion, issuing large amounts of stock with little in the way of dividends. Well-managed Chinese companies are now able to return excess capital to shareholders, which is important in a slower macroeconomic environment.

While this could be a catalyst for dividend yielders, we believe it’s also a good setup for exporters and market-share gainers—particularly given China’s tepid macroeconomic backdrop. Since the market tends to paint China with a broad brush, we believe investors can find select companies within all three of these segments, which are trading at attractive valuations.

2. The AI Revolution Runs Through Taiwan

As the artificial intelligence (AI) revolution gains steam, look for Taiwan to be at the forefront. After all, Taiwan produces more than half of the world’s semiconductors. It’s also home to a whopping 90% of all global manufacturing capacity for the advanced chips that power machine learning. As Asia’s equivalent to Silicon Valley, Taiwan offers investors back-door access to AI at relatively attractive valuations.

Of course, there’s more to AI than chips. Some of the biggest players in the global AI supply chain are based in Taiwan, including testing and measurement firms and manufacturers of substrate, which allows advanced chips to be attached to circuit boards. We believe the AI build-out still has room to run. AI spending has shifted from software to hardware, which should benefit AI enablers across the developing world.

3. India Could Fill a Critical Void

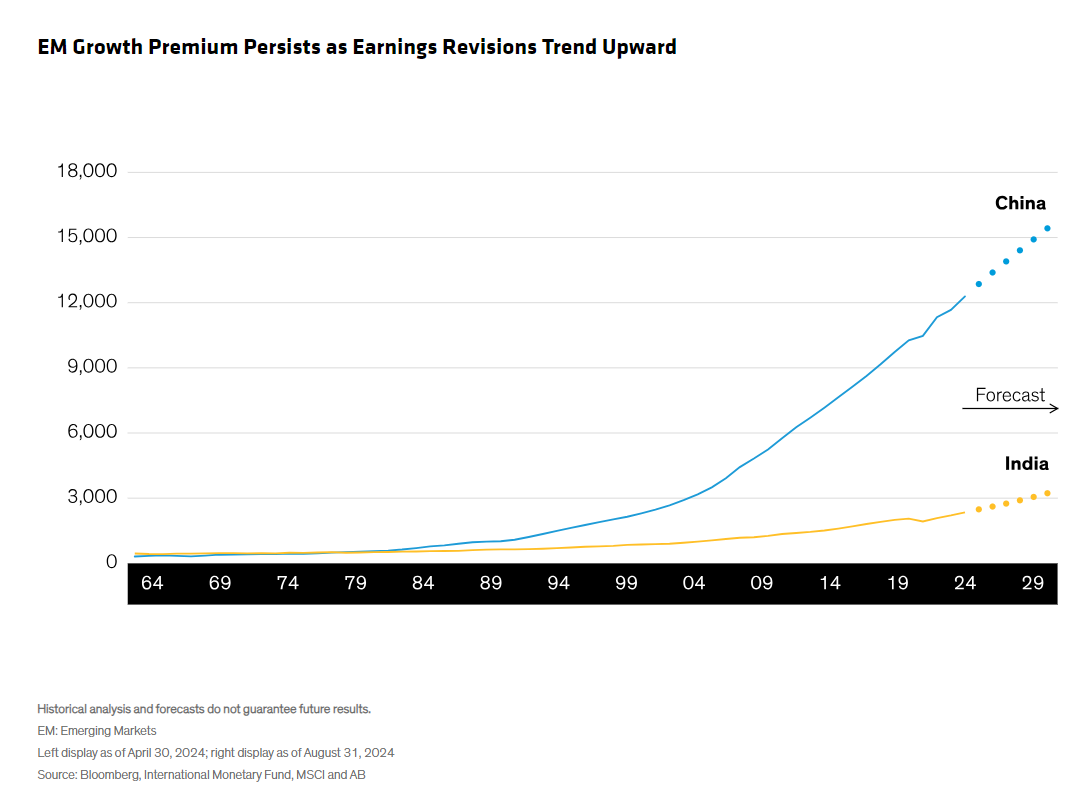

The world’s most populous nation is making a concerted effort to become more competitive on the global stage. Recent initiatives out of New Delhi include improving intercity travel, streamlining the country’s notoriously onerous bureaucracy, improving physical infrastructure and developing an increasingly cutting-edge digital infrastructure. In time, we believe infrastructure improvements and increased business efficiency will ripple across the Indian economy, creating new opportunities for investors. In the meantime, robust consumer spending has supported strong GDP growth in India. Currently, India’s GDP per capita is similar to the level at which China’s growth inflected upward (Display).

In time, India could play a bigger role in global supply chains. Increasingly, India is being eyed as a potential manufacturing hub, as international firms look to reduce their dependence on China. If China continues to see slowing economic growth, India may offer EM equity investors access to powerful growth potential.

4. South Korea: Barriers Down, Value Up?

South Korea has long been an EM powerhouse, from its days as one of the four Asian tigers to its current status as a global manufacturing leader boasting a well-diversified economy. Now, policymakers in Seoul are looking to attract even more investment by improving the shareholder experience for South Korea’s listed companies. The government’s “corporate value-up” program is aimed at boosting stock prices in part by improving corporate financial disclosure—while also encouraging stock buybacks and higher dividends.

These may seem like common-sense proposals, but they can be a tough sell in a country dominated by family-owned conglomerates (chaebols)—a key reason South Korean companies trade at such persistently cheap valuations. These reforms will take time, but we believe investors will eventually see benefits in the form of increased shareholder value—particularly in autos, financials and industrials.

5. Hidden Gems Abound Across the Developing World

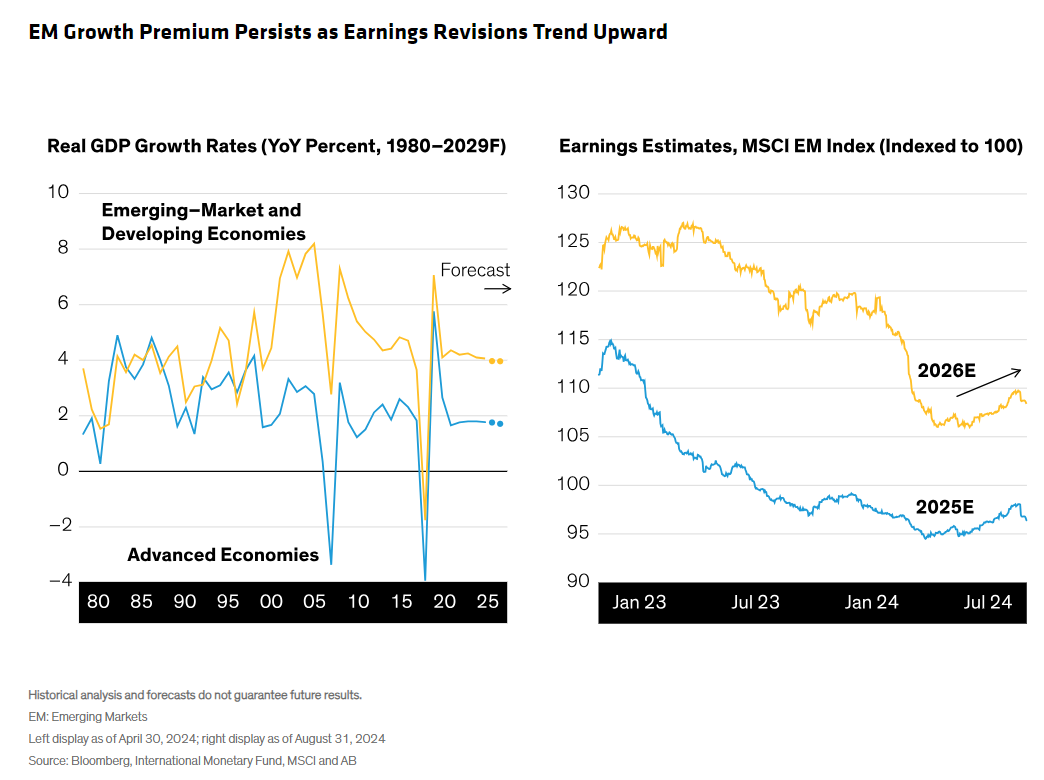

Collectively, emerging markets and non-DM countries account for roughly half of global GDP, as well as nearly 90% of the world’s population. And despite inconsistent performance, many EM economies continue to grow at a faster clip than their DM counterparts, while earnings estimates are trending upward (Display).

Compelling EM investment opportunities can be found all around the world. Markets outside of China, India, Taiwan and South Korea account for more than 25% of the MSCI EM Index, and warrant more attention from investors, in our view. This includes the Middle East, where Saudi Arabia is aggressively attempting to diversify its economy away from energy and the United Arab Emirates is bolstering its status as a neutral haven. We also see potential in other regions—from the rehabilitated banking sector in Greece to fintech in Kazakhstan and e-commerce in Latin America.

We believe EM equity opportunities are best captured through an active approach that incorporates both fundamental and quantitative research. Skilled investment managers can spot quality businesses in high-flying growth sectors as well as in struggling industries and weak macroeconomic environments. With EM earnings recovering and valuations still attractive, we believe this may an opportune time for investors to give EM equities a closer look.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein