After ten years of ultra-low interest rates, European companies are facing elevated rates and slowing euro-area growth. Euro high-yield bonds appear vulnerable on two counts: spreads are towards the tighter end of their historical range, and issuers need to refinance a large share of their total debt over the next two years. But there are several reasons why we think these worries may be overdone, and we believe investors should stay invested in a market that offers attractive potential returns.

High Yields Can Compensate for Risks

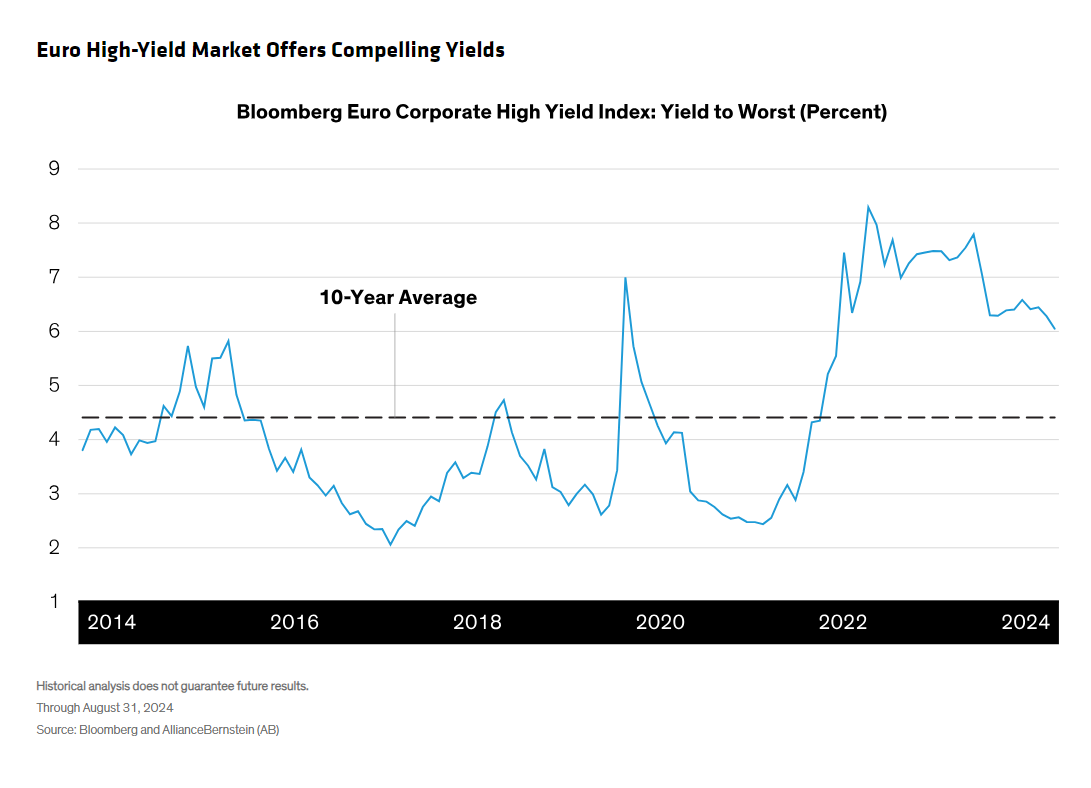

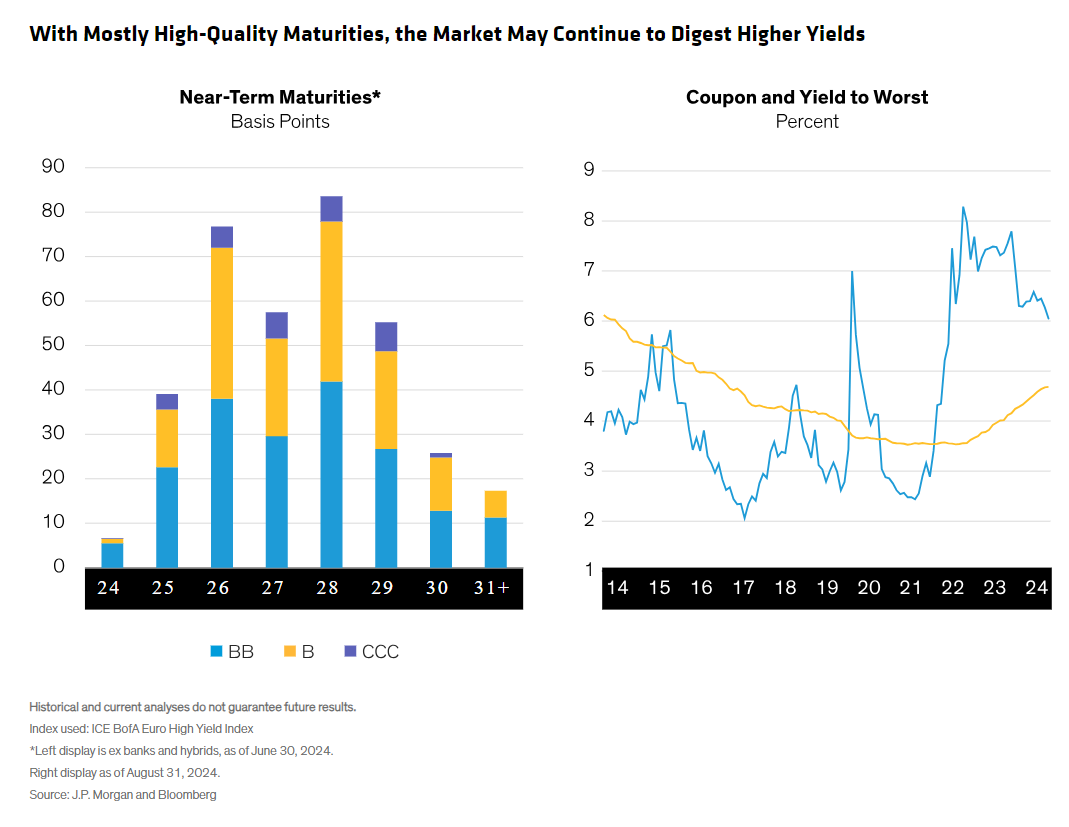

Euro high-yield bondholders are being well-compensated for the risks, in our view. At around 6%, yields are high by historical standards (Display).

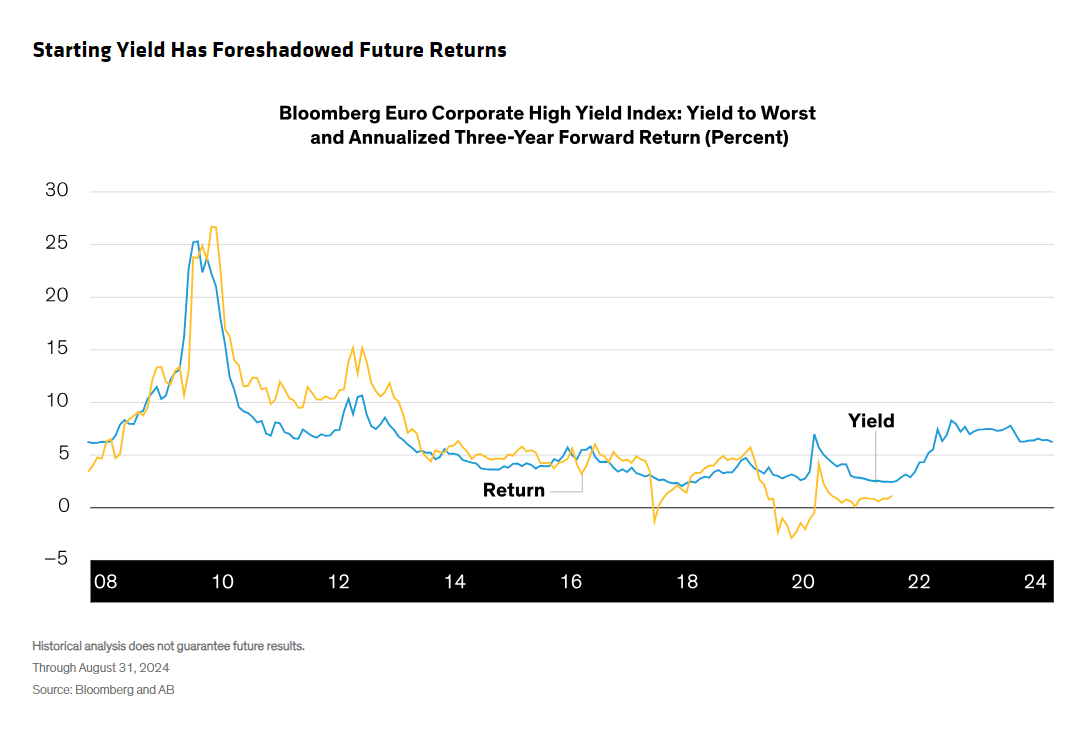

Historically, starting yield has been a strong predictor of return over the next three years (Display). As a result, current yield levels look attractive to us—especially considering that the European Central Bank (ECB) is cutting interest rates. We expect six cuts in 2025, with the ECB accelerating the pace from the second half of the year and reducing the deposit rate to 2% in the third quarter.

High Quality and Low Net Issuance Are Supportive

Global high-yield markets have changed a lot in recent years, and the euro market stands out for improved quality and strong technical support. Around two-thirds of the euro high-yield market is rated BB (versus 52% in the US). Euro CCC-rated bonds currently comprise just 7% of the euro high-yield market (down from 12% 15 years ago) and with an average price of €68 are already discounting a lot of bad news.

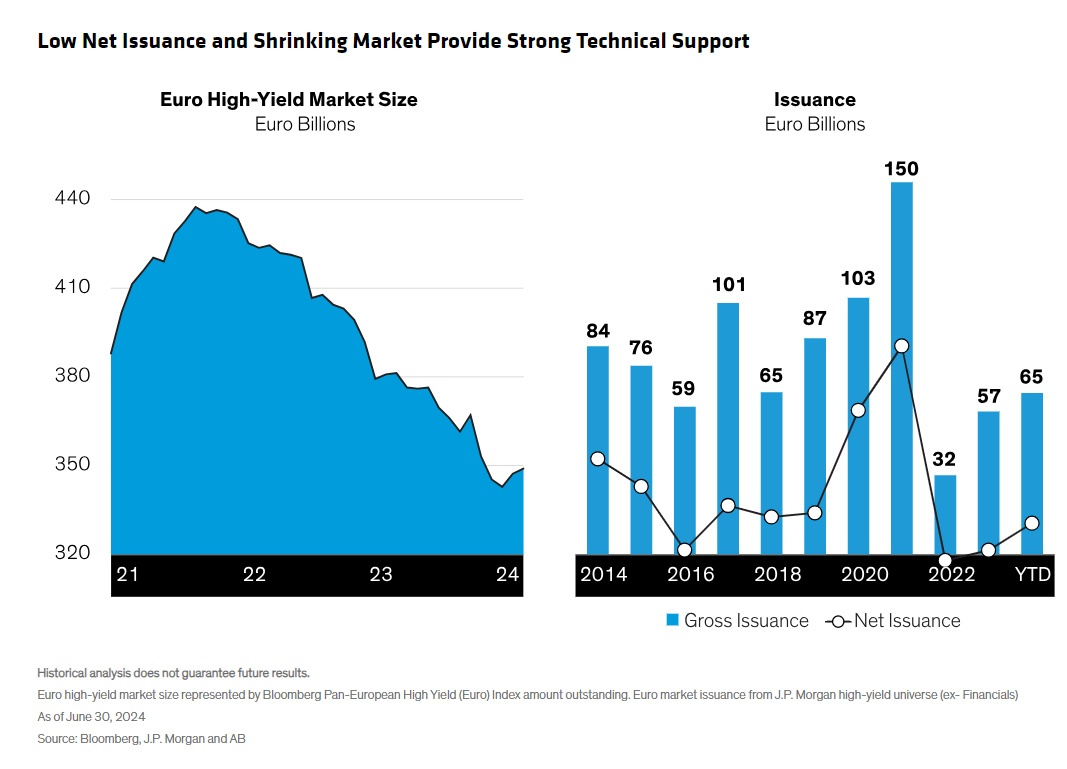

Meanwhile, the euro high-yield market has been shrinking (Display, left) because of recent maturities and €40 billion of upgraded credits migrating to investment grade since the start of 2023. Euro high-yield issuers have become more cautious, and net issuance has fallen as corporates have focused mostly on refinancing existing borrowings rather than investing for growth (Display, right). Roughly two-thirds of corporate issuance in the first half of 2024 was used to repay existing debt obligations and, with investor appetite for high-yielding euro credit remaining strong, demand continues to exceed supply.

Underpinning Performance Potential: Short Durations and Low Prices

As rates rose over the past few years, bond prices fell. Today, the euro high-yield market’s average bond price of around €96 is at a significant discount to pre-COVID levels.

As bonds approach maturity, their prices naturally rise toward par at €100. Considering that issuers will likely redeem their bonds ahead of upcoming maturities this “pull to par” can provide potential upside as it will likely be realized over a short period. This potential outcome can create a return stream that’s not only additional to the bonds’ yield to worst but is also largely independent of broad market conditions. That makes euro high-yield a potentially attractive portfolio diversifier, in our view.

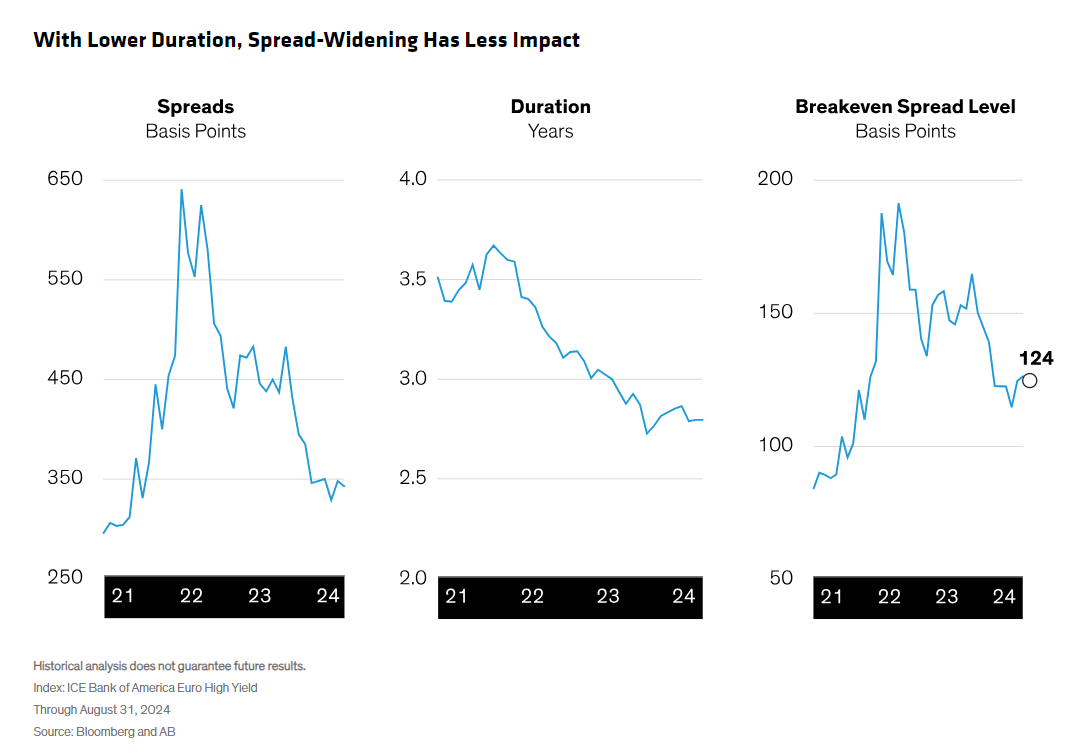

Thanks to the market’s shorter duration, bond prices are also now less sensitive to spread movements. Further, with yields so high, investors still have a significant safety margin: spreads would need to widen by more than 120 basis points before incurring losses (Display).

Approaching Maturities Are Not So Forbidding

While a tougher economic backdrop and high rates may pose challenges for companies, mostly their financing costs will only increase gradually, as their outstanding bonds mature over time. During the extreme low-rate period, issuers took the opportunity to extend their bonds’ maturities and refinance at very low yields. As a result, the average coupon paid is just 4.5% compared to today’s cost of financing at around 6.0%. And with yields continuing to fall, peak financing costs will likely be lower than the market was previously expecting.

Though approaching maturities are elevated through 2028, they’re mostly in the higher-quality part of the market that is better placed to cope with increased funding costs (Display).

Meanwhile, the amount of distressed debt is small and is concentrated in the low single B/CCC part of the market, so we don’t expect it to become a systemic concern. For the euro high-yield market overall, we expect defaults to stay low at 3% for 2025.

Euro High-Yield Can Help Diversify US Exposure

While the US high-yield market offers investors the widest range of opportunities, euro high yield represents a smaller but complementary market that’s less mature, less efficient and more varied. For instance, it has a higher credit rating than its US counterpart (BB- vs B+), lower defaults (1.2% versus 2.8%, as of June 30, 2024) and a more defensive sector composition, making it an effective diversifier, in our view.

Given the strong return potential across both markets, we believe investors shouldn’t be deterred by worries that may prove overplayed.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein