Equity Outlook: As Volatility Rises, Resist the Tactical Temptation

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGlobal equities advanced in the third quarter despite acute volatility, driven by uncertainty over the US economic outlook and a rethink of the technology giants. In fluid market conditions—and ahead of fateful US elections—we think investors should maintain a strategic focus on finding sources of healthy earnings growth that drives long-term returns.

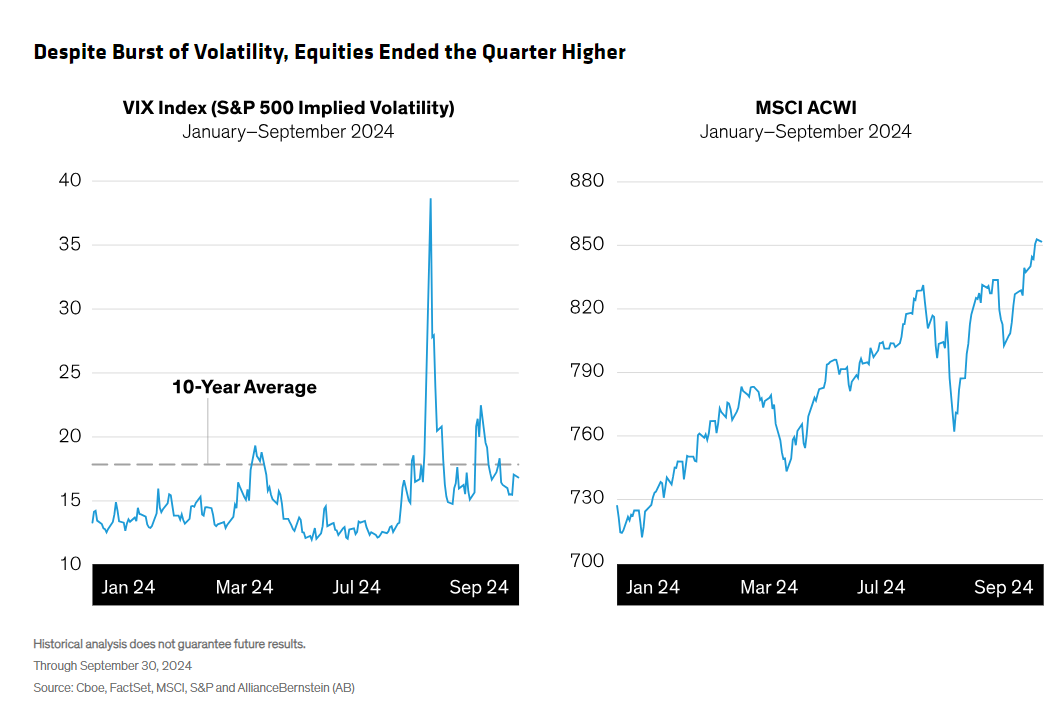

After relatively calm market gains through the first half of the year, investors experienced an unsettling third quarter. Much of the instability was driven by growing signs of US economic weakness. When the US Federal Reserve announced an aggressive 0.5% interest-rate cut on September 18, it reassured investors that inflation could be tamed without tipping the US economy into recession. Equity markets began to recover.

Before the Fed cut, in early August, volatility spiked to its highest since 2022, only to settle above levels seen over the last year (Display). Yet when the dust settled, the MSCI ACWI Index of global developed- and emerging-market stocks finished the quarter up 6.6% in US-dollar terms, taking its year-to-date gain to 18.7%.

Japanese stocks advanced in US-dollar terms but finished the quarter down in yen terms. In August Japanese equities tumbled after the Bank of Japan raised interest rates in July and the yen strengthened. The rate hike had a global ripple effect by triggering an unwinding of the longstanding yen carry trade, in which investors borrowed cheap yen to finance asset purchases elsewhere. This added to worries about equity markets and contributed to the volatility spike in early August.

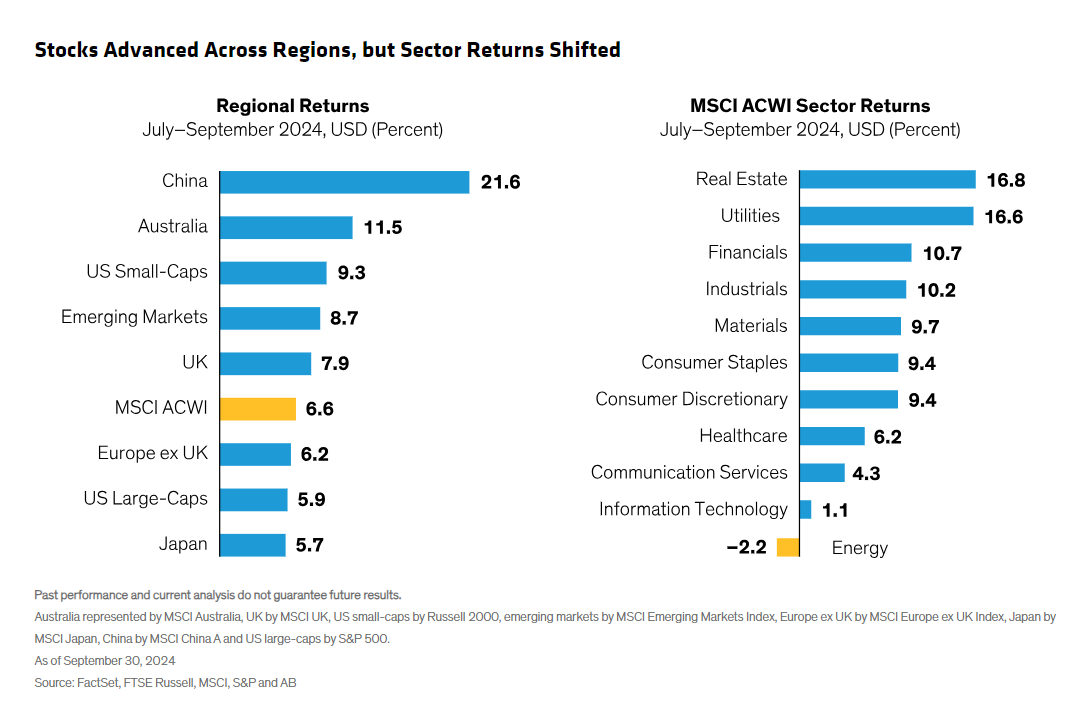

Then, in September, after the Fed cut rates, US large-caps rebounded, though they underperformed European, Asia-Pacific and emerging markets in the quarter (Display). Chinese stocks posted a powerful rally in late September—after eight weak months—as markets cheered new government stimulus measures.

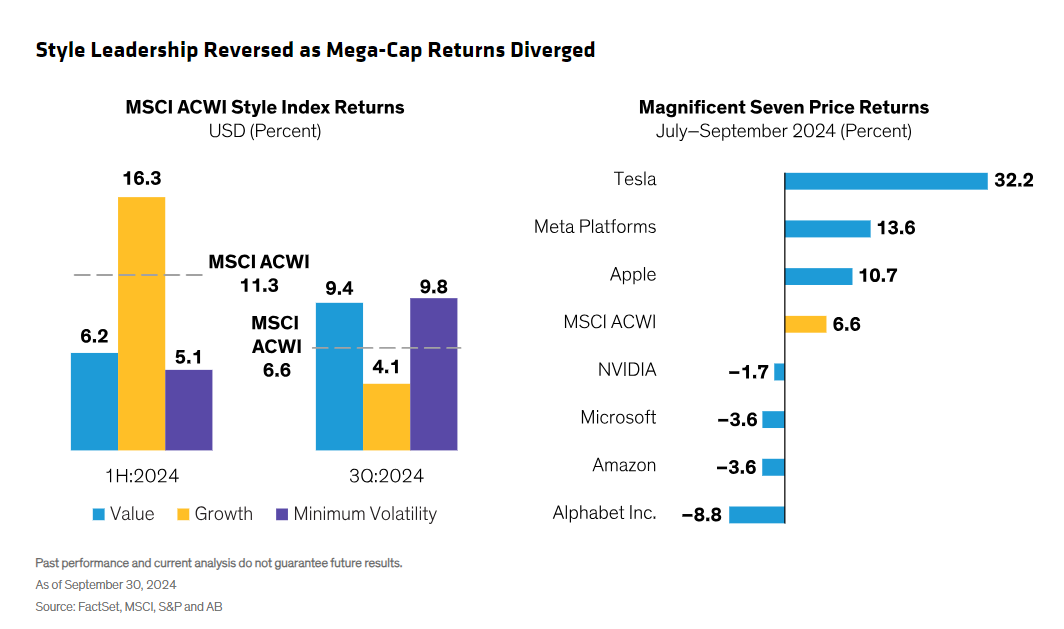

Sector performance shifted dramatically. Technology stocks, which led markets in the first half, were among the worst performers (Display, above), as returns of the Magnificent Seven (Mag Seven) US mega-caps weakened. Real estate and utilities, defensive sectors known for interest-rate sensitivity, were top performers. Growth stocks underperformed both value and minimum-volatility stocks in a reversal of trends from earlier this year (Display).

Reality Check? Reconsidering the Mega-Caps

Technology and growth weakness reflected a reassessment of the US mega-caps after two dominant years. Although their second-quarter earnings generally met expectations, returns diverged, with four of the Mag Seven stocks declining and trailing the broader market during the quarter (Display, above).

We’ve often said investors must be cautious toward this group of giant stocks as their valuations soared. Yes, the Mag Seven includes companies with great businesses and growth potential. However, given their huge market weights—about 30% of the S&P 500 combined—we think it’s very risky to own the entire group, and each stock should be held in line with a portfolio’s philosophy at appropriate weights.

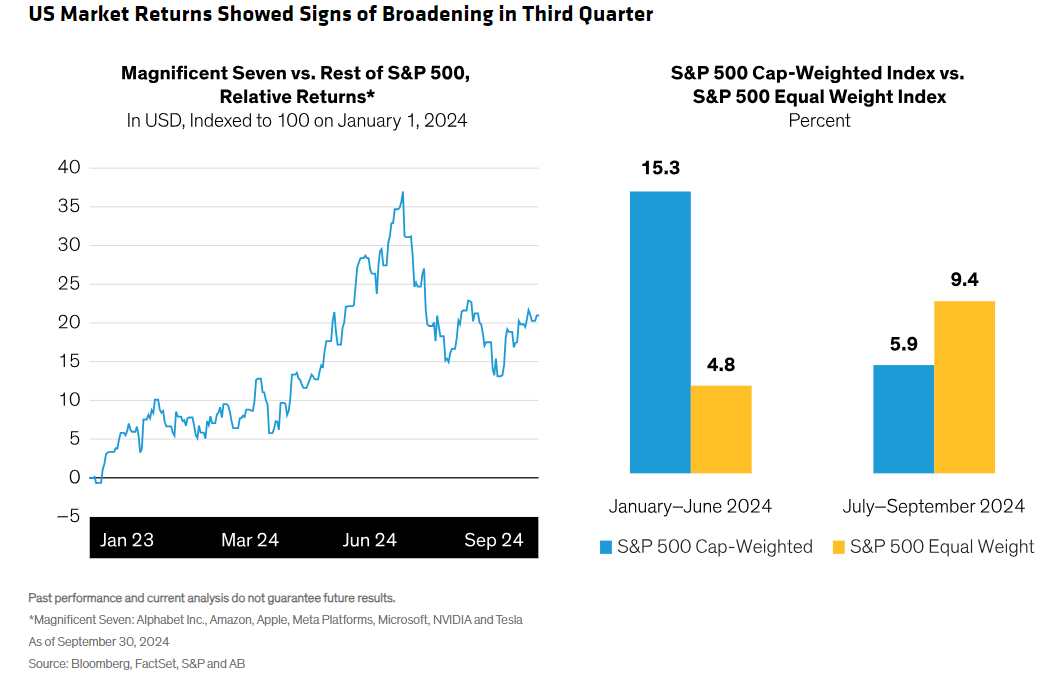

What caused the rethink? In our view, investors became more discriminating about whether massive investments in artificial intelligence (AI) will deliver a sufficient return over time. As a result, the mega-caps underperformed the S&P 500 since mid-July (Display). Meanwhile, the S&P 500 Equal Weight Index—a proxy for the broader market—outperformed the cap-weighted benchmark. We think the market reaction indicates that expectations were set too high for the Mag Seven.

Despite the Mag Seven’s underperformance, the S&P 500 still delivered a positive return in the quarter. This may signal that a broader group of high-quality companies that were left behind in recent quarters—what we’ve called the Magnificent Others—are starting to be rewarded.

Soft or Hard Landing for the US?

The reevaluation of the technology giants unfolded at a pivotal moment for the global economy. Easing inflationary pressures led major central banks—including the Fed, the European Central Bank and the Bank of England—to begin transitioning away from restrictive monetary policies in an effort to prevent a weakening of macroeconomic growth.

In the US, while real risks persist, we think a soft landing—a slowdown of economic growth—is more likely than a recession. The Fed’s September rate cut kicked off a monetary easing cycle that should last for several quarters, according to AB economists. The pace and magnitude of future cuts in the US and Europe will affect market returns and corporate performance. But we don’t think the trajectory of rate cuts should be the main focus of long-term equity investors for two reasons.

First, no matter how rate cuts unfold, we expect inflation to remain relatively higher than we’ve seen in the last 10 years. Our research suggests that equities have been vital for generating real returns during periods of moderate inflation over the last century.

Second, we think long-term equity performance is mainly driven by corporate earnings and cash flows. While economic growth and rate cuts affect businesses, active investors can target companies that are capable of delivering earnings growth through challenging environments; even in tougher conditions there will be winners and losers.

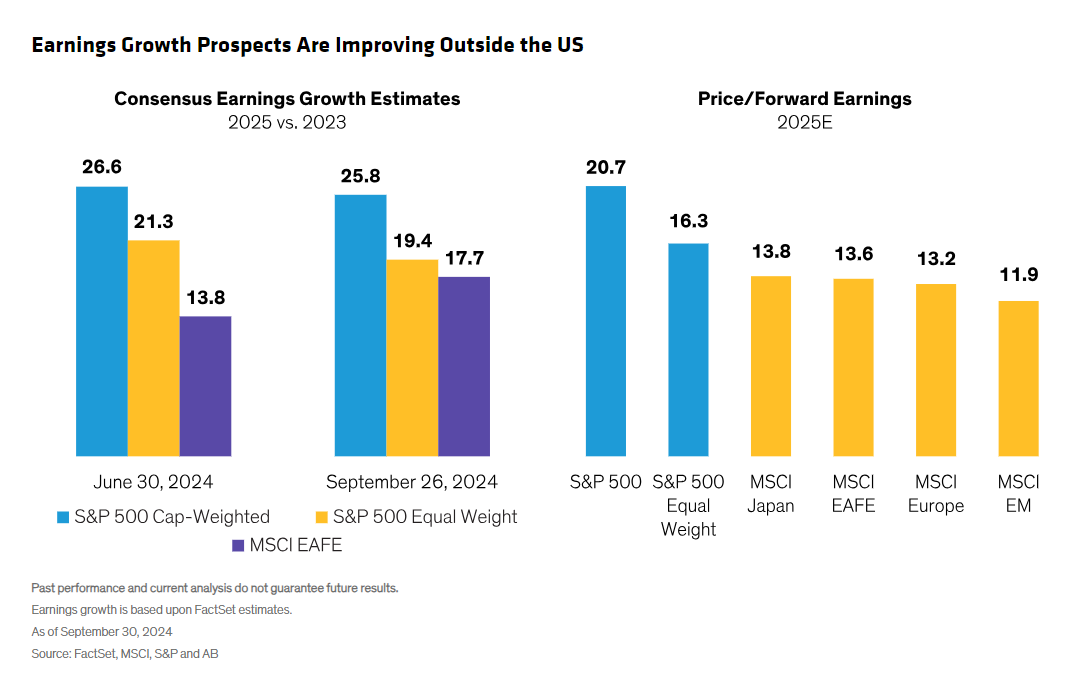

The good news is that earnings patterns appear to be broadening. The powerful earnings growth expectations of the Mag Seven seem poised to moderate. And during the third quarter, consensus earnings estimates suggest that non-US companies are catching up with US companies (Display). While a gap is likely to remain, attractive valuations outside the US are creating opportunities for investors to identify companies with high-quality fundamentals, whose shares haven’t reflected their business strengths. Within the US, valuations outside the mega-caps—reflected by the S&P 500 Equal Weight—also look attractive.

Earnings Growth Patterns Are Changing

So what should investors look for? It depends on your investment philosophy. Growth investors can target companies with clear business advantages to support profits that exceed the cost of capital—a robust indicator of consistent growth potential. After languishing for years, value stocks also deserve attention, as the style has shown signs of life, and many investors are underexposed.

In Europe, despite hurdles to economic growth, individual company earnings still matter most for equity returns, in our view. Our research shows that European equity returns have closely tracked long-term earnings growth over time, and companies with stronger earnings than the market tend to be rewarded.

Emerging markets, too, are presenting diverse opportunities from AI in Taiwan to Greek bank recoveries. Even in China, incentives for companies to boost dividends could support equities. The Chinese economy remains hamstrung by a distressed property sector and sluggish growth, but new rate cuts and stimulus measures to support the equity market unveiled in September could add an impetus for select investment opportunities.

And as the recent bout of market unease reminds us, lower-volatility securities should be an important part of a robust equity strategy. The key is to focus on businesses with consistent performance patterns and attractive valuations, which can help cushion losses in a downturn and bolster confidence to stay invested through turbulence.

Do US Elections Matter?

Many investors expect stock markets to be unstable ahead of US elections in November, especially given the polarization of US politics. However, our research of forward volatility contracts suggests November isn’t expected to be a particularly turbulent month.

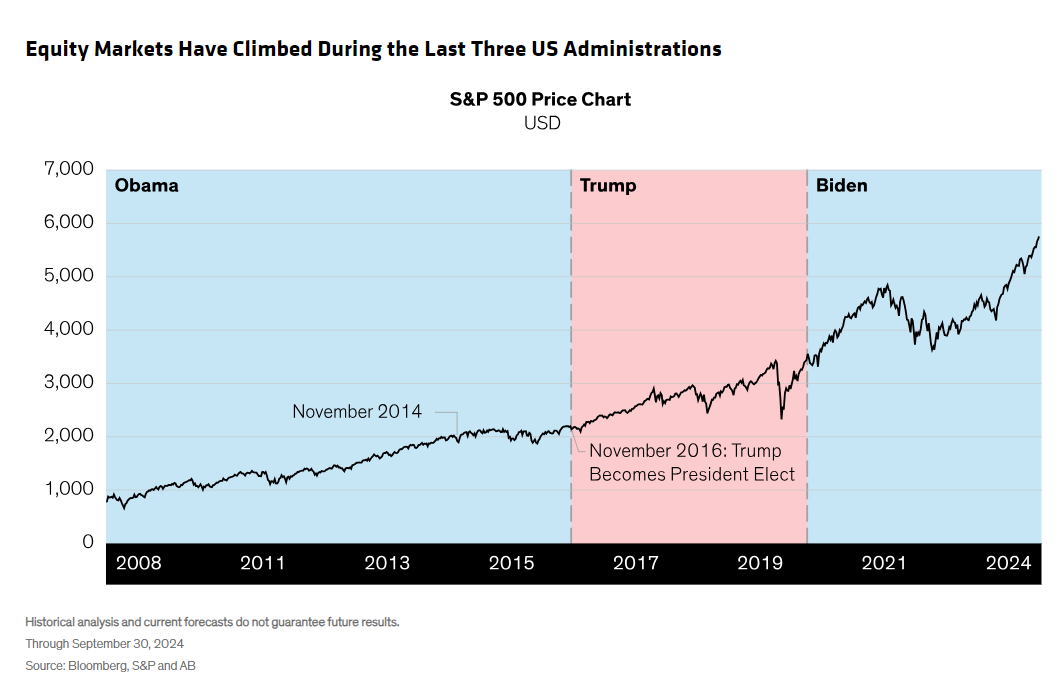

Even if investors could project the winner, it wouldn’t necessarily help much. In a historical perspective, the political party of the US president hasn’t made a material difference to equity returns. Since the global financial crisis, the S&P 500 has posted healthy long-term gains under three different presidents, though policy decisions have had periodic effects on market returns (Display).

To be sure, the government’s composition—and whether the incoming President will have a supportive Congress or not—will influence policies and fiscal priorities. Policy changes could be more substantial than usual given the significant distinctions between the candidate’s positions in the 2025 election.

However, we believe the election outcome is unlikely to materially shape long-term corporate earnings growth in aggregate. That said, it does matter for risk management. Active equity investors will need to assess how companies in their universe will be affected by policy changes over the long-term, from tax cuts or hikes to fiscal spending priorities.

Of course, US policies have major global implications that investors must incorporate into research. Examples could include the impact of potential new tariffs or how major geopolitical changes can impact business or defense spending in Europe.

Whatever the next US government may look like, we think fiscal spending is likely to be higher. This supports our prognosis that even as inflation eases from post-pandemic peaks, it will likely normalize to higher levels than we’ve observed in the prior decade.

Staying the Course

On the cusp of a decisive political period after a volatile quarter, how should investors respond? First, define your long-term goals clearly and verify that your allocation is positioned to capture diverse sources of returns from different parts of the market. Second, set your sights on the long-term—at least three years ahead—and invest in portfolios with coherent plans for surmounting short-term volatility. Third, resist the temptation to change your strategy: this quarter reminded us that volatility is a normal part of investing and a well-diversified plan built on well-researched investment insights is the key to staying confident in your equity allocation through changing market conditions.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All