Is China Investable Again?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat would it take for the recent rally in China's stock market to become sustainable and one of the biggest bull markets for China of the past 20 years? A lot—but it's not impossible.

A new bull market

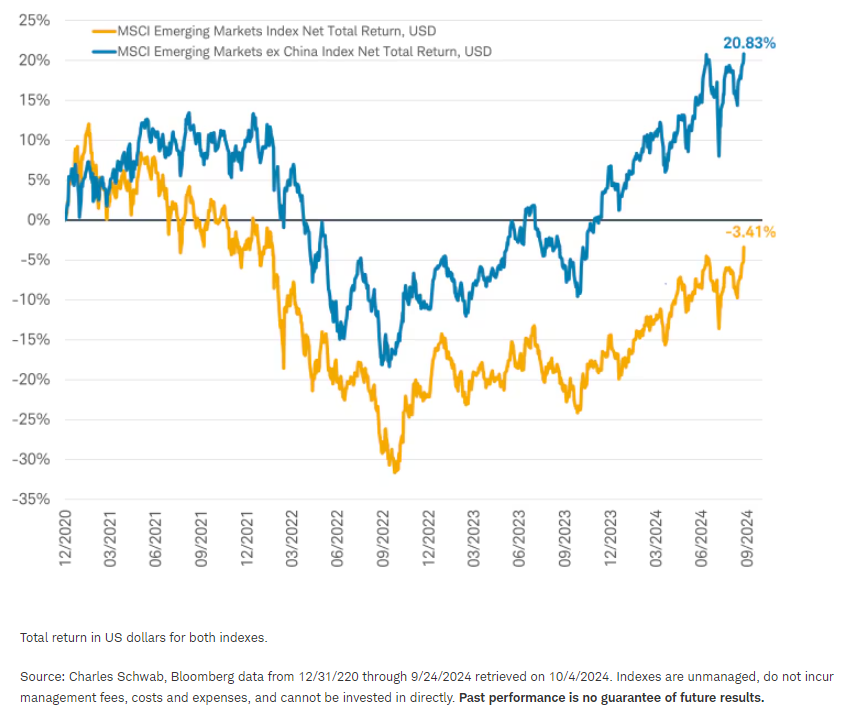

During the past few years, we've written about the need for China to deliver much more powerful stimulus and been repeatedly disappointed. China's stock market was near the low end of its 15-year range as of mid-September, trading at a forward price-to-earnings ratio of less than 9, near its lowest levels of the past 20 years. As the biggest weight in the MSCI Emerging Market Index, China had been dragging down the performance of the emerging market (EM) stocks asset class. From the end of 2020 until the day before China's announcement of new stimulus on September 25, 2024, the total return of the MSCI Emerging Market Index was a loss of -3%, while the MSCI Emerging Market Ex-China Index produced a 21% gain.

China acted as a drag on EM stocks from the end of 2020 until late September

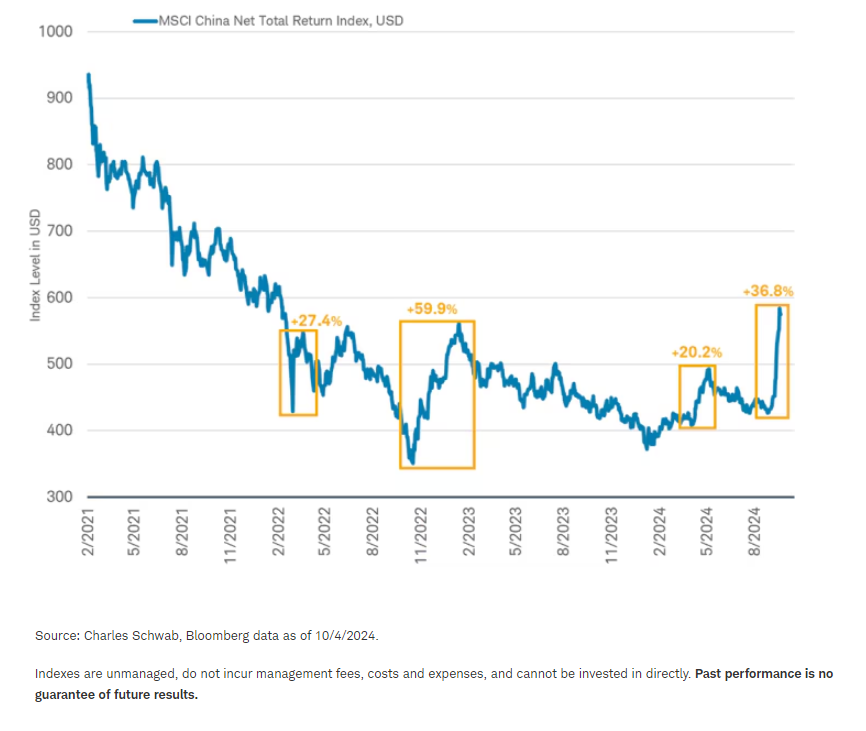

September's announcement brought a surprise and emerging market stocks, as measured by the MSCI Emerging Market Index, ended the third quarter having outperformed the S&P 500 Index. The press release of a major Chinese stimulus program lifted China's stocks into a new bull market from their mid-September low, just ahead of the weeklong market closure for the Golden Week holiday that started October 1.

Just to review, China's stocks have experienced four stimulus-driven bull markets over the past four years—including the one earlier this year in May—and the prior three all soon fizzled out, reversing their gains.

Past bull markets have fizzled out

What is China's problem?

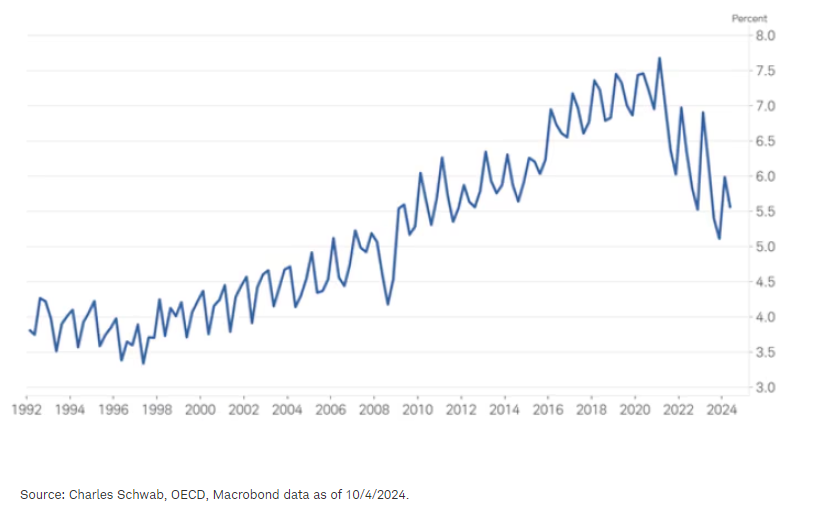

China's economic problems feed into each other—so let's walk around this circle. China's weak property market caused fiscal policy to aggressively tighten this year which reinforced the drag on the economy and further weakened the property market. Trying to break the cycle, China's central bank announced aggressive monetary policy easing on September 24; including cutting the one-year prime loan rate to its lowest level since the People's Bank of China began using it as the main policy rate in 2016.

Real estate recession: China real estate investment as a percent of GDP

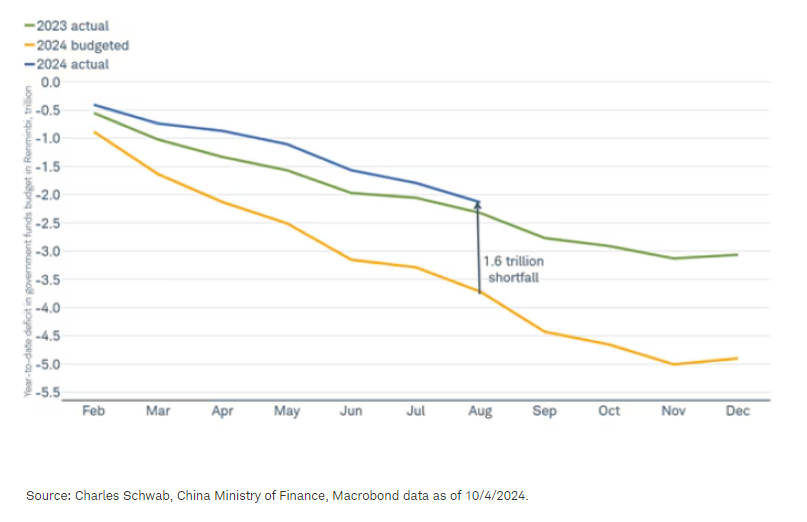

Fiscal spending has come in a lot lower than last year and policymakers' plans in the budget that was submitted to the National People Congress in early March. In China, the general government budget only tells part of the fiscal story. China has three additional national budgets: the government funds budget, the state capital operations budget, and the social insurance fund budget. The government funds budget is the source of the fiscal tightening.

The 2024 plan was for China's government funds budget to include 7 trillion renminbi in revenue and 12 trillion of spending, resulting in a deficit of 5 trillion. The planned deficit was expanded from 4 trillion last year, to provide an economic boost. As of the end of August, two-thirds the way through the year, the deficit was only 2.1 trillion. Planned fiscal policy would have allowed for the deficit level to be around 3.7 trillion at this point. As a result, there was an unintended 1.6 trillion tightening of fiscal policy, acting as a drag on the economy.

Unintended tightening of fiscal policy

The shrinking government funds budget comes from local governments' sales of land again coming in much weaker than anticipated following China's clampdown on borrowing by large real estate developers. The slow pace of land sales means revenue is down 21% from last year and local government spending on land infrastructure upgrades for development has been impacted. Therefore, the weak property market gave rise to lower government spending, which has acted as a drag on the economy and subsequently reinforced the weakness in the property market.

To make up for the shortfall and try to break this cycle of weakness, local governments could possibly issue special local government bonds to finance more infrastructure spending. However, the current quota for special-purpose local bonds was set in March and has not yet been boosted to account for the accumulating shortfall. Furthermore, the central government seems to be slow to approve projects for special bond funding, possibly wanting to avoid losses as property values continue to fall. Consequently, local government bond issuance at this point in the year has come in below the now insufficient quota.

Special bond issuance may accelerate in the fourth quarter. Should it move toward closing the gap and fulfilling the quota, it could turn around the government fund deficit from a fiscal drag of about 2 trillion to closer to 1 trillion. It might help, but at that level, spending would still be far from the planned 1 trillion fiscal expansion. The government funds deficit was also around 1 trillion smaller than budgeted in both 2022 and 2023, which contributed to China's lingering economic malaise.

China's aggressive easing of monetary policy by its central bank is unlikely to stimulate economic activity absent a break in the cycle of tightening fiscal policy. As a result, China's stock market rally could fizzle and give back much of the gains as it did in May when prior stimulus announcements ultimately failed to deliver real support to the economy.

What we are watching to see if it works

China's policymakers have announced interest rate cuts and plans to issue more central government bonds to try to address both monetary and fiscal stimulus, according to official government statements. It's a move in the right direction, but there are a few things we're looking for to judge whether the stimulus announcements deliver the boost to China's growth that may sustain its stock market's gains.

- Boosting local government special bond issuance. Raising the special bond issuance quota by more than 1 trillion renminbi would be needed to ease tight fiscal policy. Last year, the central government decided in October to issue an additional 1 trillion in bonds for the year. We feel more would be needed this year to boost growth, given the deeper property downturn. Following monetary policy easing announcements from the People's Bank of China (PBOC) earlier in the week, China's Politburo announced 2 trillion in issuance of special treasury bonds by the central government on September 26th. An announcement on fiscal support for 2024 could come the week of October 22, in conjunction with the Standing Committee meeting.

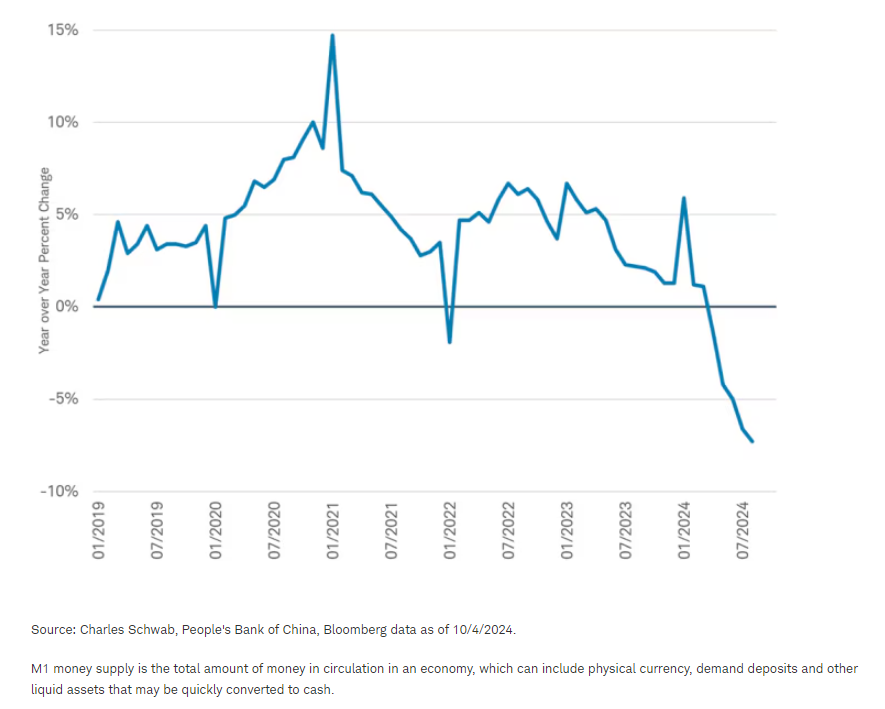

- Faster money supply growth in China. To see if expansionary monetary policy is working to offset the fiscal tightening, we can track the pace of money supply growth. The stimulus by the People's Bank of China is intended to turn around very weak borrowing by businesses and consumers to fuel growth. A sign that this was working would be more demand for money. So far, money supply growth has turned negative in recent months, falling below -5% as of August.

Shrinking money supply

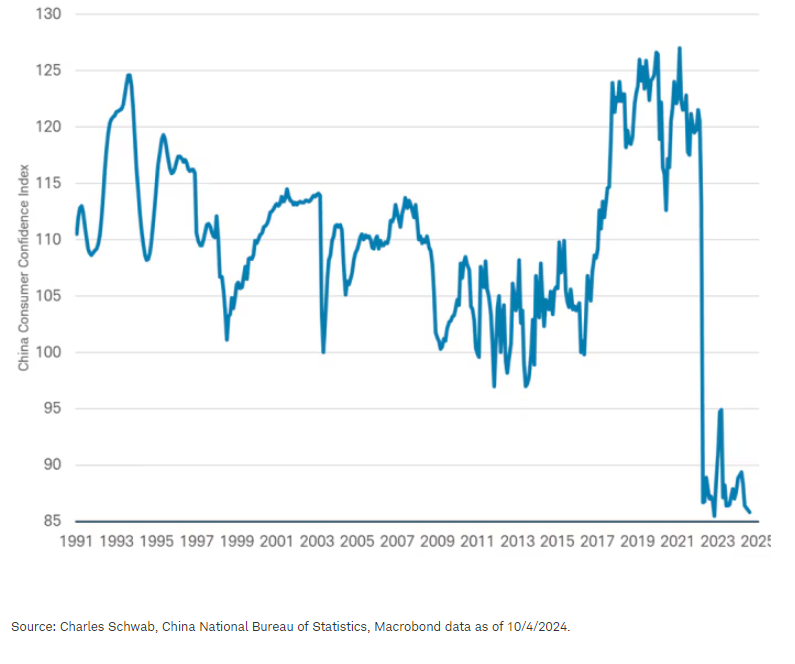

- A rise in consumer and business confidence. China's policymakers could guarantee homebuyer deposits and boost social safety nets to reduce high levels of precautionary savings that are keeping consumption in check and could signal they are going to reduce business interference with sudden regulatory changes that have impeded business investment. Although the stock market rally and reduction of mortgage payments could boost confidence in the near-term, consumers need hope of improvement in income and job growth for the rally to have staying power.

Very weak consumer confidence in China

Is China investable?

China has been a drag on emerging-market stock performance for years. Sustainably turning that around is a formidable challenge for policymakers. Back in September 2020, the government's "three red lines" policy created restrictions on the property market to crack down on the buildup of leverage and curb speculation in housing that had driven up prices and to divert investment to more productive, high-tech areas of the economy. The policy worked too well and ended up starving developers of capital, causing a loss of confidence by homebuyers and price decline that became a self-reinforcing negative feedback loop. Abrupt changes in regulations on businesses and scarring from zero-COVID policies that reduced income growth and job prospects kept pressure on consumer and business confidence. On the property front, mortgage and down-payment rates have been lowered, and homebuying restrictions in some cities have been relaxed. However, the lack of funding for property developers has not been addressed. It will take a lot for the stimulus announcements to sustainably change China's economic and stock market trajectory—but it's not impossible.

China's policymakers have already announced interest rate cuts and plans to issue more central government bonds to try to address both monetary and fiscal stimulus. Consumer confidence could begin to turn around and create a positive feedback loop for the economy. While China's policymakers are at last signaling that they understand the need for major stimulus, without sufficient follow-through on these announcements, the stock market rally may not continue and instead is likely to follow the path of prior announcements and give back nearly all the gains over the coming months. But if the policymakers deliver, the tradable rally in emerging-market stocks could turn into a sustainable bull market and, in the minds of many investors, make China (and emerging markets) investible again.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Markets (EM) countries, covering approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets ex China Index captures large and mid-cap representation across 23 of the 24 Emerging Markets (EM) countries excluding China, covering approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs) covering about 85% of this China equity universe.

1024-XT4X

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All