In recent months, investors' attention has been on easing monetary policy, as central banks around the world started to cut interest rates. However, the less closely followed tightening of fiscal policy in Europe and China could offset the global stimulus of lower interest rates.

Fiscal policy involves taxes and spending set by the government while monetary policy is enacted by the central bank, which tends to be politically independent. When they both move in the same direction, they combine to provide a potent boost or restraint on growth and inflation. This was evident in 2021 when central banks aggressively cut rates in response to the global pandemic while governments approved new spending programs and tax cuts that drove large budget deficits. That year saw the strongest global economic growth and inflation in nearly 50 years, according to the International Monetary Fund (IMF). In 2023, both tighter budgets and rate hikes contributed to slower growth and inflation. But, when fiscal policy and monetary policy conflict with each other, the outcome is less clear.

China

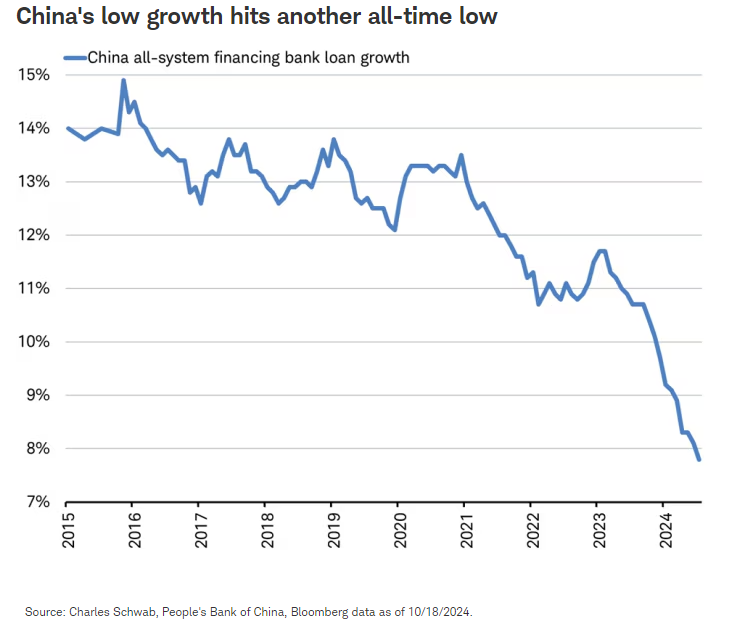

The central bank of the world's second largest economy, the People's Bank of China (PBOC), cut its main policy rate (the one-year medium term lending facility rate) by 30 basis points in September, the second cut this year. Yet loan demand remains weak, suggesting easier monetary policy isn't working. The latest data from the People's Bank of China shows that loan growth decelerated from 8.1% year-over-year in August to a new record low of 7.8% year-over-year in September. Last week's money supply data shows growth slowing further to 7.4%, reflecting a shrinking amount of money circulating in the economy as activity remains sluggish. With consumer confidence near all-time lows in China, there seems to be little demand for borrowing by households or businesses even at the lowest policy interest rate the PBOC has ever implemented.

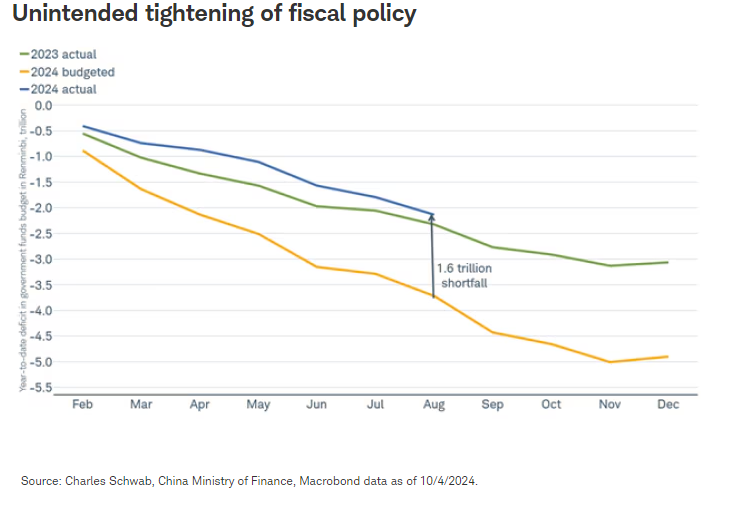

The PBOC's easing of monetary policy is being undermined by an unintended tightening of fiscal policy. China's fiscal policy problem is explained in this excerpt from our recent commentary entitled Is China Investable Again?:

"The 2024 plan was for China's government funds budget to include 7 trillion renminbi in revenue and 12 trillion of spending, resulting in a deficit of 5 trillion. The planned deficit was expanded from 4 trillion last year, to provide an economic boost. As of the end of August, two-thirds the way through the year, the deficit was only 2.1 trillion. Planned fiscal policy would have allowed for the deficit level to be around 3.7 trillion at this point. As a result, there was an unintended 1.6 trillion tightening of fiscal policy, acting as a drag on the economy."

The net effect of easing monetary policy and tightening fiscal policy has been GDP coming in below the government's target of 5% this year. Fiscal policy has contributed to a weak outlook for earnings, while monetary policy has helped to lift stock valuations from a price-to-earnings ratio of 8 at the start of this year to 11 as of mid-October for the MSCI China Index. These contrasting factors had offset each other leaving the MSCI China Index flat for the year as of September 9. However, the index is now up about 20% this year as of mid-October amid wild volatility tied to recent fiscal and monetary policy announcements.

Europe

The European Central Bank (ECB) cut policy rates by 25 basis points again last week for the fourth time this year. The ECB is widely expected to cut rates at every meeting though the middle of next year. But at the same time, fiscal policy makers are planning to tighten budgets.

In the U.S., the budget deficit has soared with the Congressional Budget Office forecasting it will remain above 5% of GDP over the coming decade. In contrast, Europe has an effective "debt ceiling" that has been re-introduced, where governments must manage budget deficits to a target of 3% of GDP. Plans presented in recent weeks show that the three largest Eurozone economies (Germany, France, and Italy) will all be pursuing tighter fiscal policies in 2025 to rein in their budgets.

- In Germany, the cuts are intended to adhere to the German Debt Brake, a balanced budget amendment, that restricts structural budget deficits to 0.35% of GDP.

- In France, where cuts to excessive deficits are required by the European Union, new prime minister Barnier has announced spending cuts and new taxes which seem to be supported by the new government.

- In Italy, the government announced spending cuts to bring down the Italian deficit from 3.8% of GDP in 2024 to below 3% in 2026.

In GDP terms, the fiscal tightening in Europe may average about 0.7 percentage points in 2025, ranging from about 1% of debt-to-GDP in France to about 0.5% in Italy and Germany. Using the European Commissions' 0.75 short-term fiscal multiplier (which estimates how government spending affects GDP), tightening would result in a drag on GDP of 0.5% in 2025. This drag could be partially offset by the European Recovery Fund and New Green Deal spending which is financed at the European Union level. By itself, this drag is not likely to be enough to tip Europe into recession but keep growth below average. The International Monetary Fund forecasts 1.5% growth for Europe's GDP in 2025. This fiscal policy tightening points to an outlook for modest single-digit earnings growth for European companies in 2025.

The conflict between tighter fiscal policy (potentially acting as a drag on earnings growth) and easing monetary policy (potentially boosting valuations) may net out in a favorable way for investors. This is because earnings growth expectations by analysts are already lackluster with just single-digit growth forecast for coming quarters on easy comparisons to last year when earnings were declining, suggesting less potential downside to earnings expectations. And because stock market valuations offer some potential for upside as experienced during past monetary policy easing cycles that took place in 2008-09 and 2011-16.

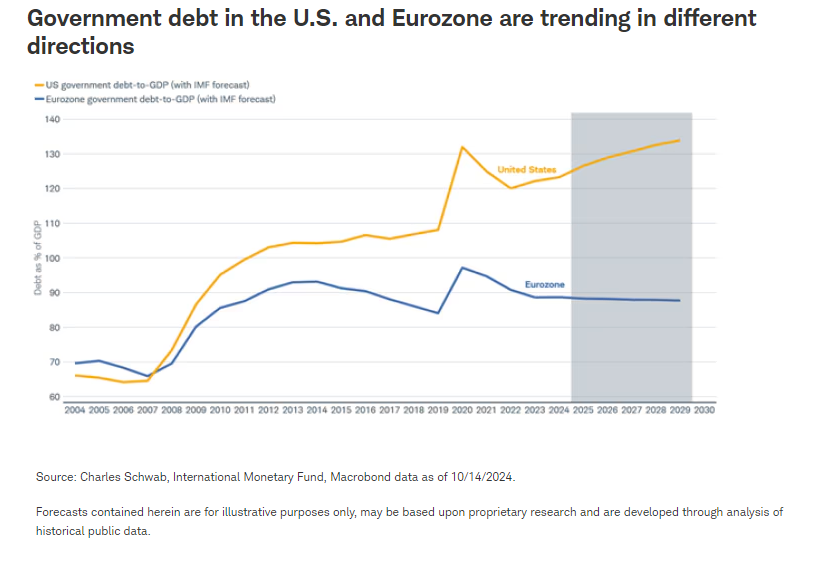

While tighter fiscal policy can act as a drag on short-term growth, it is not without longer-term benefits. Prior to the Global Financial Crisis of 2008, the percentage of debt-to-GDP in the U.S. and Europe were similar. But since then, U.S. debt-to-GDP has soared while in the Eurozone it has stabilized thanks to tighter fiscal policy. While it is set to continue to climb in the United States, it is on a path to recede slightly over the coming years in Europe, according to International Monetary Fund (IMF) estimates that preceded the latest budget proposals.

Pivot

With two of the world's three largest economies (China and the Eurozone) tightening fiscal policy, it could mean global growth may not respond as effectively to easier monetary policy. After enthusiastically embracing easing monetary policy this year, investors might soon pivot to a less optimistic focus on tightening fiscal policy.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs) covering about 85% of this China equity universe.

The MSCI EMU Index (European Economic and Monetary Union) captures large and mid-cap representation across the 10 Developed Markets countries in the EMU, covering approximately 85% of the free float-adjusted market capitalization of the EMU.

1024-0FU7

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Charles Schwab

Read more commentaries by Charles Schwab