Central Bank Policy and Global Bond Yields

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary

- In Europe, the ECB is stimulating a sluggish economy…

- …while in the UK, the problem is inflation.

- In contrast, the US is responding to stronger growth.

- Thus, we believe the Fed will be ‘slower to lower’ rates.

Not All Easing Policies Are Created Equal

Central banks around the world have begun recalibrating their monetary policies now that inflation has subsided. Since June, the world has seen the Federal Reserve (Fed) and the Bank of England (BOE) cut twice, while the European Central Bank (ECB) cut its policy rate three times to remove restrictive monetary parameters. On the other end of the spectrum, the Bank of Japan (BOJ) has hiked interest rates twice in 2024, as their economy has experienced sustained inflation for the first time in decades. The impact of each central bank’s decision has played out in the global bond markets.

The Fed May Be ‘Slower to Lower’

The Fed made an aggressive 50-basis point rate cut to kick-off its rate cutting campaign in September, followed by a 25-basis point cut at its November meeting. Financial strategists anticipate the Fed will cut again in December, and then lower the fed fund funds rate by an additional 1% in 2025. If this projection is correct, the fed funds rate would end 2025 at 3.375%, in line with the Fed’s forecast from September.

However, the economy is not cooling as fast as many forecasters have predicted. In Q3, GDP grew at 2.8% after growing 3% in Q2. To put this into perspective, the US economy is growing as fast as it grew the quarter prior to the pandemic, when the fed funds rate was at zero. Furthermore, inflation has slowed, and the labor market has been resilient, despite hurricanes and strikes making the data harder to analyze over shorter periods of time. Accordingly, the ‘data-dependent’ Fed looked beyond the volatility in the employment numbers at its most recent meeting by stating that “the risks to achieving its employment and inflation goals are roughly in balance.” Hence, we believe that the Fed may be “slower to lower” interest rates than the market is predicting. For proof, just look to the 10-year Treasury for guidance.

The Rise in Treasury Yields Point to Higher Growth, Not Inflation

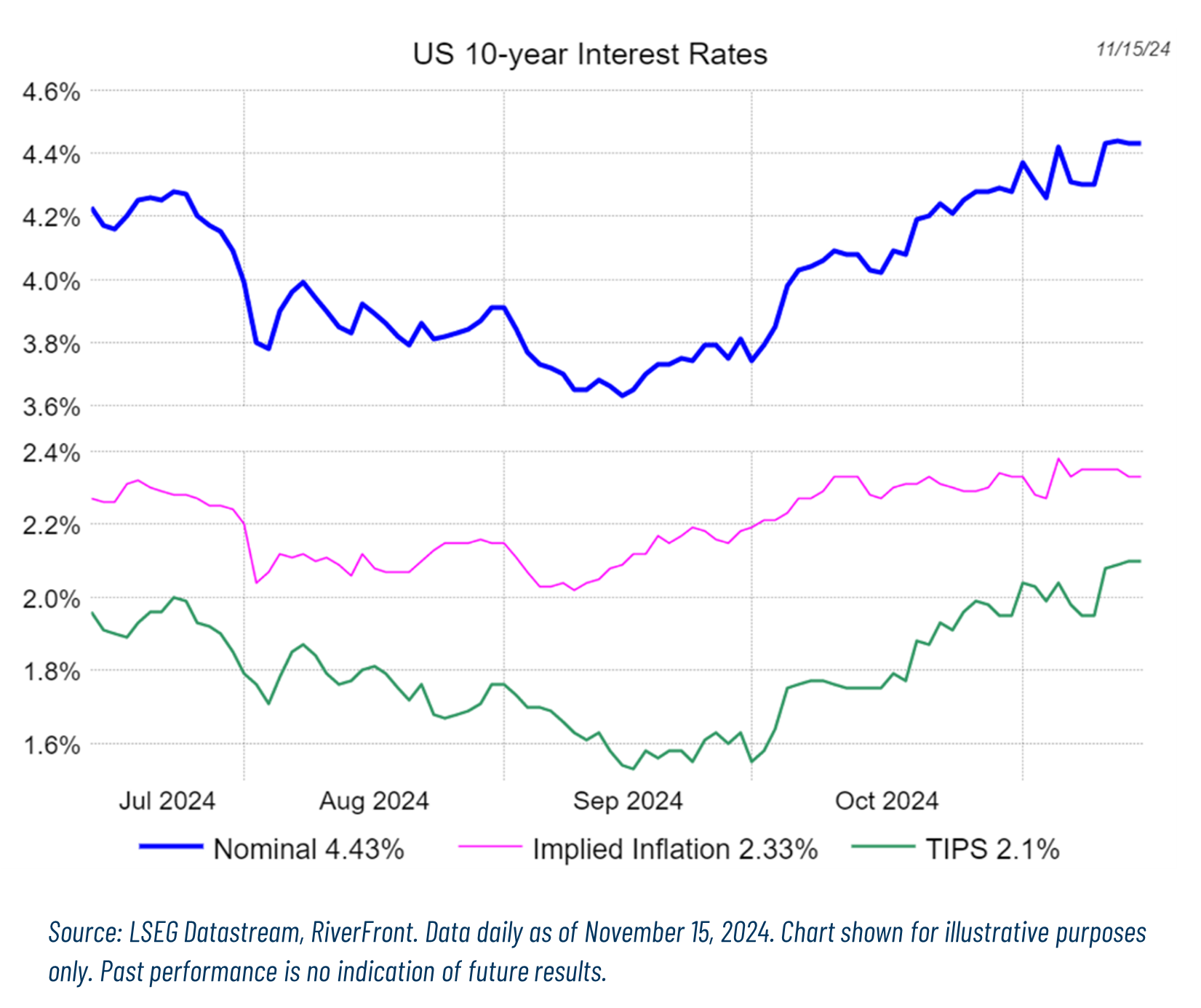

Prior to the Fed’s September rate cut, the 10-year Treasury yielded 3.62%. However, as of November 15th, the yield had moved up to 4.44%. As we wrote in our September 24th Weekly View, we expected 10-year yields to stall as the yield curve normalizes. At first glance, this market reaction defies logic because the Fed lowered short-term rates to help stimulate the economy. However, for simplicity’s sake, if we break the 10-year nominal yield into its’ two main signaling components, one can better understand the market reaction post-rate cuts.

In our chart at right, we show 3 things. The blue line is the yield on 10-year Treasury notes. The green line is the yield on Treasury Inflation Protected Securities or TIPS. It shows the real yield, or the portion of the nominal yield, (blue line), that is the expected inflation adjusted return for investing in the bond. The pink line is the difference between the green and blue lines. It represents the market’s implied inflation expectations and is known as the ‘break-even’ yield. After the first rate cut, the economic data has improved as the labor market has firmed, which in turn pointed to the economy growing. As you can see in the chart, inflation expectations (pink line) have been relatively stable over the last month as real yields have risen (green line). Thus, we believe nominal bond yields are reacting more to an improvement in US growth prospects than an acceleration of inflation risks. With growth prospects rising, the Fed may be ‘slower to lower’ interest rates than the market is pricing, in our view.

International Central Banks: Customized Responses for Different Economic Conditions

Internationally, the Bank of England (BOE) and the European Central Bank (ECB) both have begun cutting their policy rates as well. Unlike the Fed, the BOE and ECB have opted to only move in 25-basis point increments. Thus far, the BOE has seen its 10-year Gilt react very similarly to the 10-year Treasury with yields 0.59% higher since the rate cuts began. The 10-year Gilt yielded 3.88% in August when the BOE first cut and now yields 4.47% after the second rate cut. Unlike in the US, where rising rates reflect better economic prospects, the Gilt market views the rate cuts as increasing the likelihood for inflation to reappear. The ECB on the other hand has cut three times, and 10-year Bunds yield 2.35%, 0.20% lower than when the central bank began cutting in June. The ECB rate cutting policy has lowered yields due to the eurozone economy being in a more tenuous state, as its largest economy, Germany, attempts to avoid a recession. Thus, it is evident not all central bank easing policies are created equal. On the other end of the spectrum, the BOJ has raised interest rates as inflation expectations have increased. However, unlike the other developed central banks, its benchmark 10-year is rangebound.

Conclusion: We Continue to Prefer US Treasuries and the US Dollar Over International Bonds

While we still prefer domestic equities over bonds in our balanced portfolios, we believe that US Treasuries are a better relative value than international bonds for our fixed income allocation due to the relative yield differential. Even in the case of 10-year Gilts where yields are comparable to Treasuries, we do not see the risk-reward benefit given the added currency risk that comes along with such an allocation. We expect more money to flow into Treasuries as investors are getting a second chance to get off the sidelines and lock in higher yields for longer, as the Fed will be slower to lower, in our opinion. Additionally, the market reaction to the Fed’s rate cutting campaign has strengthened the dollar as the US is seen as having the best economic prospects relative to other developed economies. We believe higher yields on Treasuries will bring more investors to the table, both foreign and domestic, which should enhance the dollar’s appreciation.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

For more news, information, and strategy, visit the ETF Strategist Channel.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Index Definitions:

The Bloomberg Aggregate Bond Index, or "the Agg," is a broad-based fixed-income index used by bond traders and managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

Bloomberg U.S. Treasury Bills 1-3 Month Index is a component of the Short Treasury index. The Bloomberg Short Treasury Index includes aged US Treasury bills, notes and bonds with a remaining maturity from 1 up to (but not including) 12 months. It excludes zero coupon strips.

Treasury Bonds is represented by the Bloomberg US Treasury Index which measures the performance of the US Treasury bond market.

10 year treasury note: The 10-year Treasury Note is a debt obligation issued by the United States government with a maturity of 10 years upon initial issuance. A 10-year Treasury note pays interest at a fixed rate once every six months and pays the face value to the holder at maturity.

Treasury inflation-protected securities (TIPS) are a type of Treasury security issued by the US government. TIPS are indexed to inflation in order to protect investors from a decline in the purchasing power of their money. As inflation rises, TIPS adjust in price to maintain its real value.

Definitions:

The European Central Bank (ECB) is the central bank responsible for monetary policy of the European Union (EU) member countries that have adopted the euro currency. This currency union is known as the eurozone and currently includes 19 countries. The ECB's primary objective is price stability in the euro area.

The Bank of England (BoE) is the central bank of the United Kingdom. The BoE oversees monetary policy and issues currency. It also regulates banks, financial firms, and payment systems. Like other central banks, the BoE may act as a lender of last resort in a financial crisis.

The Bank of Japan (BOJ) is headquartered in the Nihonbashi business district in Tokyo. The BOJ is the Japanese central bank, which is responsible for issuing and handling currency and treasury securities, implementing monetary policy, maintaining the stability of the Japanese financial system, and providing settling and clearing services. Like most central banks, the BOJ also compiles and aggregates economic data and produces economic research and analysis.

Gilt-edged securities are high-grade bonds issued by certain national governments and private organizations. In the past, these instruments referred to the certificates issued by the Bank of England (BOE) on behalf of the Majesty's Treasury, so named because the paper they were printed on customarily featured gilded (golden) edges.Inflation is a gradual loss of purchasing power, reflected in a broad rise in prices for goods and services over time.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. (bps = 1/100th of 1%)

In a rising interest rate environment, the value of fixed-income securities generally declines.

The yield curve is a line that plots yields (interest rates) of bonds having equal credit quality but differing maturity dates. The slope of the yield curve gives an idea of future interest rate changes and economic activity.

A recession is a significant, widespread, and prolonged downturn in economic activity. A common rule of thumb is that two consecutive quarters of negative gross domestic product (GDP) growth indicate a recession. However, more complex formulas are also used to determine recessions.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

US Equities include stocks listed in the United States. Stocks represent partial ownership of a corporation. If the corporation does well, its value can increase, and investors can share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Small/mid-cap equities, MLPs, REITS and alternatives equities are types of US Equities and assume further risks described below.

Interest rate sensitivity is a measure of how much the price of a fixed-income asset will fluctuate as a result of changes in the interest rate environment. Securities that are more sensitive have greater price fluctuations than those with less sensitivity. This type of sensitivity must be taken into account when selecting a bond or other fixed-income instrument the investor may sell in the secondary market. Interest rate sensitivity affects buying as well as selling.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2024 RiverFront Investment Group. All Rights Reserved. ID 4033690

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All