As expected, the Federal Reserve made no change in policy at the July meeting of the Federal Open Market Committee (FOMC). The target range for the federal funds rate—the rate that banks charge each other for overnight loans—was left unchanged at 4.25% to 4.5%, where it has been since December 2024.

There were two dissenting votes however—one from Fed Governor Christopher Waller and one from Fed Governor Michelle Bowman. Both favored a rate cut at the July meeting. Although dissents have not been common in recent years, the majority of the committee still voted to hold steady for now.

Balance-of-risks focus is still on inflation for now

Despite the unchanged policy, the Fed appeared to open the door for a potential rate cut later in the year. The statement accompanying the Fed's meeting continued to characterize the labor market as "solid" but the assessment of the economy's growth rate was downgraded to "moderate" compared to "a solid pace." The description of inflation remained unchanged at "somewhat elevated."

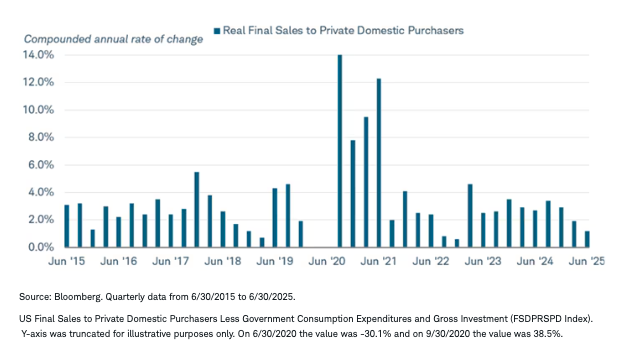

We continue to believe that there will be enough evidence to support a decision to ease policy by the September meeting. By then, we expect to see further moderation in economic growth and enough weakness in the labor market to warrant a rate cut. The pace of consumer spending has already slowed, growing just 1.4% in the second quarter and averaging just 1.0% year to date. Real final sales to domestic purchasers—a reading that strips out the volatility of trade and inventories—grew at a sluggish 1.2% in the most recent quarter.

The pace of consumer spending has slowed

However, we don't look for a rapid decline in rates, as inflation is likely to remain above the Fed's 2% target until next year due to the impact of tariffs, which are pushing prices for imported goods higher. In his press conference following the meeting, Fed Chair Jerome Powell noted that tariff price increases were just beginning to show up, and that inflation readings likely would move higher in the near term. The committee was hopeful that those price increases will prove "short-lived" but they wanted to ensure that they don't produce a longer-turn rise in inflation or inflation expectations.

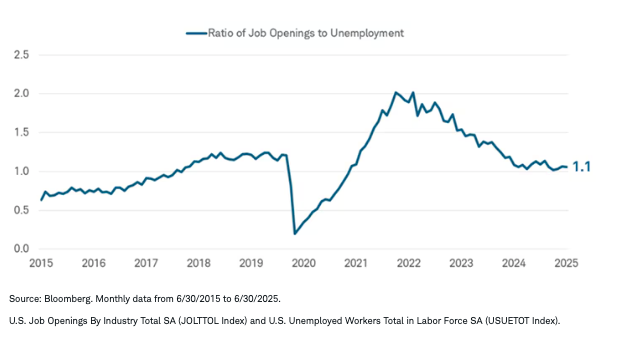

Recent data from the Job Openings and Labor Turnover Survey (JOLTS) suggest that the labor market is languishing as hiring slows. The unemployment rate has remained low because there haven't been widespread layoffs, but the trends suggest a softening tone. If that continues, we would expect the Fed to respond with a rate cut even if the inflation readings remain above target. The assumption would be that slower growth will pull inflation lower longer term.

Job openings have slowed

Given the potential for inflation to be above the 2% target for quite some time, the Fed will likely take a cautious approach to cutting rates and the ending rate may be higher in this cycle than previously estimated. A terminal rate of 3% to 3.5% might be the low for this cycle, similar to the median longer-run projection of 3.0% from the Fed's last Summary of Economic Projections.

Treasury yields rose modestly following Powell's comments in the press conference, with short-term yields rising more than long-term yields. The two-year Treasury yield rose five basis points, or 0.5%, with the federal funds futures market pricing in one or two cuts by the end of this year. As we've noted, 10-year Treasury yields have been around 4.35% to 4.40%—near the current federal funds rate—for several months. Longer term, we see room for yields to drop but it will take more evidence of easing inflation pressures to see yields fall.

For investors, today's FOMC meeting does little to change our views. We continue to suggest maintaining an intermediate-term average portfolio duration and focusing on higher-credit-quality bonds.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

All names and market data shown are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Investment and Insurance Products Are: Not FDIC Insured • Not Insured by Any Federal Government Agency • Not a Deposit or Other Obligation of, or Guaranteed by, the Bank or any of its Affiliates • Subject to Investment Risks, Including Possible Loss of Principal Amount Invested

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2025 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

© Charles Schwab

Read more commentaries by Charles Schwab