Why have value stocks been more durable than expected in today’s uncertain market environment?

Since early 2025, value stocks have enjoyed a strong run, defying market volatility driven by trade tensions, geopolitical stress and macroeconomic uncertainty. That resilience may seem counterintuitive given value’s historically cyclical profile. Yet, we believe the underlying characteristics of value stocks are proving particularly well suited to today’s evolving market landscape.

Global markets have faced a wave of destabilizing forces over the last two years. In 2025, President Trump’s tariff agenda fueled market turbulence and made it hard for investors to forecast earnings. Ongoing AI disruption has added an unpredictable variable to businesses, while raising profitability questions about the US mega-caps. Meanwhile, the Middle East conflict prompted a surge in oil prices with cascading effects across economies and sectors.

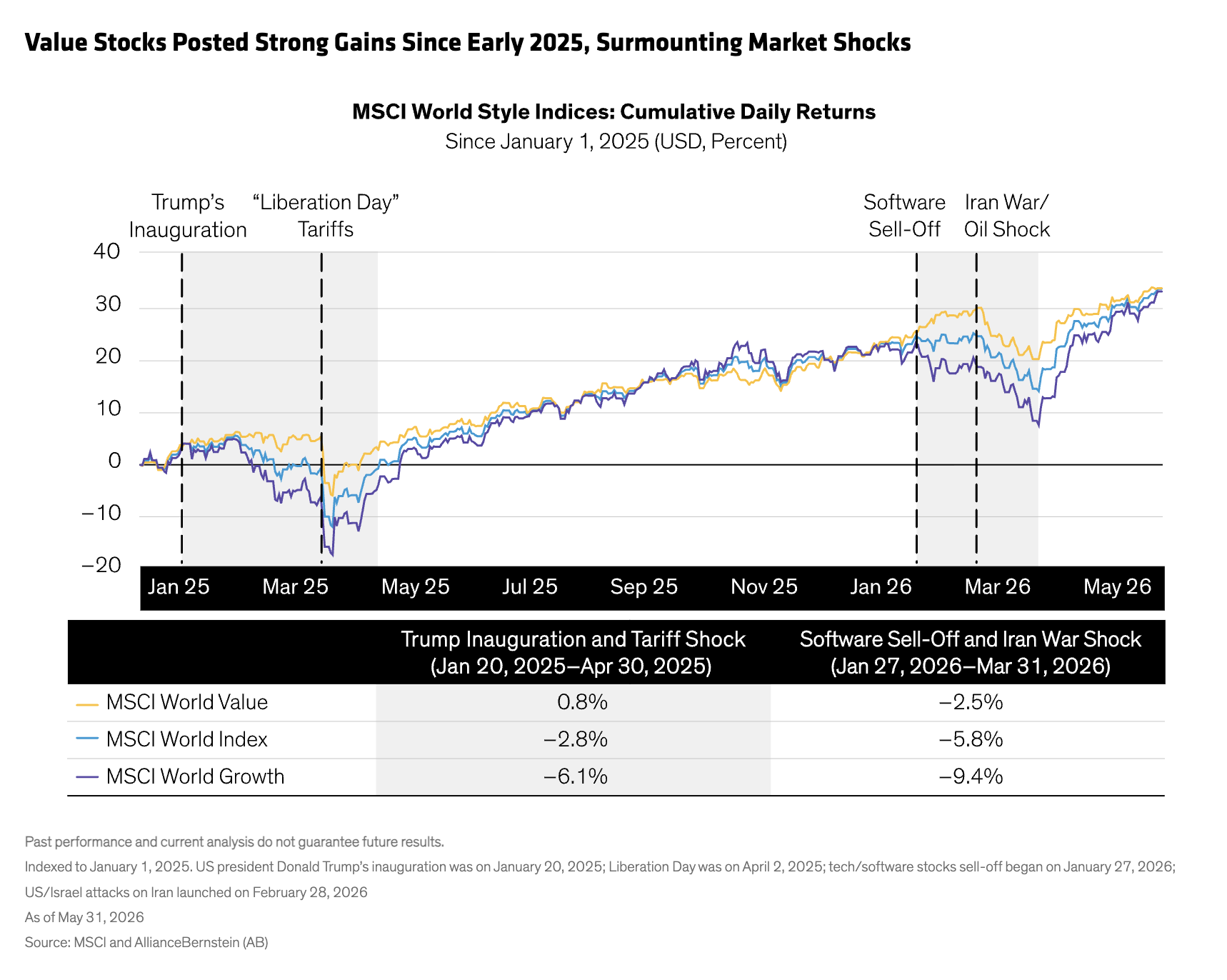

Investors in value equities have largely surmounted these shocks. Even though growth stocks have rebounded in the second quarter, since the beginning of 2025, the MSCI World Value outperformed both growth and the broader market during major market shocks (Display).

So how can we explain value’s resilience? Three reasons stand out.

Read more: Aviation Leasing: Looking Beyond the Fuel Price Shock

The “HALO” Effect of AI Build-Out

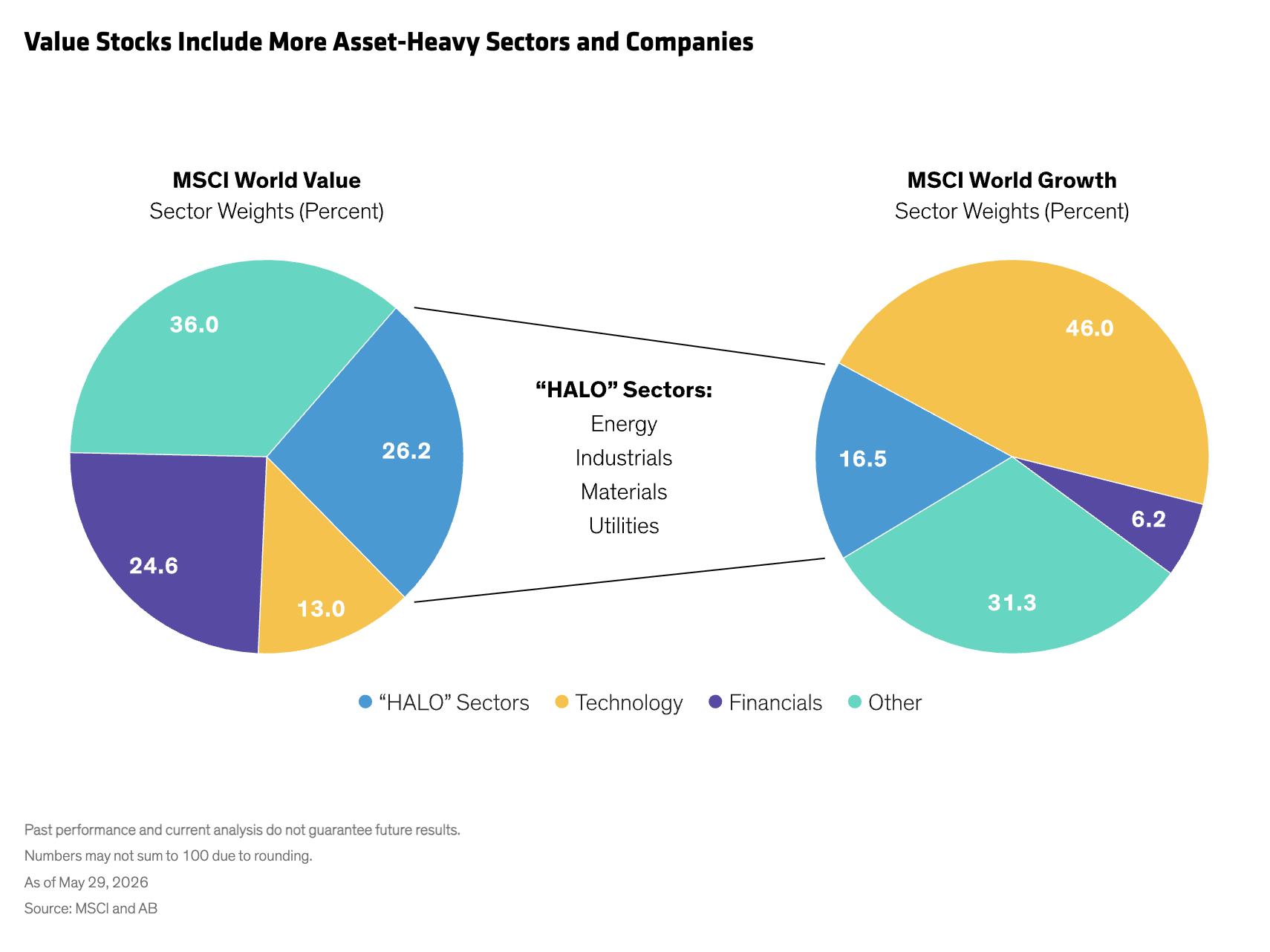

AI has led to rapid expansion in digital capacity, in areas such as software and automation. At the same time, it has exposed bottlenecks in the physical economy. Massive spending on AI infrastructure is benefiting companies with heavy assets and long-lived capital bases—sometimes referred to as “HALO” (heavy assets, low obsolescence).

These companies can be found in industries such as energy, materials and resources—big constituents of global value benchmarks (Display). Many are considered quality, cyclical businesses, which struggled back in the lower-growth 2010s as globalization peaked and inventories were efficient. Today, however, they’re benefiting from renewed pricing power driven by infrastructure demand, supply chain realignment and rising investment in real assets.

Beyond the HALO-leaning sectors, some value-oriented segments of the technology ecosystem are also benefiting from the AI build-out. For example, semiconductor shares are surging, which include chipmakers and memory manufacturers that are significant constituents in value benchmarks.

Shorter-Duration Cash Flows Are Back in Vogue

Since the AI boom began in late 2022, investors have driven valuations higher for companies perceived to be leaders of the technological revolution. US mega-cap valuations soared as investors priced in future earnings streams that may only materialize well into the next decade.

These long-duration cash flows are now under greater scrutiny. With hyperscalers investing heavily in AI, investors are reassessing the timing and magnitude of potential returns. As a result, performance has become more volatile among large-cap technology stocks recently, while markets attempt to figure out how much their high-growth potential is really worth today.

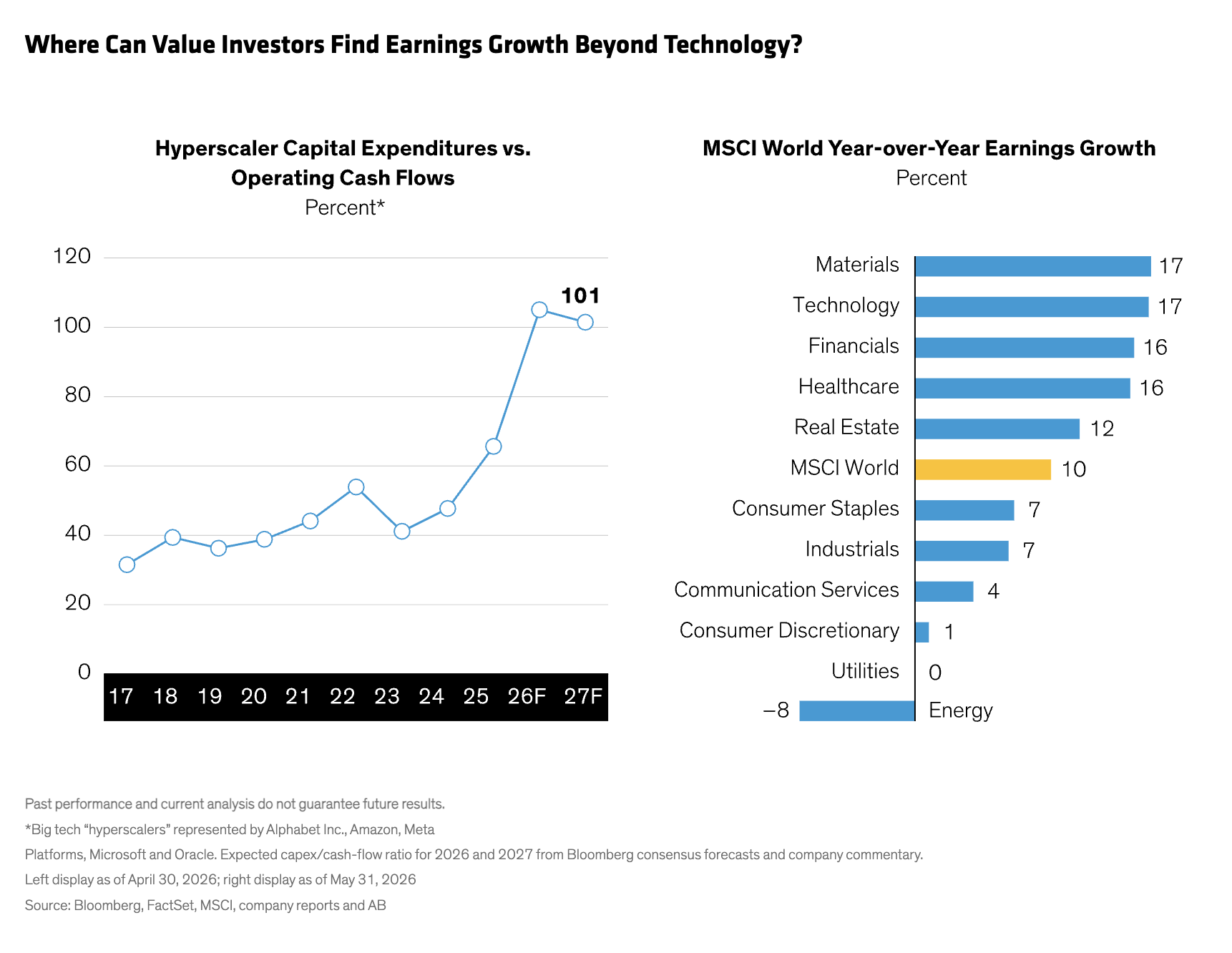

Free cash flow (FCF) is at the heart of that question. While the hyperscalers have formidable FCF from their dominant businesses, massive capital spending on AI is changing their underlying financial profiles (Display). To pay for their capex plans, the mega-caps are now taking on significant debt and raising equity capital, which pushes out the timeline for returns to shareholders. Across the US technology sector, five-year earnings-growth expectations have reached an annualized 23%, a forecast that, in our view, is difficult to underwrite with confidence.

In contrast, we believe businesses with shorter-duration cash flows are much more predictable. These companies tend to be more prominent in the value universe, where sectors such as financials, materials, healthcare and real estate are showing strong earnings growth potential (Display, above). And because of the nature of their business models, we think their five- to seven-year cash flows deserve a higher level of confidence from investors. As we see it, the combination of attractively valued stocks and shorter-duration cash flows provide a clearer view of equity return potential in a market that craves more certainty.

Forecasting Normalized Earnings Is a Value Specialty

The forces described above have created fertile ground for value investors. Even so, capturing the return potential of undervalued stocks is no easy task. It requires a deep understanding of how the cycle of a given product unfolds, when to buy and when to sell.

In other words, unlocking value is all about whether a company’s share price accurately reflects its normalized, mid-cycle earnings power. Value opportunities arise when the market becomes overly pessimistic on a company’s prospects, creating a disconnect between the valuation and future earnings potential. This approach differs from growth investing, which focuses on identifying companies capable of compounding earnings well beyond current expectations.

In today’s environment, we believe the value investing discipline is particularly relevant. As demand for physical assets increases and supply constraints persist, many value-oriented companies that are rooted in the physical world are ripe for rerating. Sectors such as commodities, financials and real estate, which are more prevalent within the value universe, tend to perform well during inflationary periods, addressing a prominent concern for investors today. What’s more, since 2025, the MSCI World Value delivered solid risk-adjusted returns, posting a Sharpe ratio of 2.3—exceeding the broader MSCI World’s 1.4, with lower levels of volatility.

Discipline Helps Counter Disruption

Of course, value stocks aren’t inherently defensive in all environments, and not every value strategy is positioned to capitalize on today’s conditions. It takes a highly disciplined security selection process and robust risk controls to avoid “value traps” by buying stocks that appear to be attractively valued but are in fact facing structural challenges.

With the right approach, we think value equities can play a complementary role in allocations that may have become heavily weighted toward growth stocks in recent years. By focusing on reasonably priced businesses that generate solid cash flows over time, investors can build portfolios that are well equipped to navigate an era of heightened uncertainty and structural change.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Avi Lavi was appointed Chief Investment Officer of Global and International Value Equities in March 2016 and has also been Portfolio Manager for Global Research Insights since May 2016. He has been a member of the Cross Border team since early 2012.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

More Innovative ETFs Topics >