Investors should consider designing portfolios to stay resilient and capture opportunities.

Markets weathered turmoil in the first half, helped by solid earnings with signs of broadening beyond a few AI beneficiaries. If the war in Iran eases, oil prices could normalize, reducing inflation pressure. Still, growth, inflation and policy risks may be underestimated. Two areas we’re monitoring are how energy prices affect consumers and the pace of AI monetization. We think a diversified multi-asset approach includes an equity overweight, downside resilience and inflation protection.

Volatility as Expected, but Markets Have Been Resilient

Coming into 2026, our outlook was generally favorable. AI was still in its early stages, some signs emerged that market fundamentals would provide broader support beyond a handful of tech titans and central banks seemed poised to cut policy rates. But valuations were elevated, performance was still highly concentrated and the pace of AI monetization was up for debate.

Markets: What to Watch Midway Through 2026

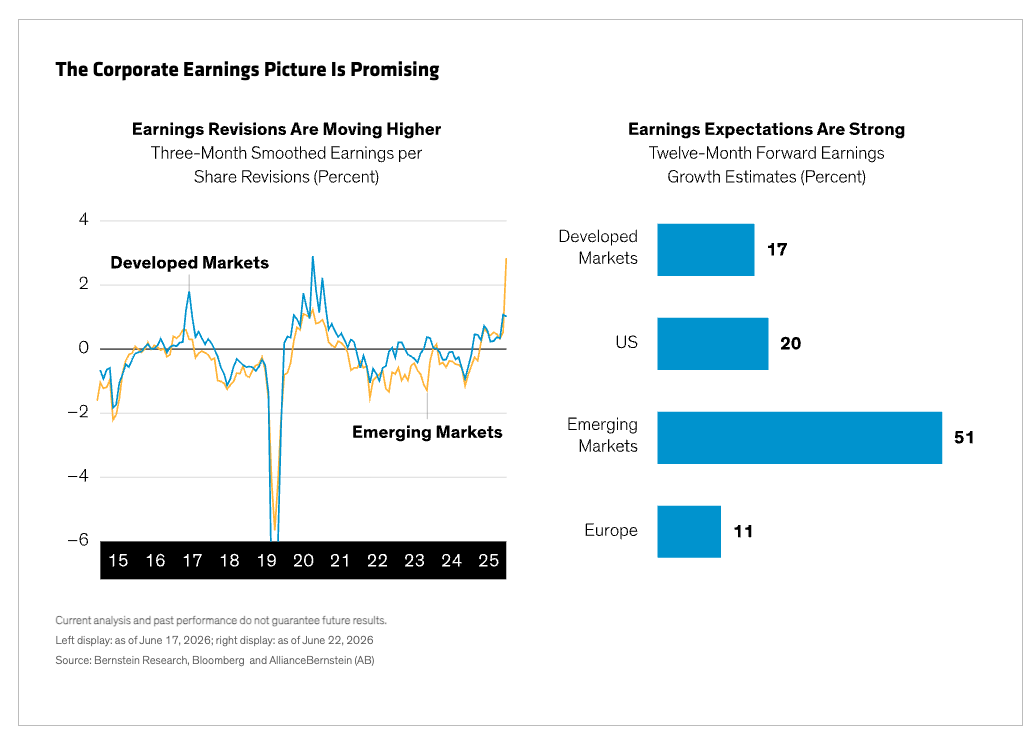

This backdrop suggested to us that the path this year would be bumpier, and two rapid-fire shocks reinforced this view. In late February and March, markets slumped as investors looked more deeply into how quickly AI investment would translate into profits, with concern intensifying around AI’s disruption among software firms. The onset of war in Iran moved energy and inflation worries back to the front burner, triggering a sell-off. Still, the market rebounded relatively quickly thanks to strong earnings delivery (Display), especially in markets with high tech exposure.

As we enter the second half, the market view seems to be that the shock will be temporary. Hopes for de-escalation of the conflict and a reopened Strait of Hormuz have encouraged investors to look through near-term disruption and price an eventual normalization in oil markets, which had started at publication time with oil trading below its pre-conflict level. For now, that supports a relatively benign base case, but one that could shift quickly. Renewed escalation, fresh disruption to energy flows or a resurgence in geopolitical risk premia could push energy prices up again, reviving concerns around input costs, inflation expectations and real household incomes.

Broadly speaking, we’re still positive heading into the second half of the year. In our view, the two developments that defined the first half remain key pieces of the puzzle, and we continue to focus on their potential implications.

Has the War Lasted Long Enough to Disrupt the Macro Picture?

While oil prices came down late in the first half, they’ve been higher long enough to influence input costs, inflation expectations and central bank paths. This raises the question, Is the shock starting to reach consumers—a key part of major economies?

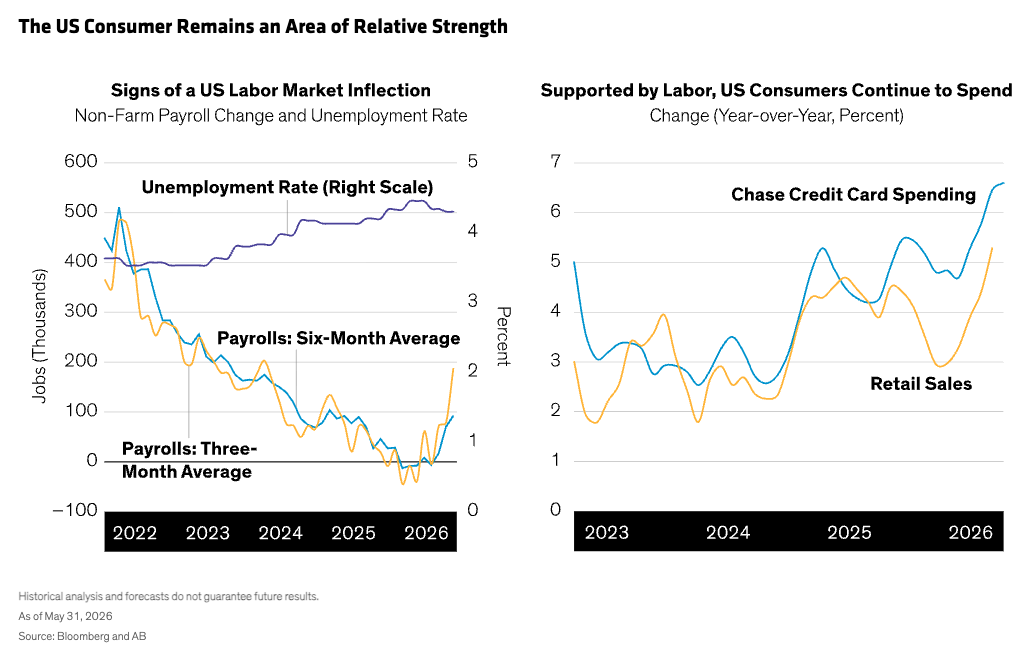

Real, or inflation-adjusted, household income is the clearest channel for transmitting the pain, and UK and European consumers seem likely to feel it earlier. Consumers in those regions had weaker fundamentals even before the war. The consensus expects global growth to slow from last year while avoiding recession; we think the outcome could be somewhat better, supported by resilient US domestic demand and a seemingly better positioned US consumer (Display).

As we enter the second half, the market view seems to be that the shock will be temporary. Hopes for de-escalation of the conflict and a reopened Strait of Hormuz have encouraged investors to look through near-term disruption and price an eventual normalization in oil markets, which had started at publication time with oil trading below its pre-conflict level. For now, that supports a relatively benign base case, but one that could shift quickly. Renewed escalation, fresh disruption to energy flows or a resurgence in geopolitical risk premia could push energy prices up again, reviving concerns around input costs, inflation expectations and real household incomes.

Broadly speaking, we’re still positive heading into the second half of the year. In our view, the two developments that defined the first half remain key pieces of the puzzle, and we continue to focus on their potential implications.

Has the War Lasted Long Enough to Disrupt the Macro Picture?

While oil prices came down late in the first half, they’ve been higher long enough to influence input costs, inflation expectations and central bank paths. This raises the question, Is the shock starting to reach consumers—a key part of major economies?

Real, or inflation-adjusted, household income is the clearest channel for transmitting the pain, and UK and European consumers seem likely to feel it earlier. Consumers in those regions had weaker fundamentals even before the war. The consensus expects global growth to slow from last year while avoiding recession; we think the outcome could be somewhat better, supported by resilient US domestic demand and a seemingly better positioned US consumer (Display).

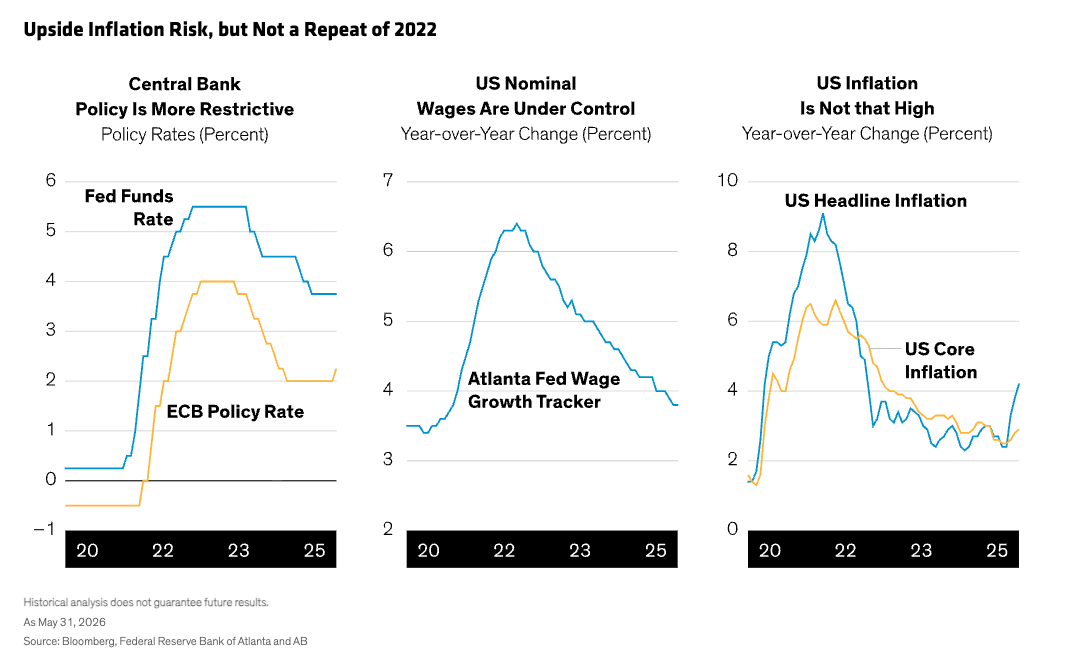

Interest rates seem most likely to show the pressure, and central banks’ policies could diverge further in coming months. The Fed may be more willing to set aside temporarily higher energy prices if labor markets soften, while the European Central Bank and Bank of England could face pressure to respond, leaving them battling inflation with a weaker growth backdrop. But overall, economies may be better positioned to absorb an energy shock than in 2022 (Display).

Exploring What the Next Chapter of the AI Story Will Look Like

As we see it, the AI debate is shifting from the scale of capital spending to whether that scale will translate into enough productivity gains, revenue and earnings growth to justify it. The investment phase of the AI cycle still seems underway, but investors are increasingly looking to what comes next. Can leadership spread beyond “pick-and-shovel” firms into areas like software and power?

The software sell-off has been broad, but some firms will likely play a role in AI’s next phase. We see the pipeline of initial public offerings as a key test of the market’s appetite for long-term AI growth. What we see now doesn’t yet look like a classic valuation bubble, but lofty earnings expectations may not be met if the sizable capital already deployed doesn’t translate into accelerating earnings.

How Should Investors Consider Positioning Multi-Asset Portfolios?

At the midway point of the year, we think investors should consider the following pathways to maintain resilience while capturing opportunities.

Overweight equities, with a US preference. We think equity exposure should favor the US, with its AI exposure, stronger earnings and profitability and more resilient economy. Emerging markets and Japan offer access to the AI value chain, and earnings revisions are improving in certain sectors.

Build portfolio resilience. As the first-half turmoil highlighted, investors need to think not only about bolstering defenses but doing it with a diverse tool kit. Option-based strategies may mitigate downside while keeping exposure to growth areas. Lower-beta stocks and gold may also help defense. Exposure to the US dollar also helped defend during volatility this year (though our longer-term view is for dollar weakening).

Deploy systematic equity strategies. Markets will likely stay concentrated for a while, which can increase the risk of unintended biases. Systematic equity approaches may help manage these risks while offering potential for outperformance that complements fundamental strategies.

Underweight duration but tap income. Duration could be less diversifying, with stagflation worries and expected tighter monetary policy likely to keep yields elevated, though the market seems too hawkish in the UK. Higher overall yields offer compelling potential for income seekers.

Explore other sources of inflation protection. While stocks may be considered the biggest real asset available, other strategies have the potential to enhance the mix. Real assets, commodities, gold and option protection are building blocks that could help if the energy shock lasts or volatility rises.

From a big-picture perspective, we think a multi-asset approach is well suited to the current environment, providing that it’s disciplined, risk-aware and able to adapt dynamically to a changeable landscape.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein

More Volatility/Downside Protection Topics >