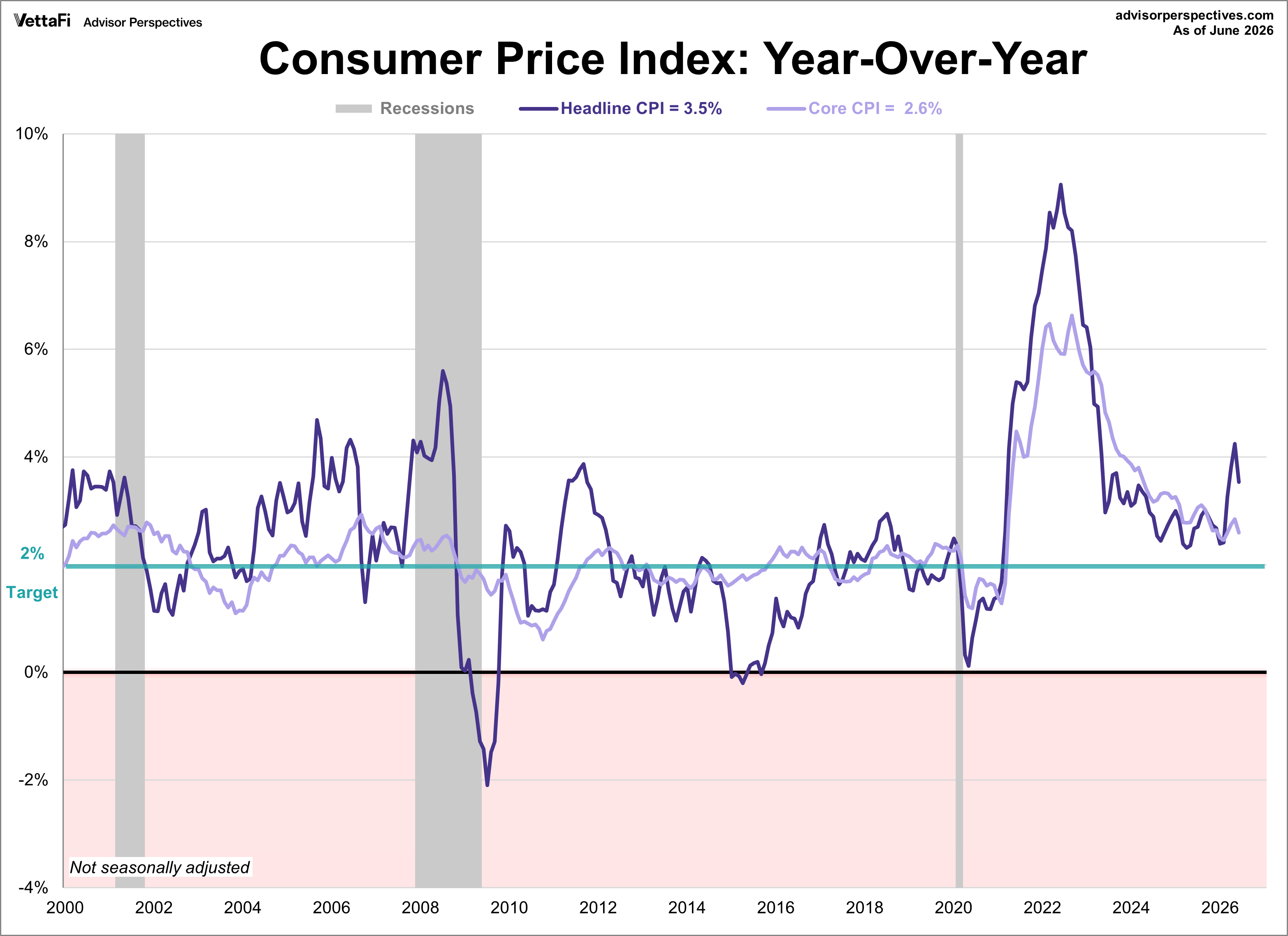

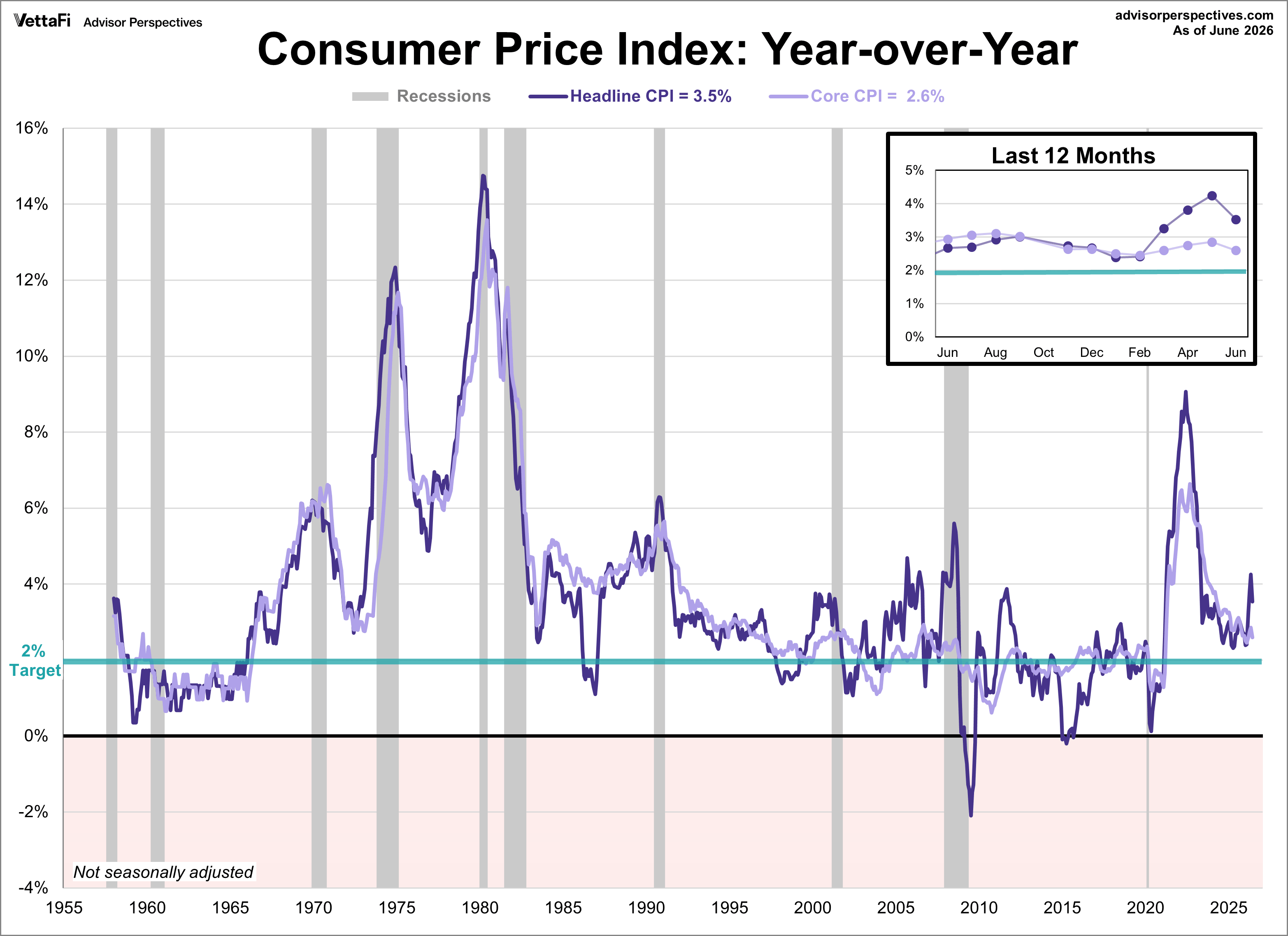

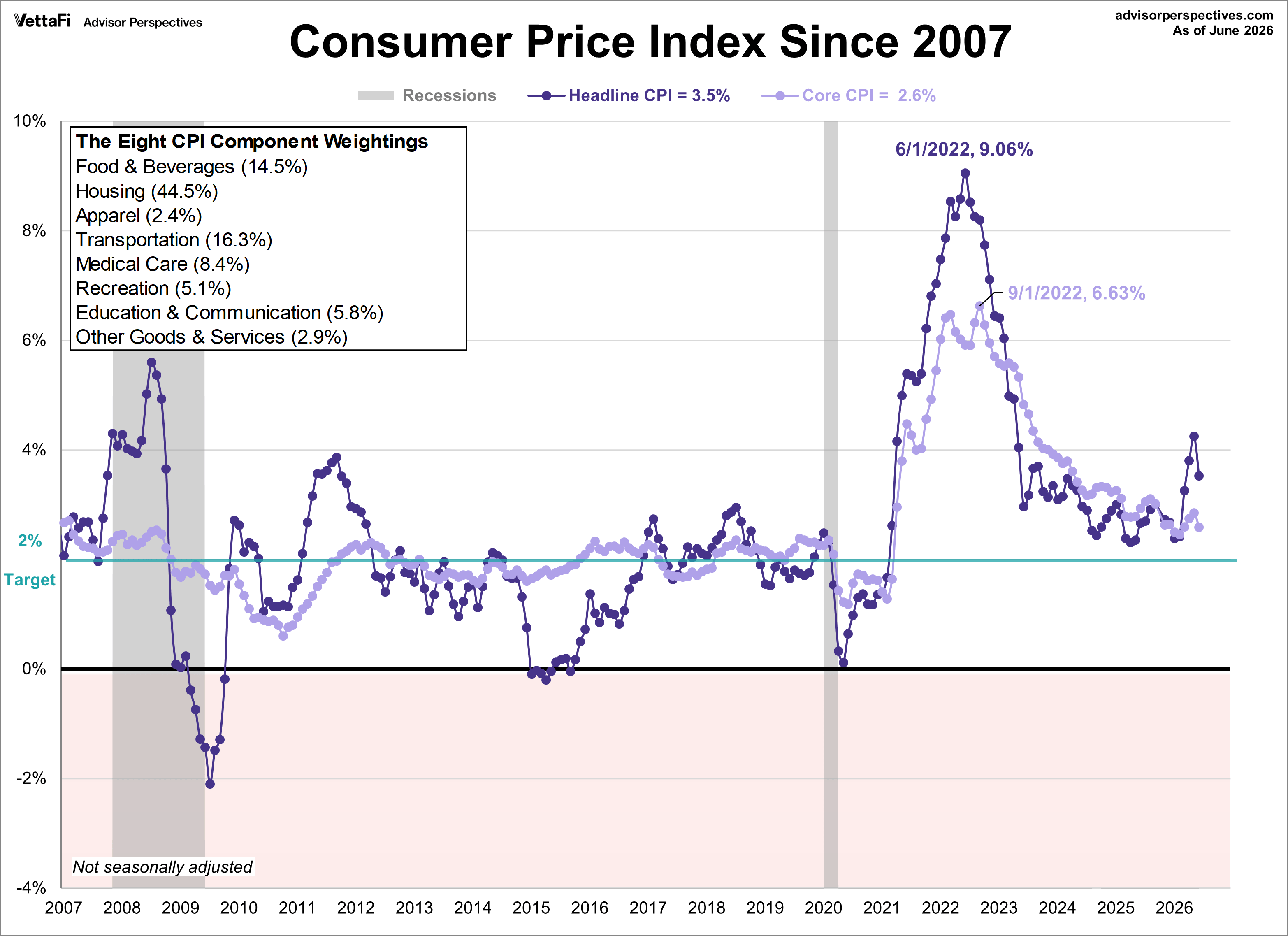

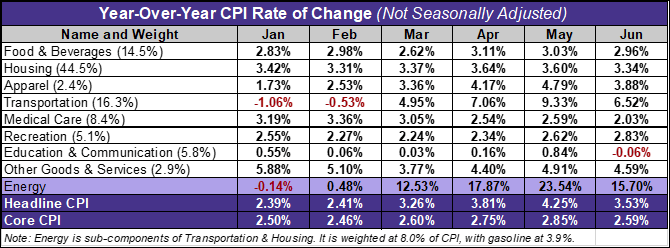

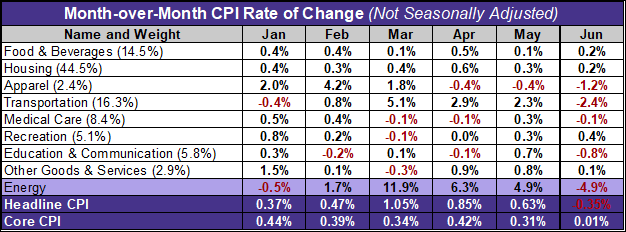

Inflation cooled for the first time in five months as the headline Consumer Price Index eased to 3.5% year-over-year. This marks a sharp deceleration from May's 4.2% reading, and was lower than the 3.8% forecast. On a monthly basis consume prices fell 0.4%, the largest monthly decline since April 2020 and more than the projected 0.1% decrease. The decline was largely driven by a fall in energy prices (-5.7%) which more than offset increases in other categories such as shelter (+0.1%) and food (+0.2%).

On a "core basis," which excludes volatile food and energy prices, prices rose 2.6% year-over-year and were flat month-over-month. Both readings were lower than their respective forecasts of 2.8% and 0.2%.

Key Takeaways

- Headline inflation eased to 3.5% year-over-year while core inflation fell to 2.6% in June.

- Headline prices fell 0.4% from May, driven by a 5.7% drop in energy prices.

- Current market expectations show an 88% chance of a hold at the next Fed meeting versus a 12% chance of a 25 basis point hike.

Here is the introduction from the BLS summary, which leads with the seasonally adjusted monthly data:

The Consumer Price Index for All Urban Consumers (CPI-U) decreased 0.4 percent on a seasonally adjusted basis in June after rising 0.5 percent in May, the U.S. Bureau of Labor Statistics reported today. This decline in the all items index was the largest 1-month decrease since April 2020 when it fell 0.8 percent. Over the last 12 months, the all items index increased 3.5 percent before seasonal adjustment.

The index for energy fell 5.7 percent in June after rising 3.9 percent in May, 3.8 percent in April, and 10.9 percent in March. The energy index was the largest contributor to the monthly all items decrease, more than offsetting increases in other indexes including those for shelter and food. The index for food increased 0.2 percent over the month, as did the index for food at home and the index for food away from home.

The index for all items less food and energy was unchanged in June. Indexes that decreased over the month include motor vehicle insurance, communication, apparel, medical care, and used cars and trucks. Conversely, the indexes for recreation, household furnishings and operations, and personal care were among the major indexes that increased in June.

The all items index rose 3.5 percent for the 12 months ending June after rising 4.2 percent for the 12 months ending May. The all items less food and energy index rose 2.6 percent over the year, following a 2.9-percent increase over the 12 months ending May. The energy index increased 15.7 percent for the 12 months ending June. The food index increased 3.0 percent over the last year.